From the Otteau Group:

Home Sales Shift into 3rd Gear in April

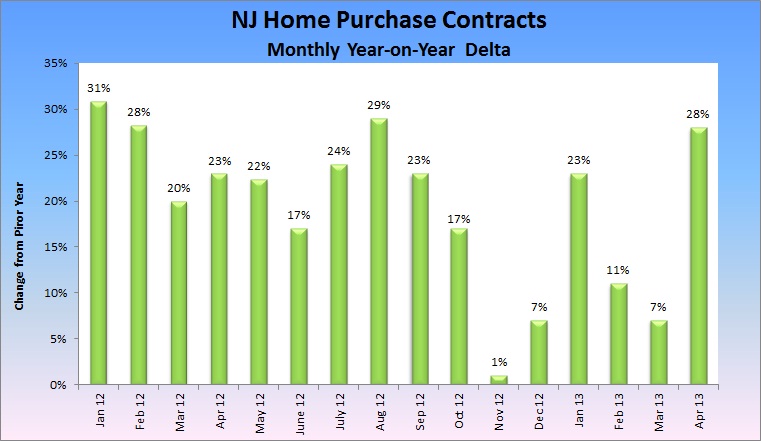

Home purchase contracts in New Jersey soared in April, recording a 28% increase compared to one year ago. Given that the pace of sales rose by 23% in April-2012, purchase demand has expanded by an astounding 58% over the past 2 years. The “buy now, pay less” mood among home buyers is creating a sense-of-urgency that is likely to raise purchase demand in 2013 to pre-recession levels last seen in 2006.

From the Star Ledger:

Study finds 350,000 homes, $118 billion at risk of flood surge in another Sandy

More than 350,000 homes in New Jersey are at risk of being damaged in a storm surge similar to the one caused by Hurricane Sandy, according a report issued yesterday, and most of them fall into the “very high” and “extreme” risk categories.

CoreLogic, an analytic company for real estate professionals, found that 4 million properties nationwide are exposed to storm-driven water surges along the Eastern and Southern coasts. Florida, Louisiana and Texas, all with extensive shorelines, have the most homes at risk. New Jersey ranks fourth because of its relatively low elevation and the density of houses.

The estimated value of property in New Jersey at risk from another Sandy is $118 billion, according CoreLogic. When combined with New York and Long Island, the total rises to $200 billion.

Damage from Sandy was estimated at $50 billion.

From the NYT:

In a Seller’s Market, Every Minute Counts

If there was any doubt that New York City real estate has become a seller’s market, consider the following: open houses are packed to capacity, bidding wars and all-cash offers have almost become the norm, and some listing prices actually rise, not drop, after a home is listed.

“It’s the kind of insanity you live for in this business,” said Mickey Conlon, a broker with CORE, recalling a two-bedroom two-bath condominium at 49 East 21st Street in the Flatiron neighborhood that he listed with his business partner, Tom Postilio, for $1.89 million in early January.

“At the moment, that was considered aggressive pricing,” Mr. Conlon said. Yet within 24 hours, the brokers had received a flurry of requests to see the place, which prompted them to be bold. The next day they raised the price by $100,000, to $1.99 million. Though some potential buyers grumbled about the change, about 100 people came to the first open house. Soon, there were multiple offers above the asking price. By the end of January, there was a signed contract for $2.16 million — all cash. The sale closed in April.

The rules of engagement for buying an apartment in the city have changed. Negotiation, brokers say, is no longer part of the equation. Forget about taking time to mull over your decision. Serious buyers need to be prepared to pounce. And while lots of cash has always helped, it’s now more important than ever, as sellers select the best offers with the least amount of hassle involved.

Not that sellers can name just any price. Brokers caution that even in this market of extremely tight inventory, listings priced too high tend to linger, and low prices intended to bring the biggest crowds through the door could result in lowball offers. There is an art to choosing the right price.

While housing prices across the country recently posted their biggest gains in seven years, New York City’s market has been experiencing a slow and steady recovery ever since the market hit bottom in 2009.

More recently, scarce apartment listings and low mortgage rates have stoked competition among buyers and driven up prices. The number of Manhattan apartments for sale dropped 27.6 percent last month, to 5,077, versus 7,011 for the same period a year ago, according to the appraisal firm Miller Samuel. At the same time, prices have inched up. The median sale price rose 12 percent to $930,000, from $829,000 a year ago, according to the most recent available data for the second quarter, which began on April 1. That follows a 5.9 percent year-over-year increase in the median sale price, to $820,555, in the first three months of the year.

Apartments are going into contract at a faster pace, with listings lasting 105 days on the market, down from 156 a year ago, according to Miller Samuel. In popular neighborhoods like the West Village, it’s not uncommon for sought-after properties to go into contract well above the asking price in the head-spinning span of 10 days or less. Brokers are fueling the frenzy, turning open houses into pressure cookers, with tactics like one-day-only showings and short deadlines set for best and final offers.

Contracts data I posted earlier this month:

Here it is! The first look at pending home sales (contracts) for Northern NJ.

(Source GSMLS, except Bergen- NJMLS) – Updated with 2011 Data

April Pending Home Sales (Contracts)

——————————-

Bergen County

April 2011 – 669

April 2012 – 812

April 2013 – 1016 (Up 25.1% YOY, Up 51.9% Two Year)

Essex County

April 2011 – 320

April 2012 – 352

April 2013 – 555 (Up 57.7% YOY, Up 73.4% Two Year)

Hunterdon County

April 2011 – 100

April 2012 – 126

April 2013 – 149 (Up 18.3% YOY, Up 49.0% Two Year)

Morris County

April 2011 – 394

April 2012 – 436

April 2013 – 619 (Up 42.0% YOY, Up 57.1% Two Year)

Passaic County

April 2011 – 168

April 2012 – 205

April 2013 – 320 (Up 56.1% YOY, Up 90.5% Two Year)

Somerset County

April 2011 – 280

April 2012 – 332

April 2013 – 418 (Up 25.9% YOY, Up 49.3% Two Year)

Sussex County

April 2011 – 107

April 2012 – 122

April 2013 – 175 (Up 43.4% YOY, Up 63.6% Two Year)

Union County

April 2011 – 330

April 2012 – 323

April 2013 – 470 (Up 45.5% YOY, Up 42.4% Two Year)

Warren County

April 2011 – 74

April 2012 – 73

April 2013 – 133 (Up 82.2% YOY, Up 79.7% Two Year)

open houses are packed to capacity

I don’t see this. My husband and I still go to open houses and we see a couple of other people there, but it is nothing compared to what we went through in early 2000’s. We actually waited on line for 20 minutes to get in. Many times the house would get sold while we were on line.

Do they get to open houses? Tried to set up a showing yesterday afternoon, only a day or two on the market. Listing agent said don’t bother, they already have 5 solid offers.

That said, there is a lot of inventory making its way to market over the past 2-3 weeks, a *LOT*.

Then there are obviously a bunch of fools buying now..you will never get me to believe that 5 years after a complete crash, everyone has great credit, down payments, job(s) and nothing else to sell. Inventory has been low but it can’t stay low forever. Too many boomers need to get out of dodge and away from 20K tax bills. If you are getting into a bidding war then you are a bigger fool. Market mouths trying to push a frenzy and idiots are buying it hook, line and sinker. “They’re not making more homes..hurry now”. Grim, you may think that buyers are more saavy today but I think bubble may be back. Their is absolute irrationality going on right now.

There, I meant

Ahhhhh — that is the sound of me jumping into my pool this morning…

Doom is nigh. Prepare accordingly.

grim [6],

My master plan is working [insert evil scientist laugh here]. :)

Doom has been postponed until further notice due to sunshine, nice weather and happy people. We apologize for the delay…

Suck in all the sheep, then slam the exits shut.

Great good fun.

Any questions?

“The shockingly anemic pattern of post-crisis US consumer demand has resulted from a deep Japan-like balance-sheet recession. With the benefit of hindsight, we now know that the 12-year pre-crisis US consumer-spending binge was built on a precarious foundation of asset and credit bubbles. When those bubbles burst, consumers were left with a massive overhang of excess debt and subpar saving.

The post-bubble aversion to spending, and the related focus on balance-sheet repair, reflects what Nomura Research Institute economist Richard Koo has called a powerful “debt rejection” syndrome. While Koo applied this framework to Japanese firms in Japan’s first lost decade of the 1990’s, it rings true for America’s crisis-battered consumers, who are still struggling with the lingering pressures of excessive debt loads, underwater mortgages, and woefully inadequate personal saving.

Through its unconventional monetary easing, the Fed is attempting to create a shortcut around the imperative of household sector balance-sheet repair. This is where the wealth effects of now-rebounding housing prices and a surging stock market come into play. But are these newfound wealth effects really all that they are made out to be?

Yes, the stock market is now at an all-time high – but only in current dollars. In real terms, the S&P 500 is still 20% below its January 2000 peak. Similarly, while the Case-Shiller index of US home prices is now up 10.2% over the year ending March 2013, it remains 28% below its 2006 peak. Wealth creation matters, but not until it recoups the wealth destruction that preceded it. Sadly, most American households are still far from recovery on the asset side of their balance sheets.

Moreover, though the US unemployment rate has fallen, this largely reflects an alarming decline in labor-force participation, with more than 6.5 million Americans since 2006 having given up looking for work. At the same time, while consumer confidence is on the mend, it remains well below pre-crisis readings.

In short, the American consumer’s nightmare is far from over. Spin and frothy markets aside, the healing has only just begun.”

http://www.project-syndicate.org/commentary/america-s-over-hyped-consumer-recovery-by-stephen-s–roach

Fast,

Only you can appreciate this- back from showings and 3 houses under 1600 sq ft, ikea updates, with front views of 95, two with no garage or central air. All this for 600k not to mention 80m commute to Grand central. This is Fairfield,CT. Sure, no bubble going on..What savvy buyer will step up.

Plenty of dumb buyers- flush with little green pieces of Bernank- will step up.

From Zillow:

Zillow: April Case-Shiller Composite To Show Annual Appreciation Above 12%

Buckle up, folks. If you thought the Case-Shiller numbers out this morning for March were eye-popping, just wait until next month. Our updated forecast indicates that the April 20-City Composite Case-Shiller Home Price Index (non-seasonally adjusted [NSA]) will rise 12.1 percent on a year-over-year basis, while the 10-City Composite Home Price Index (NSA) will increase 11.4 percent from year-ago levels. The seasonally adjusted (SA) month-over-month change from March to April will be 1.7 percent for both the 20-City Composite and the 10-City Composite Home Price Indices (SA). All forecasts are shown in the table below. Officially, the Case-Shiller Composite Home Price Indices for April will not be released until Tuesday, June 25.

It looks like a housing recovery

http://www.njherald.com/story/22463267/2013/05/30/it-looks-like-a-housing-recovery

Posted: May 30, 2013 9:40 PM EDT

Updated: May 30, 2013 9:40 PM EDT

In the last six years, along with wildfires, floods and tornadoes, has come another spring tradition — the spring slowdown, slump or swoon. Choose your own noun. What seemed to be a healthy late-winter recovery suddenly ground to a near-halt.

Analysts were expecting a repeat this year, but an unexpected thing happened on the way to the swoon: the ailing housing market took off. “Take off” may be too strong a description, but trust us: Good things happened, good enough to power the economy through the swoon.

Home prices surged in the first quarter at their fastest pace in nearly seven years. Prices in March rose 10.2 percent from a year earlier, according to the authoritative Standard & Poor’s/Case-Shiller Index, the largest annual gains since 2006, when home prices began to go over the cliff. The report sent the Dow Jones to a new high.

Prices are a function of supply and demand, and the supply is not great. Wary homebuilders haven been cautious about launching major new projects. Homeowners with their houses under water — i.e., they owe more on the house than it is worth — or facing foreclosure have decided to tough it out to see if the economy improves.

They may be right. Despite a 2 percent increase in the payroll tax and severe cuts in federal spending, personal consumption is up 1.2 percent and consumer confidence is at five-year high.

But excuse us if we don’t break out the champagne and begin flinging confetti. The pickup in housing could cause the Fed to reassess its easy money policies and its $85 billion-a-month asset-buying program. As the housing market picks up, mortgage rates will unavoidably rise.

The full impact of the federal sequester — the planned steep cuts in federal spending — has yet to be felt. We might suffer sympathy pains from slowdowns in the Chinese and European markets. We may feel that we’ve learned our lessons from the last housing bubble and that the new, and untested, financial-watchdog agencies created during the recession will be standing guard.

But consider: Home prices are down 28 percent from 2006 and have returned to their 2003 levels. But signs of improvement and recovery are definitely there. We’ll keep the champagne on ice and the confetti close at hand — just in case, mind you.

Scripps Howard News Service

I saw a house in Chadds Ford that I liked but didn’t love. Wife felt the same. We felt it was a good house, great with some work and it had an awesome location. We felt it was overpriced though. I knew the comps and they didn’t support the 559k asking price. Just came on three days ago.

Already has two offers but I know that they were under asking. Our agent is the Listing agent and I already told her that I wouldn’t trust her. She laughed and said she already knew that about me because I told her I didn’t trust realtors.

Still mulling an offer. I may come in under but waive mortgage contingency.

More grandparents keeping childcare all in the family.

http://www.nj.com/news/index.ssf/2013/06/grandparents_now_provide_child.html

Retired Grandparents staying in NJ and their kids moving near them.

Jean Shelby reads a story with her grandson Jude Pingree, whom she takes care of after preschool, recently in Maplewood. The former Ohio resident retired to Florida, then did a âreverse retirementâ to move back north once her daughter had a son.

John Munson/The Star-Ledger

Drove up to Alpine through a lot of Bergen County today for a soccer game. I just don’t get what the attraction Bergen County is. Unless one loves traffic.

Can’t imagine any good footballers in Alpine.

It an amazing piece of writing for all the internet visitors; they will get advantage from it I am sure.

tFmahaDn

tFmahaDn http://www.r74u8sNmd8GfFnU09g50m2.com/

[url=http://www.r74u8sNmd8GfFnU09g50m2.com/]tFmahaDn[/url]

かつて私 コメント時間|されている付加チェックボックスと今毎各 最初に私は新しいフィードバックはコメントは私を通知をクリックしたコメントした私が追加されますコメント| 同じと同じメール| 4 4を得る。 私に、そのサービスからの|は奪う削除?あなたはありあなたがすることができるでしょうそこにはanyですありがとう!

I like the helpful information you provide in your articles. I will bookmark your weblog and check again here regularly. I am quite certain I’ll learn a lot of new stuff right here! Good luck for the next!

449540 178935Really fascinating information !Perfect just what I was looking for! 129477