From the WSJ:

Housing on Mend, but Full Recovery Is Far Off

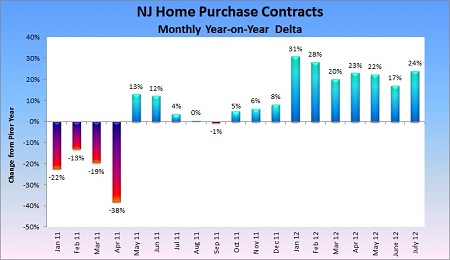

Home prices during the first half of 2012 posted their strongest gains in six years, the clearest sign that more U.S. housing markets have hit bottom.

But the housing market remains far from normal. Hitting a bottom shouldn’t be confused with a full-on recovery, which looks a ways off.

Today’s rising prices have less to do with surging demand—though hard-hit markets in Arizona, California, and Florida have seen significant investor appetite for distressed homes—than with declines in the number of properties for sale.

Inventories of “existing” homes—that is, ones that haven’t just been built—are at eight-year lows. New-home inventories are lower than at any time since the U.S. census began tracking them in 1963. In some cities, there are one-third fewer homes listed for sale than a year ago.

Here’s why prices are rising: There are more buyers chasing fewer homes, and—critically—fewer distressed homes, such as foreclosures. Low inventory is one sign that housing markets may have reached a turning point because many want to buy at the bottom but few want to sell.

There are several factors behind the low inventory. Banks have slowed their pace of foreclosures. Investors have snapped up discounted properties that they can convert into rentals. Home builders, struggling for several years to compete on price with foreclosed properties, have added little in the way of new supply.

For now, price gains are concentrated at the low end of the market, where inventory declines have been most dramatic. “The market is really drying up in these seemingly distressed markets really quickly,” said Michael Sklarz, president of research firm Collateral Analytics. “They really are scratching for properties to sell.”

Low inventory is benefiting home builders, as buyers grow frustrated by bidding wars sparked by a shortage of move-in-ready housing. “People can’t find inventory that they want, so they say, ‘I’m just going to buy the house down the block that’s brand new. I don’t have to go through the whole torture,’ ” Mr. Sklarz said.

…

An important test comes later this year. In each of the past three years, prices rose in the summer but gave up all those gains and more in the winter, when sales traditionally slow. This year could be different because the supply of homes isn’t piling up.Absent a shock to the economy, housing is on the mend. But it will be a long time before it returns to normal.