NJ YTD Purchase Contracts Back Up

After home sales recorded a 6% retraction in March, New Jersey recorded more than 11,000 purchase contracts during the month of April equating to a 7% increase compared to the same month last year. As a result, the number of year-to-date purchase contracts (January-April) in New Jersey is up marginally by 1%, or roughly 425 contracts. While misinformation about the newly implemented tax reform is partially to blame, statewide housing inventory is also holding back sales, especially for homes priced below $400,000 where there is only 3 months of supply.

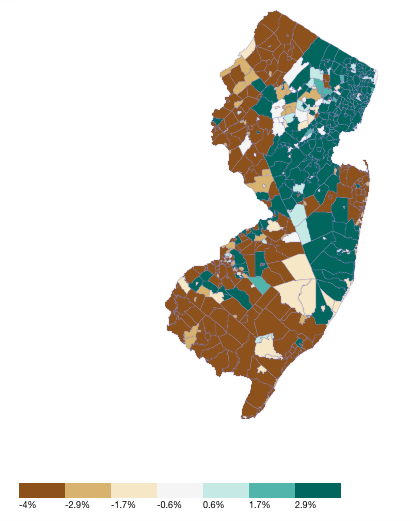

While the number of year-to-date home sales has increased by 1% overall, that is not the case for all price ranges. Contract activity for homes priced under $400,000 has declined by 1% due to supply shortages, with unsold inventory having dropped by 15% year-to-date. At the opposite end of the spectrum, contract activity for luxury priced homes over $2.5-Million has increased by 15%, which is somewhat misleading, given the smaller sample size of sales within this price point.

Shifting to the supply side of the equation, inventory remains restricted, which is limiting choices for home buyers. The number of homes being offered for sale today in New Jersey has fallen to its lowest point since 2005, having declined by 3,200 (-7%) over the past year. This is also 44% less than the amount of homes (32,000 fewer) on the market compared to the cyclical high in 2011. Today’s unsold inventory equates to just 3.7 months of sales (non-seasonally adjusted), which is lower than one year ago, when it was 4.2 months.

Currently, all of New Jersey’s 21 counties have less than 8.0 months of supply, which is a balance point for home prices. Middlesex County has the strongest market conditions in the state with just 2.5 months of supply, followed by Union, Essex, Hudson, Passaic, Monmouth, Mercer and Burlington Counties, which all have fewer than 3.5 months of supply. The counties with the largest amount of unsold inventory (5 months or greater) are concentrated in the southern portion of the state including Cumberland (5.0), Atlantic (5.9), Salem (6.1) and Cape May (6.5), however, these counties have shown vast improvement and are exhibiting strengthening conditions.

Demand for rental apartments continues to expand in NJ with statewide occupancy ratesbeing among the highest in the US. Statewide vacancy increased slightly from the prior quarter, rising by 10 basis points to 3.6%. The rise in vacancy is attributable to the rapid growth in pipeline supply, which has increased from 6,400 apartments in 2008 to 30,000 today. Nationally, the average vacancy rate increased by 20 basis points to 4.7%. Still, statewide and national vacancy rates remain well below their 2010 peak having fallen by 160 bp and 330 bp, respectively.

Consistent with national trends, the homeownership rate in New Jersey declined following the onset of the Great Recession. More recently however, the State’s homeownership rate has risen to 64.3% in 2018.Q1, due largely to increased market participation by Millennial homebuyers, which is favorable to housing development. Still, the homeownership rate at both the state and national levels have declined by 10% and 7% from their respective peaks. Because of this shift, there are approximately 231,000 additional renters in New Jersey.

…

The percentage of delinquent mortgage loans in New Jersey that are 90+ days past due fell by 10 basis points from the prior month, falling to 3.3%. Most of the nation has seen a decline in delinquency rates over the past year apart from storm-ravaged states like Florida and Texas whose delinquency rates have increased by 100% and 50%, respectively, over the past 6 months. Florida leads the nation with 5% of mortgages being 90+ days delinquent. Rounding out the list of states with the highest delinquency rates are New York (3.7%), New Jersey (3.4%), Louisiana (3.3%), Mississippi (3.3%), Maine (2.7%), Texas (2.6%) and Delaware (2.5%).

New Jersey foreclosure filings in 2017 recorded a decline (-5%) over the prior year, falling from 74,200 to 70,150. This is the second consecutive annual decline that the state has seen since 2010. Based upon year-to-date data (January-April), foreclosures are projected to decline further, falling by -8% in 2018, with filings estimated to be about 64,350. The greatest concentrations of mortgage delinquencies in New Jersey continue to be in the state’s urban and rural places, such as Warren and Atlantic Counties who lead the state in the ratio of foreclosure actions-to-housing units.