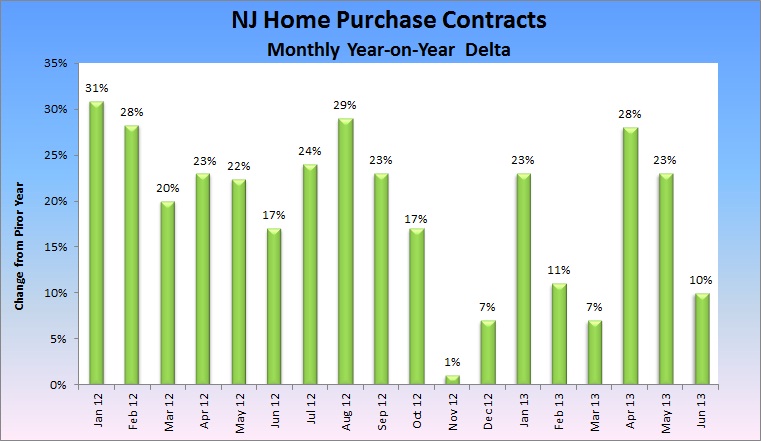

From the APP:

NJ lost 11,800 jobs in July; unemployment rate drops to 8.6 percent

This isn’t going to be easy, is it?

New Jersey’s job market lost 11,800 more jobs than it gained in July, the state reported Thursday, the first monthly employment loss since the beginning of the year.

The Christie administration and economists cautioned not to make too much of one monthly survey. But from a broader perspective it showed that despite an influx of billions of dollars in federal aid and insurance money since superstorm Sandy, New Jersey’s economy hasn’t gained traction.

“It’s like a roller coaster,” said Jim Wallace, 59, owner of Matawan Stained Glass. “You get a couple good weeks, and it dies off for a while. There’s, like, no rhyme or reason.”

…

New Jersey’s unemployment rate still managed to fall to 8.6 percent in July from 8.7 percent in June, the state Department of Labor and Workforce Development said, but the decline could be chalked up to fewer prospective workers actively seeking jobs.

…

The recovery has been slow. While the U.S. has regained more than 80 percent of the private-sector jobs it lost, New Jersey has recovered less than 60 percent, according to a recent study by Rutgers University.The obstacles are widespread: New Jersey hasn’t benefited from a resurgent manufacturing industry; federal taxes rose in January; upstart economies in China, Brazil and India have slowed; and gasoline prices spiked in July, diverting consumers’ disposable income to their gas tanks, said Patrick J. O’Keefe, director of economic research for CohnReznick, a New York accounting firm.

There are more sweeping changes, too. Workers are emerging from the recession in a new digital age in which they are armed with tablet computers and smartphones, making them so productive that employers don’t need to go on a hiring streak, said Farrohk Hormozi, an economist at Pace University in New York.

“This week I’m on vacation, but believe it or not, I’m working more extensively than if I was in the office,” Hormozi said. “That’s the nature of the job market.”