From Inside Jersey:

Trying for a comeback: New Jersey’s housing market in 2010

After putting the nation’s economy through the spin cycle, the real estate market this year could take a break.

Home prices look as if they’ve reached their lowest points, and people are starting to take deep breaths and buy again. It’s beneficial, too, that the federal government has helped keep mortgage rates down, in the 5 percent range, and Congress extended and expanded tax credits so they reach almost all potential buyers — not just first-timers anymore. Together, this means houses remain more affordable than they were for decades.

However, it’s tough to pay your mortgage without a job, and New Jersey’s labor market is key to a recovery in home prices.

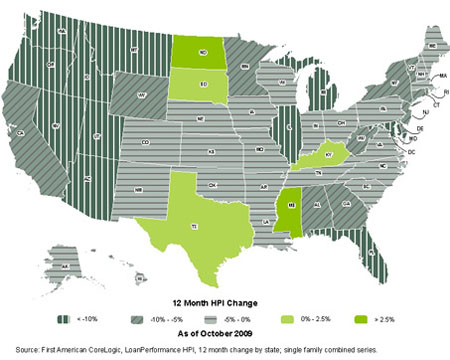

“The worst is behind us, but the labor market is the big cloud going forward,” says Rutgers economist Joseph Seneca. If the economy does what’s being called a “double dip” or a “W,” more people could lose their jobs, and eventually their homes. But for now, most local markets have already stopped their price slide, and some markets are even coming back.

Overbuilt Hudson County will continue to struggle. Manhattan’s weak market is sapping demand from Hudson County, and deep South Jersey is hurt by being far from major job centers — Philadelphia and New York — and by Atlantic City’s losing streak.

…

Good news for home sellers is that while they don’t exactly have the upper hand, they may not feel as desperate to sell before prices fall any further. “It gets better from here,” Otteau says. “Some markets will be experiencing modest, gentle price increases.”

…

Still, sellers will be up against more competition from the “shadow market” — something that’s not quite as spooky as it sounds. This market is composed of sellers who had been waiting on the sidelines, because they figured it wasn’t worth putting their homes on the market when buyers were scarce. They’ll come out, adding to the supply.

…

BEST THING THAT COULD HAPPEN:

Home prices rise slowly. It could take years to get back to the highs of 2005 and 2006. Jeffrey Otteau, who tracks home prices, predicts no change in 2010 prices. However, New Jersey should see a 3 percent rise in 2011.WORST THING THAT COULD HAPPEN:

The economy retreats, consumers and employers get scared, and more people lose their jobs. The government pulls back support, mortgage rates rise and sales fall. Foreclosures and fear send prices down again.