From the WSJ:

Finally, It Is Time to Buy a House

Warren Buffett famously once said: “Be fearful when others are greedy, be greedy when others are fearful.”

And if you’re not instinctively scared of the housing market, then global warming, saturated fat, running with scissors and the bogeyman probably aren’t keeping you awake at night, either.

The fact that everyone is scared to dabble in—much less commit to—housing makes it a close-to-perfect investment based on Mr. Buffett’s principle. But buying real estate is a good long-term investment for many more reasons, some of which have only become apparent in recent weeks.

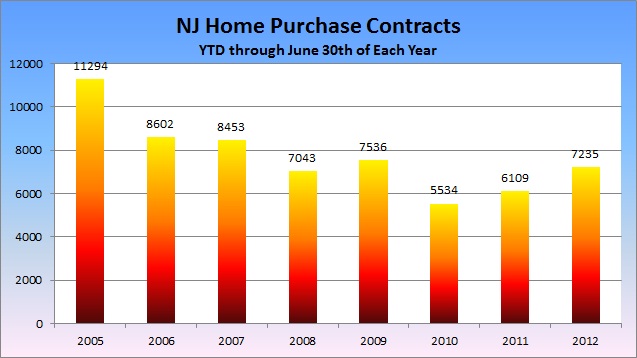

The most striking: Housing prices rose sharply from April to May. The S&P/Case-Shiller Index rose 2.2% in 20 of the nation’s big cities. Prices shot up more than 3% in Chicago, Atlanta, San Francisco and Minneapolis. Even Detroit’s housing market scored a gain, inching up by 0.4%.

Nationally, the increase was the first in seven months. More importantly, the increase matched other data and empirical evidence this spring that foreclosures slowed and inventories were shrinking. Simple economics suggests that as the supply of distressed property slows, buyers will be forced into higher-price properties.

In addition, interest rates on 30-year fixed mortgages have tumbled below 3.5%. For those who can get credit, these aren’t just historically low rates; they are one-sided deals tilted toward borrowers.

…

Here’s where the fear comes in. From 30% to 50% of existing mortgages in the U.S. market are underwater, depending on the estimate. That means many borrowers are trapped in their homes and loans. They either can keep paying and hope prices will improve or walk away, putting downward pressure on home prices.Foreclosure rates have leveled off, but market analysts believe an increase is likely.

Here’s why. Since the financial crisis, 3.7 million homes have been foreclosed on, but an additional 1.4 million remain in the national foreclosure inventory, according to CoreLogic, a real-estate research firm.

Finally, a housing recovery won’t happen, or could be snuffed out, by a rotten economy. There’s never been significant growth in housing with high unemployment. And as Dow Jones’s Kathleen Madigan noted, “Potential buyers must feel secure with their job prospects before they commit to long-term mortgages. Higher loan standards mean banks want to see an applicant’s solid income history before lending.”

There is plenty to be afraid of when it comes to home buying. But in the current investing climate, housing presents an attractive long-term investment that should hold steady or even have upside surprise in the short term.

…

Mr. Buffett would remind us that investments of any kind are not without risk. Each should be considered with the investor’s time horizon and appetites. But he also has acknowledged that real estate is especially attractive when financing is cheap, there is pent-up demand and prices have been driven down by a spooked market. Put another way, it’s time to be greedy.