hiladelphians Luis Valenti, 25, and Eleonora Barbieri, 26, are getting married July 14.

If planning a wedding doesn’t seem stressful enough, the couple are settling July 10 on their first house, a duplex in the 2200 block of West Thompson Street listed at $155,000.

Two major events in the lives of anyone, and just four days apart.

“With the housing recovery and interest rates going up, we thought the time was right,” said Valenti, who works in the financial industry.

They also wanted to lock into an FHA loan by June 1, before the rules changed, Barbieri said.

Since then, all loans with less than 10 percent down require that mortgage insurance be paid for the life of the loan. In addition, mortgage insurance will no longer be canceled when the loan balance is 78 percent of the original amount.

They beat the deadline.

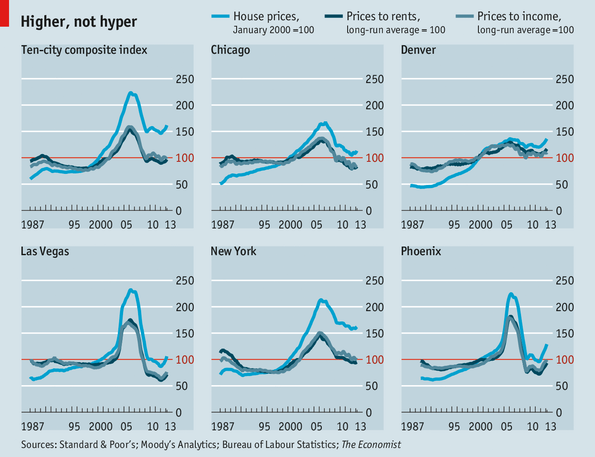

First-time buyers like Valenti and Barbieri are key to the health of residential real estate. So there is concern, at least on the national level, that there might not be enough of them to sustain the housing recovery.

This buyer segment is so important, in fact, that the National Association of Realtors surveys 3,000 members monthly for the latest percentages.

The April survey, said spokesman Walt Molony, put first-time buyers at 29 percent, “weaker than the historic norm” of 40 percent.

Other research organizations report similar findings. Tight credit, competition with investors for lower-end properties, and limited inventory typically are cited as reasons.

Economist Kevin Gillen, of the University of Pennsylvania’s Fels Institute, maintains that since the housing bubble burst in 2007, “many lower-income home buyers have been effectively cut out of the market.”

“Whether they’re unemployed, underemployed, can’t assemble a sufficient down payment, or can’t get credit, these are problems,” he said, “that disproportionately affect young, first-time home buyers.

“We’ve been left with a housing market composed of relatively wealthier households trading relatively high-priced homes with each other.”

That may be changing. In many parts of the region, the numbers of first-timers are increasing. Owing to the shortage of inventory, many of them are not having an easy time, however.