From the WSJ:

HOUSE TALK

Another Full Year Of Housing Pain?

By JUNE FLETCHER

May 1, 2008 3:55 p.m.

Don’t look for the housing market to improve until the daffodils bloom next spring.

For home sellers, the continuing pain means that that homes likely won’t sell unless they are well-kept, priced below the competition and are marketed aggressively. Adding incentives like seller financing or lease-options can help bring in buyers who are having trouble getting conventional financing.

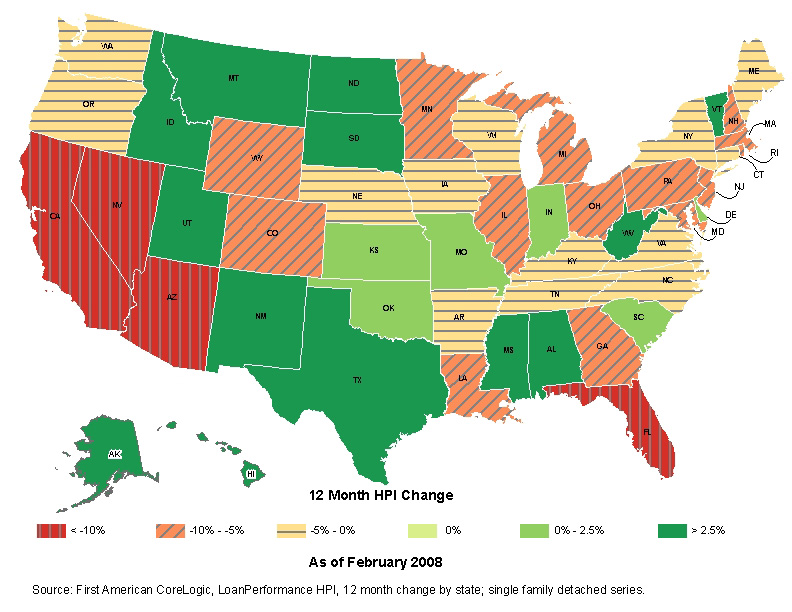

The latest S&P/Case-Shiller Home Price Index shows that new and existing home prices fell 12.7% in February from a year earlier.

According to economists who convened at the spring construction forecast conference of the National Association of Home Builders in Washington, D.C., last week, the trend will continue until early next year, dragging down prices.

The consensus view was far gloomier than a few months ago, when housing economists predicted the bottom would be reached in late summer or early fall. But now the U.S. is in a mild recession, although it hasn’t been officially declared, and the pain is spreading to more parts of the country, according to the association’s chief economist David F. Seiders. “Foreclosures keep getting worse,” he said. “Where in the world does it stop?”

Foreclosures push homeowners out of their homes and simultaneously ruin their credit, making it difficult for them to become owners again, he said. The drop-off of demand from these owners, as well as would-be buyers who don’t want to purchase while prices are still falling has become a “diabolical feedback loop,” he said.

Home builders have put the brakes on building — total annualized housing starts are down 34.5% to 1.035 million in the first quarter of this year and will likely stay at under 1 million until the middle of next year. But demand is still too weak to absorb this pace of building, according to Mark Zandi, chief economist for Moody’s Economy.com. It would take 11 months at the current sales rate to sell the new homes now on the market.

Mr. Zandi expects three quarters of the country’s major markets to experience new and existing-home price declines. In places that have been losing jobs, prices could drop as much as 40% from their peaks. “The coast is not clear,” he said.

Eric Belsky, executive director of Harvard’s Joint Center for Housing Studies, noted that declining home prices, which eroded the equity of many homeowners, “caught people by surprise.” He expects to see more households doubling up in shared homes as job loss, foreclosures and the credit squeeze continues. “People are being forced to sleep on floors,” he said.

…

Economist James Glassman, a managing director of J.P. Morgan Chase & Co., said that the current quagmire is partly due to creditors overreacting to the subprime-mortgage crisis, leaving only good savers with enough cash able to buy homes. But overall, he said, the American economy is sound, and the crisis will eventually subside as credit becomes freer and home prices stabilize. “The wheels aren’t coming off the wagon,” he said.