Prices for single-family homes in the Philadelphia region rose 0.7 percent in the second quarter, the first increase since 2008 that was not the result of government intervention in the real estate market.

An analysis of data for Prudential Fox & Roach by economist Kevin Gillen, vice president at Econsult Corp. of Philadelphia, showed second-quarter prices rose 0.9 percent in the suburbs and 0.2 percent in the city from first-quarter levels.

Gillen’s suburban data cover Bucks, Montgomery, Chester, Delaware, Camden, Gloucester, and Burlington Counties, as well as Salem and Mercer Counties in New Jersey and New Castle County, Del. – the locales in which Prudential Fox & Roach sells real estate. The data do not include condo sales.

The modest increase came after three consecutive quarters of declines totaling an average of 11 percent since the April 2010 expiration of the home-buyer tax credit. What adds to the significance of the second-quarter rise is that it occurred without any assistance from the government.

Not every county saw prices go up: Delaware and Salem Counties fell 1.3 percent and 4.1 percent, respectively; Bucks and New Castle were flat. Of the counties in which prices rose, Camden County was up 0.6 percent; Chester, 1.5 percent; Burlington, 1.6 percent; Gloucester, 2.4 percent; Montgomery, 2.5 percent; and Mercer, 6.1 percent.

“With these most recent price changes, the region’s house values have fallen by a cumulative average of 19 percent” since the market downturn began in third quarter of 2007, Gillen said.

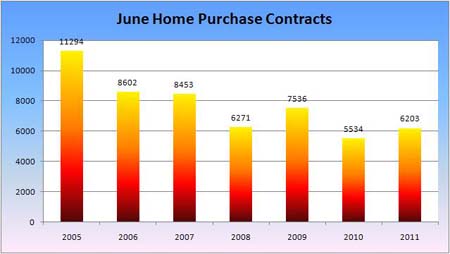

Single-family-home sales – there were 13,558 in the second quarter – are running 18 percent below normal, he said, and the average time to sell a house in the region was 100 days, down from 120 in the first quarter.

…

What he finds notable is that city home values (excluding condos) have held up better than those in the suburbs. From their peak in 2007, city single-family-home prices have fallen 16 percent; suburban prices dropped 20 percent in the same period.

In the 1990-94 economic downturn, prices in Philadelphia fell 17 percent, while the suburbs dropped just 2 percent. City values have held up much better, even though the current downturn is more severe, Gillen said.

…

Outer-ring suburbs have seen home values drop more than closer-in suburbs. In the city, outer neighborhoods lost more value than Center City and adjacent neighborhoods.

In the 1990-94 downturn, the average home in Center City depreciated 41 percent. Today, value has dropped an average of 13 percent.

“That’s enough to actually negate the underperformance of Philadelphia homes during the 1980-2000 period,” Gillen said.

“If you were standing in 1980, and had a choice between buying a random home in Philly and a random home in the suburbs, and then were to hold that home until today, the Philadelphia home would actually outperform the suburban home in terms of total appreciation.

“If you predicted that to anyone in 1980 they would have had you committed!”