From Page 1 of the Wall Street Journal

Housing Chill Grows Worse, Bites Consumers

By SUDEEP REDDY and MICHAEL CORKERY

September 26, 2007; Page A1

The housing market is going into a deeper chill, and consumers are starting to shiver.

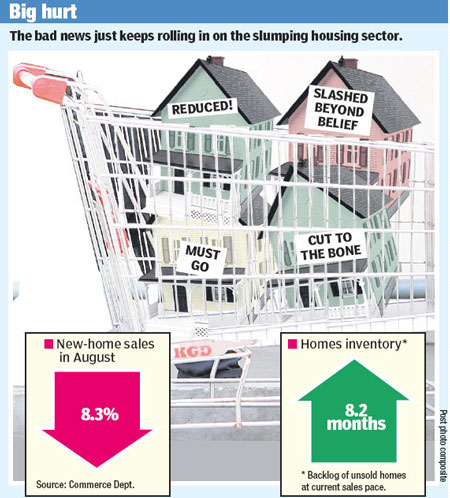

Sales of existing homes in August fell sharply, and home inventories by one measure soared to an 18-year high, according to data released yesterday. One major home builder, D.R. Horton Inc., is auctioning homes this weekend with starting prices for some units at 50% off an earlier price.

The housing market is worrying consumers, raising fresh concerns about economic growth. Consumer confidence fell this month to its lowest level in almost two years, a new survey showed. Retailers such as Lowe’s Cos. and Target Corp. said they’re feeling the pain. Both reported softer-than-expected sales Monday.

“The combination of all this is indicative of an economy that has lost quite a bit of momentum,” said Joshua Shapiro, chief U.S. economist at the consulting firm MFR Inc., an economic forecasting firm that advises investors.

…

Optimists believe the Federal Reserve’s aggressive move last week to cut interest rates will help keep the economy out of recession. Also, exports are rising, thanks to a weaker dollar, and business investment is holding up.

Still, the pace of housing’s downturn is accelerating, surprising even some bearish analysts.

From the Record:

Mortgage woes taking a toll

Home sales dropped in August for the sixth month in a row, reflecting the recent mortgage crunch, the National Association of Realtors reported Tuesday. And the NAR said it expects similar results for September.

Sales declined 4.3 percent from July, to an annual rate of about 5.5 million existing homes – a pace well below last year’s 6.5 million sales and 2005’s record 7.1 million sales.

…

In another sign of housing distress, the Standard & Poor’s Case-Shiller Home Price Indices, also released Tuesday, found home prices down an average of 3.9 percent from July 2006 to July 2007 in 20 metropolitan areas around the nation. The New York metropolitan area was down 3.8 percent in that period.

“The decline in home prices clearly continued into the summer months,” said Robert J. Shiller, chief economist at MacroMarkets LLC.

And in one more piece of pessimistic housing news Tuesday, Miami-based homebuilder Lennar Corp. said it lost $525 million in the third quarter, as home contracts and deliveries plummeted by more than 40 percent.

…

Lennar has a number of developments under way in New Jersey, including Dehart Place, a town house complex that is part of the redevelopment of central Morristown, and Henley on Hudson, a luxury condo and town home development on the West New York waterfront.

Prices of most units at both Dehart and Henley top $1 million.

Somebody should tell the Daily Record, not to ask a real estate agent their opinion on the market. What he got was a sales pitch, not an accurate assessment of the market. After all, everyone knows that there has never been a better time to pay a commission buy or sell a home.

Coldwell Banker exec: Real estate back to ‘normal’

Real estate is still one of the best investments you can make, says Ronnie Laiken, president and chief operating officer of Coldwell Banker Residential Brokerage in New Jersey/Rockland County, N.Y.

As she sees it, things are back to normal after the frenzy of recent years.

Sellers “should be aware that buyers are doing their research and checking comparables,” she says.

“We experienced an unusual market where prices were inflated, but now the market has stabilized. We didn’t have a bubble that has since burst but a market that is transitioning back to a more normal market.