From the WSJ:

US March Existing-Home Sales Up 3.7% From February

Sales of previously occupied homes in the U.S. rose slightly in March at the start of the crucial spring selling season, but prices were weak, suggesting that any recovery in the struggling sector will be slow and modest.

Existing-home sales increased 3.7% from a month earlier to a seasonally adjusted annual rate of 5.10 million, the National Association of Realtors said Wednesday. The results were slightly better than expected. Economists surveyed by Dow Jones Newswires had expected home sales to rise by 2.5% to an annual rate of 5.0 million.

“While the increase is encouraging, we still do not see the gain as the start of a genuine recovery,” wrote Wells Fargo & Co. economist Anika Khan. She noted that February’s results were likely artificially depressed due to bad weather.

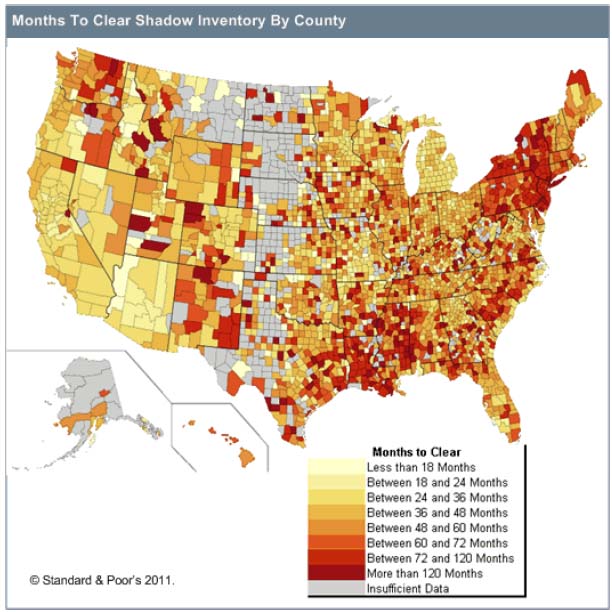

About 40% of existing homes bought last month were distressed properties–including foreclosures and sales in which the lender agrees to sell the home for less than the total mortgage amount. That was the highest percentage since April 2009.

Some analysts expect the housing market to improve later this year as unemployment drops. But they don’t expect a dramatic rebound. “The underlying trend for existing home sales is improving, but only at a gradual pace,” wrote Michael Gapen, senior U.S. economist with Barclays Capital.

The median sales price for an existing home was $159,600, down 5.9% from the year-ago median price of $169,600.

Meanwhile, the inventory of previously owned homes listed for sale climbed at the end of March to 3.55 million available for sale. That represented a 8.4-month supply at the current sales pace, compared with a revised 8.5-month supply in February.

The housing market has continued to struggle even as other segments of the U.S. economy show steady improvement. Last year was the worst year for sales of previously occupied homes since 1997, with about 4.9 million homes sold, according to the Realtors group.

Lawrence Yun, the Realtors chief economist, called the results “a decent figure, not a great figure.” All-cash sales are particularly strong, representing about 35% of all transactions, Yun said. That is likely an all-time high.

Still, many signs point to continued troubles.

From CNN/Money:

‘Uneven’ housing recovery continues

Sales of existing homes increased in March, “continuing an uneven recovery” in real estate, an industry group said Wednesday.

Home sales rose at an annual rate of 5.1 million in March, up 3.7% from February, the National Association of Realtors said Wednesday. However, sales were 6.3% lower than in March 2010.

…

hose reports are not bad, but not great either. Despite slight upticks in home sales and construction, the housing sector is still in the doldrums as supply continues to far outweigh demand for homes.

“Even as buyers scoop up deals of a lifetime, the river of foreclosed properties continues to flow,” Douglas Porter, deputy chief economist at BMO Capital Markets, said in a note to investors Wednesday morning.

The median home price slipped 5.9% to $159,600, compared to a year earlier.

Meanwhile, some buyers are still finding it tough to get a mortgage, Lawrence Yun, chief economist for the National Association of Realtors, said in a release. The average credit score to get a conventional mortgage has risen to 760 from 720 in 2007.

“Although home sales are coming back without a federal stimulus, sales would be notably stronger if mortgage lending would return to the normal, safe standards that were in place a decade ago — before the loose lending practices that created the unprecedented boom and bust cycle,” he said.

…

First-time buyers purchased 33% of homes in March, down from 44% in March 2010. Investors accounted for 22% of sales, up from 19% a year ago.

From CNBC:

Investors drove home sales up 3.7 pct. in March

Investors drove up U.S. home sales last month, plunking down cash to grab cheap homes at risk of foreclosure. But first-time homebuyers, who are crucial to a housing recovery, stayed away.

Sales of previously occupied homes rose last month to a seasonally adjusted annual rate of 5.1 million, the National Association of Realtors said Wednesday. That’s up 3.7 percent from 4.92 million in February. The pace is far below the 6 million homes a year that economists say represents a healthy market.

…

Many of those purchases are being made by investors, who are targeting cheap properties in areas hit hardest by foreclosures: Phoenix, Las Vegas and Tampa.

The evidence of their activity: sales of homes priced under $100,000 have risen 10 percent from a year ago. In that same period, sales of mid-priced homes, between $100,000 and $500,000, have fallen by more than 14 percent.

A big reason for that is fewer first-time homebuyers, the types of people who set down roots and raise families, are entering the market. Sales among that group fell to 33 percent in March. A more healthy percentage of first-time buyers is 40 percent, according to the trade group.

…

For March, sales rose 8.2 percent in the South, 3.9 percent in the Northeast and 1 percent in the Midwest. Sales fell 0.8 percent in the West.