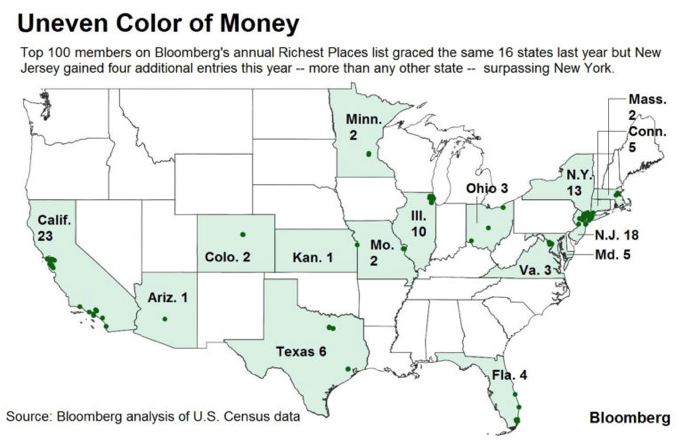

From Bloomberg:

Nick Boniakowski’s clients bought a home in Northern New Jersey in 2016. Now they want to move again.

They found a house they liked. It wasn’t the charm of new construction, an upgrade in location, better schools or a swimming pool that attracted them.

It was the lower property taxes.

Like many of Boniakowski’s clients at Redfin Corp.’s Hoboken office, these two are looking at their returns for the first time since President Donald Trump’s tax changes took effect and, despite more than a year of lead time, experienced a mild freakout. Maybe buying a new house –- the rare financial ordeal that’s more maddening than the annual April 15 ritual –- could be the solution.

….

The Tax Cut and Jobs Act promised to, well, cut taxes. For many, it does. But a new limit on the amount of state and local levies that can be deducted has costly and confounding implications for some, especially in high-income-tax, high-property-tax places like the New York City area.

Nearly 11 million taxpayers will be affected by the new cap on so-called SALT deductions on the taxes they file this year, and could lose out on a cumulative $323 billion, according to a February estimate from the U.S. Treasury Inspector General for Tax Administration.

For those people, the April 15 deadline carries a greater sense of dread than usual. New rules include a higher standard deduction and changes to the Alternate Minimum Tax, and it can be hard to say, even for experts, how they’ll affect individuals until they file.

The situation wasn’t made any simpler by state lawmakers, who argued that the cap on the SALT deduction was intended to hurt states that tend to elect Democrats, and concocted a series of elaborate workarounds that were shot down by the Internal Revenue Service.

People with more money and thus more complicated tax returns tend to file later in the season, meaning that the triggering has just begun.

“A lot of my clients are very surprised by what’s happening,” said Ann Callari, tax partner at RotenbergMeril, an accounting firm in Saddle Brook, New Jersey. “That’s the nature of taxes. People hope for the best and don’t pay attention. They don’t notice until it affects them.”

In the meantime, plenty of taxpayers are expecting the worst.