Now Open, Part II!

Prior weekend thread closed due to comment overflow.

Now Open, Part II!

Prior weekend thread closed due to comment overflow.

From the Hartford Courant:

Homeowners started losing hold of their homes years before spiking foreclosures and the housing slump slammed the economy.

Piece by piece, some gave away their homes by tapping equity to take cash out to pay for cars, weddings and vacations. Others never owned one brick. During the country’s most recent housing boom, the term “homeowner” became a misnomer as lenders offered 100 percent or more home financing to some buyers.

Now, slipping home prices threaten to further erode the value of many Americans’ single largest asset, curbing consumer spending and jeopardizing retirement assets.

Thanks in large part to mortgage-related tax deductions and a drumbeat of advice that everyone should own their home, the U.S. homeownership rate rose steadily in recent decades. It peaked at 69.2 percent in 2004 before backing down to 68.2 percent at the end of the third quarter, according to the Census Bureau, which has collected the data since 1965.

But that small decline masks a much larger plunge in the amount of equity homeowners hold. This figure, equal to the percentage of a home’s market value minus mortgage-related debt, fell to an average of 51.7 percent at the end of the second quarter, down from 62 percent at the end of 1990, the Federal Reserve reported, even as the average home value surged 139 percent during that period.

The drop in average value is particularly bad news for homeowners who treated their homes as piggy banks instead of as savings accounts. They drained $468.7 billion out of their homes in 2004 through home equity loans or cash-out refinancings, according to a report this year from former Fed Chairman Alan Greenspan and Fed senior economist James Kennedy. Fifty-eight percent of that cash went to home improvements and personal spending, while another 27 percent paid off credit card debt.

…

They felt confident that housing prices would continue to rise, replenishing the equity they took out.“To deal with your single biggest asset like that is risky,” said Jim Gaines, research economist at The Real Estate Center at Texas A&M University. “Those things should be paid for by current earnings, not savings, which is what your house is.”

From the Record:

Builders cutting prices to cut deals

How much would a buyer pay for a new house in Ramsey, with three bedrooms, 3½ bathrooms, a stone facade and high-end finishes such as crown molding and stainless steel appliances?

Mike Karvellas of Grace Michael Builders in Allendale, who built the house, used to think the answer was $759,000. But after the house sat on the market for months, Karvellas cut the price again and again. He finally sold it for $659,000 — a price that wiped out his profit. But at least he will no longer be burdened by the property’s carrying costs, such as taxes and loan interest, of more than $5,800 a month.

“I’d rather get rid of it and get out from underneath my investment,” Karvellas said.

As Karvellas’s experience shows, the market for new homes has changed radically since the boom times of 2004 and 2005. While North Jersey builders have not suffered as much as their colleagues in distressed markets such as Florida, many are being forced to cut prices and delay new projects.

According to the National Association of Home Builders, builders’ confidence in the housing market is at the lowest point since the group began measuring it in 1985.

…

North Jersey builders face high costs for land, building materials and fuel. And they’re paying higher interest on bank loans — 8 percent and up, compared with less than 5 percent a few years ago. While builders can make profits of 20 percent or more during good times, that’s far from a sure thing these days.

…

There have been dramatic price cuts. In Norwood, a subdivision of three new houses went on the market earlier this year for $1.2 million to $1.4 million. Two of the three sold for more than $300,000 off the original asking price; the third is on the market for more than $400,000 off the initial price.

…

Still, many potential buyers aren’t taking the bait yet. Many believe that prices may have further to fall — or, at the very least, that they won’t rise much for a while. A number of national housing economists and analysts agree, predicting that prices and the pace of sales won’t pick up until 2009 or later.“Now, there’s so much supply that buyers are saying, ‘It’s a nice house, I really like it, but I don’t know, I’ll wait and see,’ ” said Richie Wells, president of the Builders and Remodelers Association of Northern New Jersey. He is the head of Team Construction and Team Remodeling Inc. of Mahwah.

“There’s no sense of urgency whatsoever,” said Murad. “That’s the new market right now.”

This is the time and place to post observations about your local areas, comments on news stories or the New Jersey housing market, open house reports, etc. If you have any questions you wanted to ask earlier in the week but never posted them up, let’s have them. Also a good place to post suggestions, requests for information, criticism, and praise.

For readers that have never commented, there is a link at the top of each message that is typically labelled “[#] Comments“. Go ahead and give that a click, you might be missing out on a world of information you didn’t know about. While you are there, introduce yourselves to everyone.

For new readers that have only read the messages displayed on the main page, take a look through the archives, a substantial amount of information has been put online in the past year. The archives can be accessed by using the links found in the menus on the right hand side of the page.

From Inman News:

2008 not so great, says builders’ economist

Single-family housing starts are expected to plummet 29.3 percent this year compared to 2006, and to drop another 23.6 percent in 2008, National Association of Home Builders chief economist David Seiders said in a forecast report Thursday.

Seiders expects house values to fall about 10 to 15 percent from the peak of the boom to the low point in the downturn, with further price erosion next year. He said the price declines should ease some housing-affordability problems.

“This year has turned out to be much weaker than I had expected a year ago,” he said, and he blamed the “progressive meltdown of the housing finance system” for the housing market’s unexpected rate of decline.

“The probability of recession has probably increased fairly significantly in a short period of time,” and Seiders said he estimates a 40 percent chance that the economy will sink into recession in the next two quarters.

“We really are right now in a danger zone in terms of overall economic activity. I think it’s fair to say that the overall economy is slowing pretty dramatically in the fourth quarter.”

Single-family housing starts are projected to drop about 53.7 percent from an annual peak of 1.72 million in 2005 to an anticipated low of 796,000 in 2008 before recovering to 885,000 starts in 2009.

Single-family new-home sales peaked at a record 1.28 million in 2005 and are expected to bottom out at 741,000 in 2008, and then to rise to 838,000 in 2009.

New-home sales dropped 18 percent from 2005 to 2006, and are projected to fall 24.4 percent this year compared to last, drop 6.6 percent in 2008 and rise 13.1 in 2009.

And the builders’ group expects single-family sales of previously owned homes to drop 13.3 percent this year compared to 2006, to a total of 4.95 million. That follows a 7.7 percent year-over-year drop in 2006. Seiders also expects a 13.4 percent year-over-year drop in 2008 and an 8.4 percent rise in single-family resale home sales in 2009.

From the Wall Street Journal:

Fraud Seen as a Driver In Wave of Foreclosures

Atlanta Ring Scams Bear Stearns, Getting $6.8 Million in Loans

By MICHAEL CORKERY

December 21, 2007; Page A1

Skyrocketing foreclosures are a testament to how easy it was to borrow from mortgage lenders in recent years.

It may also have been easy to steal from them, to judge from a multimillion-dollar fraud scheme that federal prosecutors unraveled here in Atlanta. The criminals obtained $6.8 million in mortgages from Bear Stearns Cos., including a $1.8 million mortgage to Calvin Wright, a New Yorker who told the investment bank that he and his wife earned more than $50,000 a month as the top officers of a marketing firm. Mr. Wright submitted statements showing assets of $3 million, a federal indictment alleged.

In fact, Mr. Wright was a phone technician earning only $105,000 a year, with assets of only $35,000, and his wife was a homemaker. The palm-tree-lined mansion they purchased with Bear Stearns’s $1.8 million recently sold out of foreclosure for just $1.1 million. Bear Stearns, meanwhile, posted the first quarterly loss in its 84-year history as it wrote down $1.9 billion of mortgage assets yesterday. (See related article.)

Fraud goes a long way toward explaining why mortgage defaults and foreclosures are rocking financial institutions, Wall Street and the economy. The Federal Bureau of Investigation says the share of its white-collar agents and analysts devoted to prosecuting mortgage fraud has risen to 28%, up from 7% in 2003. Suspicious Activity Reports, which many lenders are required to file with the Treasury Department’s Financial Crimes Enforcement Network when they suspect fraud, shot up nearly 700% between 2000 and 2006.

In 2006, losses from fraud could total a record $4.5 billion, a 100% increase from the previous year, says Arthur Prieston, chairman of the Prieston Group, which provides lenders with mortgage-fraud insurance and training. The surge ranges from one-off cases of fudging and fibbing to organized criminal rings. The FBI says its active mortgage-fraud cases have increased to 1,210 this year from 436 in 2003. In some regions, fraud may account for half of all foreclosures. “We’ve created a culture where a great many people know how to take advantage of the system,” says Mr. Prieston.

…

Yet the system itself bears blame. The evolution of mortgages into a securities instrument turned loan origination into a competition. Caution gave way to a push for speed and volume. Embroiled in an all-out war for market share, issuers reduced barriers to credit, for example, by offering so-called “stated-income” loans, which require no proof of income. “The stated-income loan deserves the nickname used by many in the industry, the ‘liar’s loan,’ ” says the Mortgage Asset Research Institute, which works with lenders to prevent fraud. A recent review of a sampling of about 100 stated-income loans revealed that almost 60% of the stated amounts were exaggerated by more than 50%, MARI says.

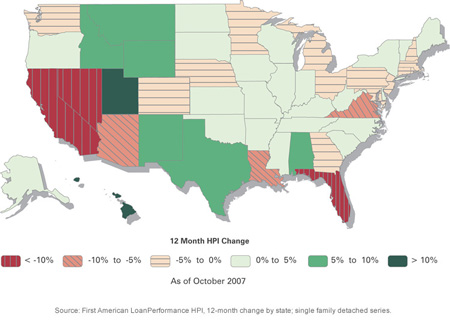

From LoanPerformance:

First American LoanPerformance Releases October 2007 House Price Index

12 Month Change By Top 30 CBSAs (Core Based Statistical Areas) As of October 2007

Honolulu, HI 17.91%

Salt Lake City, UT 11.63%

Austin-Round Rock, TX 8.62%

San Antonio, TX 7.89%

Raleigh-Cary, NC 4.56%

Houston-Sugar Land-Baytown, TX 4.52%

Charlotte-Gastonia-Concord, NC-SC 4.47%

Dallas-Fort Worth-Arlington, TX 3.92%

Seattle-Tacoma-Bellevue, WA 2.18%

Portland-Vancouver-Beaverton, OR-WA 1.73%

Chicago-Naperville-Joliet, IL-IN-WI -0.22%

Philadelphia, PA -0.61%

New York-Northern New Jersey-Long Island, NY-NJ-PA -1.83%

Atlanta-Sandy Springs-Marietta, GA -2.13%

St. Louis, MO-IL -2.76%

Detroit-Warren-Livonia, MI -3.16%

Minneapolis-St. Paul-Bloomington, MN-WI -3.33%

New York-White Plains-Wayne, NY-NJ -4.13%

Miami-Miami Beach-Kendall, FL -4.85%

Boston-Quincy, MA -6.01%

Cleveland-Elyria-Mentor, OH -8.10%

Washington-Arlington-Alexandria, DC-VA-MD-WV -8.11%

Tampa-St. Petersburg-Clearwater, FL -9.21%

Phoenix-Mesa-Scottsdale, AZ -10.08%

Orlando-Kissimmee, FL -10.16%

Los Angeles-Long Beach-Santa Ana, CA -10.45%

Miami-Fort Lauderdale-Miami Beach, FL -10.89%

Oakland-Fremont-Hayward, CA -11.44%

Las Vegas-Paradise, NV -11.65%

Cape Coral-Fort Myers, FL -14.01%

Riverside-San Bernardino-Ontario, CA -15.70%

Source: First American LoanPerformance HPI, Single Family Detached Series

From the Associated Press:

US Foreclosure Filings Rose in November

S. homeowners increasingly failed to keep up with their home loan payments in November, as the number of foreclosure filings surged 68 percent nationwide compared with the same month a year ago, according to a mortgage research company.

In all, 201,950 foreclosure filings were reported last month, compared with 120,334 in November 2006, Irvine-based RealtyTrac Inc. said Wednesday.

Last month’s filings fell 10 percent from October’s 224,451.

The last time there was a sequential drop in foreclosure filings was between August and September, when they fell 8 percent.

“It’s a little bit of good news in the otherwise murky real estate market right now,” said Rick Sharga, RealtyTrac’s vice president of marketing. “The fact that we’re seeing a 10 percent decrease is significant. It’s a good thing.”

The U.S. had one foreclosure filing for every 617 households in November, RealtyTrac said.

The filings include default notices, auction sale notices and bank repossessions. Some properties might have received more than one notice if the owners have multiple mortgages.

Forty-three states saw an increase in foreclosure filings over last year.

The decline in filings from October to November likely corresponds with a lull in adjustable-rate mortgage resets, Sharga said.

…

We’ll see another fairly big spike in (foreclosure) filings in early ’08,” Sharga said. “Then there’s another group of loans that’s due to reset in May and June, so we’ll see another wave of defaults probably in the fall.”Experts estimate some 2 million adjustable-rate mortgages are due to reset at higher rates in the next seven months.

From Dow Jones:

Home Builder Hovnanian Reports Quarterly Loss

Hovnanian Enterprises Inc. late Tuesday reported a widened fourth-quarter loss, as home builders continue in vain to search for a bottom in the residential housing market.

The Red Bank, N.J.-based company (HOV) said its net loss for the period ended in October increased to $466.6 million, or $7.42 a share, from $115.3 million, or $1.88 a share in the same period a year earlier. Meanwhile revenue fell to $ 1.39 billion, from $1.75 billion.

Hovnanian said it incurred a total of $383 million in pretax charges including land and intangible impairments. The company said similar charges in the same period a year earlier totaled $322 million.

…

Last month, when Hovnanian released preliminary fourth-quarter results, it said net contracts in the company’s fourth quarter dropped 10% from a year earlier, saying its October sales pace in most markets “significantly deteriorated” in relation to recent months.Hovnanian delivered 19% fewer homes during the October quarter compared to the year-earlier period. The cancellation rate rose quarter-over-quarter to 40% of gross contracts, up from 35%.

Heading into Tuesday’s trading session, Hovnanian shares were down more than 76% so far this year, falling harder than the broader home-builder group. The housing downturn has been particularly cruel to builders like Hovnanian with significant operations in hard-hit Florida and California

…

Ara Hovnanian, the company’s CEO, at an investment conference last month said U.S. housing won’t likely get back to a “balanced marketplace” until 2010. Meanwhile, 2008 will be “another challenging year” and he was not looking for strong earnings from home builders.“By the tail end of 2008 we should get some positive momentum in sales, setting up a recovery in 2009,” Hovnanian said. Home builders by then should return to profitability, although earnings will be more meager than the recent boom years, the CEO said.

From the Record:

Subprime woes take toll on regional banks

Valley National Bancorp Chief Executive Officer Gerald Lipkin thinks regional banks such as his are being unfairly punished by investors anxious over subprime mortgage writedowns at large banks. Shares at Valley have fallen 25 percent this year.

“The big banks blundered trying to show analysts how fast they can grow,” said Lipkin, the longtime head of Wayne-based Valley. “We don’t have any subprime loans, and most of my contemporaries have little or none on their books.”

However, there may be more anxiety ahead for Valley.

…

Many lenders have been hard-pressed to increase earnings as more subprime loans go bad, the housing market stumbles and the ability of lower-risk borrowers to pay back loans becomes a concern.Valley is not insulated from some of those concerns, although the Keefe Bruyette analysts acknowledged the bank’s conservative lending practices in their report. They predicted the bank will do “relatively well [next year] from a loss perspective.”

But they expect Valley will still have to set aside more funds in a loan-loss reserve, which will cut into profits.

…

Valley, the largest commercial bank based in North Jersey, earned $125.6 million in the first nine months of this year, unchanged from the same period in 2006.Loan charge-offs rose in that period to $9.7 million from $7.6 million in the previous year.

…

Citigroup analyst Keith Horowitz — who does not cover Valley — on Friday reduced ratings on most of the banks he follows, citing an “increasingly difficult environment.”PNC Financial Services Group, which has little subprime exposure, was lowered to a “hold” rating. Pittsburgh-based PNC recently warned that fourth-quarter earnings would be less than previously thought because of a drop in the value of commercial real estate loans.

From the Associated Press:

Fed to Unveil Home Mortgage Plan

Federal Reserve plan being unveiled Tuesday would give people taking out home mortgages new protections against shady lending practices.

The rules to be proposed are especially geared to providing some future safeguards to the riskiest “subprime” borrowers, already painfully stung by the housing and credit debacles. The proposal is expected to apply to new, or future, loans made by all types of lenders, including banks and brokers. The plan could be finalized next year.

The Fed, which has regulatory powers over the nation’s banking system, is considering:

_barring or restricting lenders from penalizing subprime borrowers — those with tarnished credit or low incomes — who pay their loans off early.

_forcing lenders to make sure that borrowers, especially subprime ones, set aside money to pay for taxes and insurance.

_barring or limiting loans that do not require proof of a borrower’s income.

_setting new standards for how lenders determine a borrower’s ability to repay a home loan.

Fed policymakers also will look into improving financial disclosures so people better understand the terms and conditions of their mortgages. It will consider ways to crack down on misleading mortgage advertising.

…

The plan, if ultimately adopted, offers Federal Reserve Chairman Ben Bernanke, who took over the helm in February 2006, an important opportunity to put his imprint on the Fed’s regulatory powers. Some critics have complained that Bernanke’s predecessor — Alan Greenspan, who ran the Fed for 18 1/2 years — failed to act as a forceful regulator especially during the 2001-2005 housing boom, where easy credit spurred lots of subprime home loans and many exotic types of mortgages.

From Bloomberg:

`Deal With Devil’ Funded Carrera Crash Before Subprime Shakeout

One week in 2002, Daniel Sadek was $6,000 short of covering the payroll for his new subprime mortgage company, Quick Loan Funding Corp. So he flew to Las Vegas and put a $5,000 chip on the blackjack table.

“I could have borrowed the money, I suppose,” Sadek says.

That wouldn’t have been his style. With his shoulder-length hair and beard, torn jeans and T-shirts with slogans such as “Where is God?” Sadek looked more like a guitarist for Guns N’ Roses than a mortgage banker.

Sadek says he was dealt a jack, then an ace. Blackjack. He would make payroll. Quick Loan Funding, based in Costa Mesa, California, would survive and, for a while, prosper as one of 1,300 mortgage lenders in the state vying to satisfy Wall Street’s thirst for subprime debt.

As home prices rose and hunger for high-yield investments grew, Sadek found his niche pushing mortgages to borrowers with poor credit. Such subprime home loans grew to $600 billion, or 21 percent, of all U.S. mortages last year from $160 billion, or 7 percent, in 2001, according to Inside Mortgage Finance, an industry newsletter. Banks drove that growth because they could bundle subprime loans into securities, parts of which paid interest as much as 3 percentage points higher than 10-year Treasury notes.

“I never made a loan that Wall Street wouldn’t buy,” Sadek says. He worked hard to build the business, he says, and the company did nothing illegal.

…

Loan officers were hired and fired all the time at Quick Loan Funding’s 26,000-square-foot call center in Irvine, says Bryan Buksoontorn, who joined the company in 2004. By then, Irvine had become a hotbed of subprime lending companies.“We were motivated by fear,” says Buksoontorn, 28, who is now an independent mortgage broker. “It was a boiler room. You had to make your numbers.”

Buksoontorn’s job: get the caller’s credit card and charge $475 for an appraisal, he says.

“You told the callers what they wanted to hear and you got the credit card,” says Steven Espinoza, 39, an employee from 2003 to 2005.

…

Sadek and his managers would berate the sales staff, many of whom had no experience or training, Buksoontorn says.“They would get in your face,” he says. “`Why aren’t you ordering appraisals? Why aren’t you selling?’ ”

Sadek brought a car salesman’s mentality to mortgages, Espinoza says.

“It’s the same type of hard sell,” Espinoza says. “Close ’em, close ’em, close ’em.”

…

Sadek says 95 percent of Quick Loan Funding’s mortgages were made to subprime borrowers.“If we had a prime borrower on the line, we hung up on them,” Buksoontorn says. “We were geared toward subprime because they were easier to close. We were giving them money no other bank would dare to give them.”

…

Sadek says that with the support of Citigroup, which funded the loans, he pioneered lending to homebuyers with credit scores of less than 450.Citigroup spokesman Stephen Cohen said the bank doesn’t comment on its relationships with clients.

“We made most of our money from selling loans to banks,” Sadek says.

Quick Loan Funding, like many subprime companies, specialized in 2/28 loans — 30-year mortgages that start with lower “teaser” interest rates and ratchet higher after two years.

…

It wasn’t a lie. Year over year, prices hadn’t fallen since the 1930s, according to the Realtors group. The belief that values would form a stairway even seduced Quick Loan Funding employees who took out 2/28 loans themselves, says Marcus Bednar, 32, a former sales manager.(no relation, -jb)

“They believed everything the borrowers believed, that the market was going to go up,” Bednar says. “It wasn’t just something we were pushing because we tried to rip people off.”

Bednar adds, “We were never encouraged to do anything shady.”

…

To get $20,000 in cash from the Quick Loan Funding refinance, Aultman was told, his monthly payments would rocket to $2,264 from $1,464.“I said I can’t do this,” Aultman says. “They said take the mortgage, make the payments and once everything is paid off, within 30 days your credit will shoot up 150 points and we’ll get you a better rate and everybody wins.”

…

Aultman says he didn’t see the pre-payment penalty in his contract. If he refinanced within two years, he’d have to pay six months interest.He also says he didn’t notice his income on the contract: $5,950 a month. At the time Aultman says he made $3,420.

…

For a $247,500 mortgage, Aultman paid Quick Loan Funding $10,813, including origination fee, application fee, processing fee, underwriting fee and quality control fee, according to his loan documents.The average closing costs for a mortgage of that amount in California is about $5,000, according to Pete Ogilvie, president of the California Association of Mortgage Brokers.

…

Sadek may be in trouble, too. The California Department of Corporations wants to revoke his lending license. The state says he tried to use the bank account of his escrow company, Platinum Coast, to apply for markers, or gambling loans, at three Las Vegas casinos in April and May.“It was a bank error,” Sadek says. “No money ever left the account.”

Sadek holds up a copy of the marker application. It has his name at the top and his signature at the bottom. In the middle of the page is a bank-account number. He says he thought it was his personal account. It wasn’t. It turned out to be Platinum Coast’s, Sadek says.

He says he didn’t know what he was signing.

From the Wall Street Journal:

Mortgage-Relief Plan Divides Neighbors

Protection Is Spotty In Southern California; The Oropezas Pack Up

By JONATHAN KARP

December 17, 2007

A mortgage-relief plan being pushed by the government is supposed to help debt-laden homeowners across America. But it’s creating dashed hopes and fresh tensions in this city that mushroomed during the subprime-lending boom.

Shannon Kelly was excited when she first heard about the plan, rushing to tape a TV news report about it. But her hope of escaping a sinkhole of debt was short-lived: Her adjustable-rate mortgage doesn’t qualify for a bailout under the terms outlined by the Bush administration and the mortgage industry.

Across town, in a condominium development riddled with foreclosures, there was holiday cheer for Karey Kelly, who is no relation. With monthly payments on her $351,000 mortgage set for a punishing rise in January, the single mother already had applied for an extension of her rate when the government-backed initiative was unveiled. Her credit score is on the cusp of the limit, but “I’m pretty positive that I meet the plan’s criteria,” Ms. Kelly says.

The Bush administration has touted the plan, announced this month, as a potential lifeline for hundreds of thousands of subprime borrowers, as well as a means to cushion the economy from the mortgage meltdown. Supporters say the proposal to freeze interest rates for certain buyers and accelerate loan refinancing for others aims to target deserving debtors and avoid aiding those who really can’t afford their homes. Congress joined the rescue effort last week, passing legislation to help borrowers with mortgages up to $417,000 to secure refinancing.

Yet Southern California, an epicenter of foreclosures, poses a particularly tough challenge because of the mix of adjustable-rate loans and high home prices that put many mortgages above the ceiling for government guarantees. The relief efforts so far have been met with skepticism.

The prospect of aid for some borrowers, but not others, brings another layer of discord to neighborhoods already racked by plummeting home values, rising bank repossessions and vacant houses whose owners simply up and left.

…

Incentives and adjustable-rate mortgages got first-timers into homes without any down payment and enabled refinancing. Many who refinanced drained their equity, betting that home values would keep soaring. Now tens of thousands of homeowners are exposed to unaffordable interest rates and a sluggish resale market.Corona lawyer Nathan Fransen says he has nearly 100 clients trying to avoid foreclosure but none appear eligible for the rescue package. “The government has misread California. Most foreclosures here are on loans that haven’t adjusted, meaning that people can’t afford what they have now,” says Mr. Fransen. He lives in a gated community where he says dozens of million-dollar homes face foreclosure. “The plan won’t help much here, and the problem is going to get worse.”

From the Journal News:

The tales of woe keep coming. A Peekskill woman overspends fixing up a condominium; she puts it on the market just as real estate sales slow. Now she can’t sell or repay the debt. Then there’s the couple in Cold Spring that was confused or, perhaps, misled, by the terms of their mortgage refinancing. They now owe more than their house is worth. In Pomona, a family facing illness and in need of a quick cash infusion shops for a modest loan, but sees their 6 percent fixed-rate mortgage morph into an adjustable-rate mortgage of more than 9 percent. The new rate now makes the home unaffordable.

…

The numbers of new foreclosures this year in Westchester, Putnam and Rockland counties are staggering. As of November, there were 1,975 foreclosure filings in Westchester, an increase of 38 percent over the previous year. In Rockland, there were 1,045 filings as of October, an increase of 16.2 percent; and in Putnam, foreclosure filings increased by a whopping 44.3 percent as of October, some 368 homes in all. Each of those represents immeasurable family disappointment, fear and, ultimately, upheaval.As staff writer Jerry Gleeson noted in an article yesterday, more than 6.2 million homeowners nationwide took the gamble with subprime mortgages, about half of which were adjustable-rate mortgages. Economists now predict that about half of the subprime mortgage holders – or 3 million homeowners – could default on their loans.

Massive defaults threaten the financial services industry and even unrelated companies that traded in real estate holdings. Add to that the rippling effect of job losses – the related layoffs are coming now to Wall Street and our Main Streets and it explains why federal and state officials are rushing to help. Foreclosed properties undermine the value of even unrelated property. Accordingly, even secure property owners and even renters in mortgaged property – have a stake in seeing troubled homeowners stay above water.

…

But these will be too little, too late for many borrowers already in arrears. They required help on the front end – from watchdog regulators and a mindful Congress. We are now seeing that they truly were on their own.

Subprime disaster: Lenders, borrowers face new requirements

For mortgage brokers, a more complex future looms.

A raft of legislation at the federal and state levels is seeking to prevent a recurrence of the conditions that have led to sharp increases in mortgage delinquencies and foreclosures across the nation.

One common denominator in many of the bills is greater regulation of the mortgage broker industry. Critics have accused brokers of recklessly drawing consumers into loans they couldn’t afford in the interest of obtaining the higher commissions that subprime mortgages commanded.

“They clearly were steering people into the subprime market who couldn’t afford to be there in the first place, or in any mortgage market,” said state Sen. Jeffrey Klein, D-Bronx, whose district includes portions of southern Westchester.

Klein has introduced a bill that calls for mandatory consumer education for borrowers using subprime mortgages. The bill also calls for a fiduciary responsibility between brokers and consumers.

“When someone sits down with a mortgage broker, they should be able to breathe easy that that person has their best interests in mind and is going to put them into a mortgage that they can afford,” Klein said. “I think that’s key.”

…

The question of how the state would define the brokers’ fiduciary responsibility to consumers is a concern to him. The bonding requirement in New York already serves as a powerful deterrent to misbehavior, Soliz said, because the inability to get bonded would put a brokerage out of business.That lenders were willing to offer loans for 100 percent of the cost of homes, and without income verification, is overlooked when blame is being assigned to the mortgage brokers, Soliz said.

“This industry has been used as a scapegoat. They provided the liquidity. They provided the securities,” he said. “If you don’t have the product to sell, you couldn’t have sold it.”

…

But it is harder now for first-time homebuyers to enter the market, he added.“I’m not saying people have to put 20 percent down. But certainly the days of putting nothing down are gone,” he said.

Pomona man trusted refi deals, now may lose home

Since Mario Dorelien can remember, he has worked hard for everything. No handouts or wealthy parents here, he says with his rich trademark laugh. His four-bedroom home with front and back yards, two children in college and another working his way there, all came by the sweat of his brow.

That’s why it’s all the more frustrating to him that it may all end as if none of that mattered – that the tortoise and the hare meet the same fate.

In the coming months Dorelien may lose his home to foreclosure, and with it the respect of his wife and children. Dorelien says a shark-like mortgage broker steered him toward a subprime mortgage that has threatened to put his family on the street.

Peekskill mom dreams of escaping subprime mortgage

Once upon a time, Judy Becker owned a spacious house in Croton-on-Hudson, with plenty of room for herself, her husband, two children and their pets.

After a divorce slashed her budget, she settled for a cramped condominium in Peekskill and began looking for her first full-time job in decades.

Now, the 60-year-old risks losing even her downsized dreams, as payments on her subprime mortgage rise beyond her means and a yearlong effort to sell her two-bedroom townhouse has yielded no offers.

“I accepted an adjustable-rate mortgage, thinking, ‘I’ll only be here a few years, it’s just a place to land,’ ” she explained. “But then, the real estate market fell apart, and things just stopped selling.”

Now Open, Part II!

Prior weekend thread closed due to comment overflow.