From CNBC:

Home Price Headlines Hide the True Picture

How do I loathe home price day?

Let me count the ways.

The rash generalizations, the seasonal vs. non-seasonal adjustment confusion, the month-to-month vs. year-over-year, the contention among all the varied home price reports from the various and varied entities that track them.

…

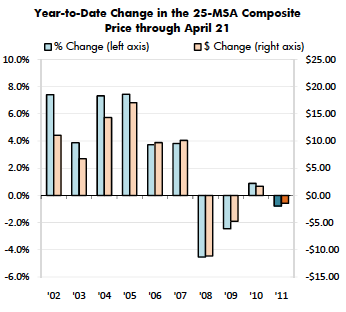

This month is particularly frustrating, because the big headline from S&P/Case Shiller was that home prices rose for the first time in eight months. Okay, yes, from March to April, with no seasonal adjustments, home prices rose barely, less than one percent, in the nation’s top 20 housing markets. When you seasonally adjust those numbers, the prices fall. Why?Because in different seasons, different types of buyers buy different types of homes.

The Spring market is historically replete with families; these are move-up buyers, purchasing larger, more expensive homes. That skews the overall prices higher. They buy in the Spring because they want to move over the summer, when school is out. You tend to see more single and first-time buyers in the fall.

(jb’s note – This is incorrect, the repeat sales methodology used by Case Shiller will correct for this seasonal skew)

This is why I judge prices year over year, because you are comparing apples to apples. Prices are down in 19 out of the top 20 markets year-over-year, with six markets hitting new lows on the S&P/Case Shiller Home Price Index.

From the WSJ Developments Blog:

Don’t Jump at Case-Shiller Bounce

There’s a good reason not to get too excited about Tuesday’s report from Standard & Poor’s on the Case-Shiller home price index: As sure as the sun comes up in the morning, home prices will rise in April.

The latest Case-Shiller report said that home prices on a non-seasonally adjusted basis gained for the first time in eight months. On a monthly basis, it did the same in 2009 and 2010 — and both times it raised hopes that home prices would hit bottom “later this year.”

After accounting for seasonal factors (more homes tend to sell in April versus March), the index was virtually unchanged from April.

That’s less exciting, but it’s still good news. It means that home price declines are moderating. Consider: Prices fell by 0.1% in April; 0.3% in March, February and January; 0.4% in December; 0.5% in November; a nearly 1% in October. In addition to normal seasonal factors, such as warmer weather, home price indexes such as Case-Shiller, which measure repeat transactions of existing homes, can be skewed by the share of distressed home sales.

…

What Tuesday’s report suggests is that “some of the declines we saw in the winter were overstated. We’re now going to see a bounce,” says Thomas Lawler, an independent housing economist in Leesburg, Va.“There’s no evidence yet that we’re in any material rebound,” he says, before making a bold prediction: “We will be in one next year.”

…

Mr. Newport expects prices to fall by another 5% over the next year, but he says “you could quite possibly argue that [prices] are nearing a bottom, and that they may not drop another 5%.”