Now Open, Part II!

Prior weekend thread closed due to comment overflow

——————————————–

Save the Date!

New Jersey Real Estate Report Get Together

June 14th, 2008 at 5pm

The Brass Rail

135 Washington St

Hoboken, NJ 07030

Now Open, Part II!

Prior weekend thread closed due to comment overflow

——————————————–

Save the Date!

New Jersey Real Estate Report Get Together

June 14th, 2008 at 5pm

The Brass Rail

135 Washington St

Hoboken, NJ 07030

This is the time and place to post observations about your local areas, comments on news stories or the New Jersey housing market, open house reports, etc. If you have any questions you wanted to ask earlier in the week but never posted them up, let’s have them. Also a good place to post suggestions, requests for information, criticism, and praise.

For readers that have never commented, there is a link at the top of each message that is typically labelled “[#] Comments“. Go ahead and give that a click, you might be missing out on a world of information you didn’t know about. While you are there, introduce yourselves to everyone.

For new readers that have only read the messages displayed on the main page, take a look through the archives, a substantial amount of information has been put online in the past year. The archives can be accessed by using the links found in the menus on the right hand side of the page.

From the Courier Post Online:

State moves to help those in danger of foreclosure

An Assembly panel released a measure today that would create a roughly $30 million fund aimed at helping those facing foreclosure because of the problems in the subprime mortgage market.

“The subprime mortgage foreclosure crisis is real. It’s happening everywhere, and it demands your immediate attention,” Staci Berger, of the Community Development Network of New Jersey, told members of the Assembly Housing and Local Government Committee.

The committee, along party lines, voted 4-2 to release a measure that would levy a $2,000 fee on lenders every time they initiate a foreclosure. The fees, expected to generate between $27 million and $33 million per year, would be placed in a trust fund for mortgage counseling and emergency loans.

“New Jersey has a responsibility to take action now to protect homeowners who are at risk of losing the roofs over their heads,” Assembly Majority Leader Bonnie Watson Coleman, D-Mercer, who sponsors the measure, said in a prepared statement. “The housing bubble has burst, and we must do all we can to ensure New Jersey homeowners swept up in the flood at foreclosures can keep their heads above water.”

The only objections voiced at the hearing were from a dispute over what services struggling homeowners need. That debate split the advocates representing ther interests of the 13,500 to 16,500 homeowners projected to lose their homes this year.

“The need is more legal representation,” said Margaret Lambe Jurow, of Legal Services of New Jersey’s Anti-Predatory Lending Project. “… The loan product itself is defective. When we had lead toys on our shelf, we took them off and we removed them. But when we have these loan products here, the answer isn’t to negotiate a better deal that could have a pay out over time. It is to go back and say what was wrong with the product and to litigate that product.”

…

The measure would also require creditors to offer a six-month hold on foreclosure proceedings and allow borrowers to use mediation services to help in their refinancing negotiations.

For those of you interested in Bergen County, Rich has provided an incredible set of charts based on New Jersey MLS (NJMLS) Bergen County data. While I’ve focused on GSMLS data, because of it’s broader coverage, its downside is that Bergen isn’t well covered. Just note that the 2008 numbers in the first three graphs are YTD. Be sure to thank Rich for putting together such a comprehensive set of charts.

From MarketWatch:

There’s a big, annoying ad campaign for a popular insurance company where the punch line of every commercial is “I saved a bundle on my car insurance.”

If people actually behaved like the actors in the commercials, you might soon hear some of your friends and neighbors saying “I saved a bunch on my real estate commissions.” And after that it could be “I saved a bundle on my financial planning.”

…

The proof may have come last week, when the Justice Department reached a tentative settlement with the National Association of Realtors that essentially forced traditional real estate brokers to give Internet-based agents access to home-listing information that they had previously been denied.Online real estate agents often charge discounted commission fees and let buyers review listings at their own pace, but for years those Internet-based brokers in many parts of the country could not access more than 800 Multiple Listing Services nationwide affiliated with the national Realtors group. An MLS is a database of regional properties for sale.

The traditional argument against opening the MLS system to online brokers was that it would result in a significant cut in commissions for traditional real estate agents. Indeed, that’s precisely what government officials wanted.

…

In the fall of 2005, government lawyers filed suit against the national Realtors group, saying that the lack of access amounted to discrimination against online brokers. Last week’s settlement, filed in Chicago, opens the listings databases to traditional and online property agents, which should effectively allow brokers to decide exactly how they want to compete in the marketplace.

Last year, the Justice Department and Federal Trade Commission found that home buyers and sellers were missing out on the kinds of cost savings and benefits that consumers in other businesses have reaped as a result of Internet technology. The main stumbling block was perceived to be the access issue.Whether the settlement — which is likely to take effect in late summer or early fall, 60 days after final approval, and which will be in place for 10 years — actually gets the job done and lowers commissions remains to be seen.

In Delaware, for example, the two listings services — including one that extends into southern New Jersey and eastern Pennsylvania — never barred access to online agents, so long as those brokers were properly licensed.

…

That schism is where consumers can potentially make some money. In a real estate market that has significantly slowed in most parts of the country, there’s nothing wrong with demanding the services you need, and paying only for what you use. Rather than lose your business — something a broker might have done a few years back when they were flush with clients — you may find that you can get both traditional and online agents to give you the best of both worlds.

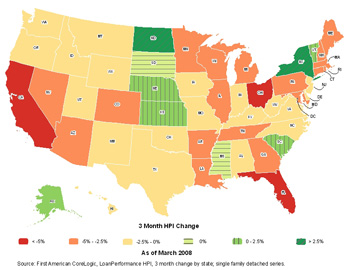

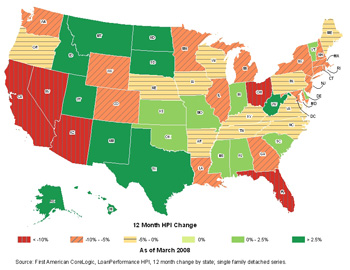

From First American CoreLogic:

Forty Two States Show Decline in Past Three Months

“Two thirds of all states now show year-over-year real estate declines according to this latest LoanPerformance HPI release,” said Mark Fleming, chief economist for First American CoreLogic. “Although only one-third of CBSAs are depreciating on a nominal basis, on an inflation adjusted basis 90 percent of CBSAs are experiencing real price declines. Only 10 percent of CBSAs are experiencing real inflation-adjusted price increases,” added Fleming.

12-Month Change By Top CBSAs (Core Based Statistical Areas) as of March 2008

Edison, NJ: -4.98%

New York-White Plains-Wayne, NY-NJ: -3.58%

From the WSJ:

Number of Foreclosed Homes Keeps Rising

Lenders Cut Prices To Jump-Start Sales As Inventory Grows

By JAMES R. HAGERTY

June 2, 2008; Page A3

The number of foreclosed homes owned by lenders continues to rise despite signs that they are increasingly willing to slash prices to sell those properties.

Lenders and investors in mortgages owned about 660,000 foreclosed homes in April, up from 493,000 in January and 231,000 in January 2007, according to First American CoreLogic, a research firm based in Santa Ana, Calif., that collects data from lenders and county clerks. The April total works out to about one in seven previously occupied homes available for sale nationwide.

A surge in defaults has increased the inventory of bank-owned homes, known in the trade as REO, for “real estate owned.” By cutting prices, lenders have managed to increase sales of such homes sharply in recent months in some cities hit hard by foreclosures, including Las Vegas, Detroit and Sacramento, Calif., local real-estate brokers say.

With home prices falling, “holding the assets means further losses,” said Mark Fleming, chief economist for First American CoreLogic. Some lenders now are cutting prices as often as every 20 days on homes that aren’t selling, said David McCarthy, chief executive officer of Integrated Asset Services LLC, a Denver-based company that helps banks value and sell REO homes.

But lenders haven’t yet managed to catch up with the inflow of foreclosed homes. Mark Zandi, chief economist at Moody’s Economy.com, forecasts that the inventory of REO homes won’t peak before the end of 2009.

In dollar terms, foreclosed one- to four-family homes owned by lenders whose deposits are insured by the Federal Deposit Insurance Corp. more than doubled to $8.56 billion at the end of the first quarter from $3.59 billion a year earlier.

The REO glut is weighing on house prices in many areas, as banks tend to cut prices faster than other sellers. A new set of local home-price indexes, to be introduced this week by Integrated Asset Services, shows that the median price of homes sold in Riverside County, Calif., in April was down about 29% from a year earlier. The median price fell about 13% in Clark County, Nev., and 12% in Arizona’s Maricopa and Pima counties. Median-price comparisons can be skewed by shifts in the proportions of high- and lower-priced homes sold from one year to the next but provide a broad indication of market trends.

From Newsday:

FREE HAIRCUTS . . . if she sells their house

Bring the buyer. Get a year of free hair salon services.

That’s the offer real estate agent Zandra Lawrence got in September from a Miller Place seller if her house-hunting client agreed to come back and purchase the home, with free high-end furniture included.

“I just thought it was very, very surprising, but it got my attention, even though my buyers were going into contract on another house,” said Lawrence, who works out of Coach Realtors’ Miller Place office. “I was obligated to tell the buyers what the seller had offered them.”

…

These perks to agents have been a growing local phenomenon as homeowners and their agents cope with a glut of homes all competing for limited numbers of buyers. A vacation, cash bonus, higher commission split and other incentives are there for agents who can match house with house hunter. This marketing to agents may not lead to a closing, but the point of a buyers’ agent bonus is to boost foot traffic on the properties, a way to increase chances of a deal.

…

But because no one’s biting, Stark has added a feature to his listing – a $5,000 bonus for the buyer’s agent. He realizes that buyers aren’t as plentiful nowadays and agents are like the gatekeepers to them.“Agents are pulled in a lot of directions,” he said. “By giving agents an incentive, they take note and maybe they would show your house.

“You can’t sell the house unless people walk through the doors. Yes, you’re paying for it to drive people in and then the house has to basically speak for itself.”

Like a lot of offers to buyers’ agents, Stark’s five grand has an expiration date. The agent gets it only if the buyer signs by the end of this month. To him, the deadline gives urgency to his listing.

“Once it’s there forever, then it’s just like any other house,” said the homeowner, who owns a mortgage brokerage. “If you don’t hit the emotions, you’re not going to sell anything.”

…

But one real estate finance professor said such bonuses could lead to a conflict between what’s best for the agents and what’s best for the buyers.“They may not be shown all the houses that are best for them,” said Robert Campbell, who teaches at Hofstra University. “They may be shown the houses that have the bonus. They may be shown those houses first.”

Victory!

At 8:18am EST on June 1st, I’m claiming victory. The New Jersey Real Estate Report is, unequivocally, the best regional/state real estate blog in the country (not that we needed this contest to know that). Kudos to Keith at Housing Panic for putting up a great fight, it came down to the wire. The allegations of ballot stuffing are pure nonsense, in the past week alone, this site was been visited by more than 10,000 unique visitors. If anything, votes were probably on the low side due to visitors coming to the site via search engine, and not hitting the main page directly.

—————————————-

This is the time and place to post observations about your local areas, comments on news stories or the New Jersey housing market, open house reports, etc. If you have any questions you wanted to ask earlier in the week but never posted them up, let’s have them. Also a good place to post suggestions, requests for information, criticism, and praise.

For readers that have never commented, there is a link at the top of each message that is typically labelled “[#] Comments“. Go ahead and give that a click, you might be missing out on a world of information you didn’t know about. While you are there, introduce yourselves to everyone.

For new readers that have only read the messages displayed on the main page, take a look through the archives, a substantial amount of information has been put online in the past year. The archives can be accessed by using the links found in the menus on the right hand side of the page.

John St, Ridgewood NJ

MLS# 2819679

Listed: 5/13/2008

List Price: $769,000

Reduced to: $745,000

Active

———————————–

Jerome Ave, Glen Rock NJ

MLS# 2723934

Listed: 5/13/2007

List Price: $549,000

Reduced to: $519,000

Withdrawn

MLS# 2809536

Listed: 3/9/2008

List Price: $500,000

Reduced to: $479,000

Active

———————————–

Harrington Street, Hillsdale NJ

MLS# 2723934

Listed: 6/11/2007

List Price: $689,000

Withdrawn

MLS# 2742492

Listed: 10/19/2007

List Price: $659,000

Reduced to: $639,000

Expired

MLS# 2817462

Listed: 4/29/2008

List Price: $638,500

Withdrawn

MLS# 2821719

Listed: 5/29/2008

List Price: $599,000

Active

———————————–

Woodland Cross, Westwood NJ

MLS# 2748135

Listed: 12/10/2007

List Price: $659,000

Reduced to: $630,000

Withdrawn

MLS# 2808782

Listed: 3/4/2008

List Price: $629,000

Sold: $570,000

Sale Date: 5/27/2008

———————————–

Haworth Ave, Haworth NJ

MLS# 2804108

Listed: 1/30/2008

List Price: $829,000

Reduced to: $769,000

Withdrawn

MLS# 2821495

Listed: 5/27/2008

List Price: $769,000

Active

From the Economist:

Through the floor

America’s house prices are falling even faster than during the Great Depression

From the Wall Street Journal:

Lessons From the Housing Bubble

By DAVID WESSEL

May 29, 2008

Before we replace angst about housing, mortgages and credit markets with anxiety about rising oil prices, consider what we’ve learned in the past several months. We had a housing bubble; that’s now obvious. But how did it happen? Why was its bursting so painful? Without answers, we can’t hope to reduce chances of a repeat.

Boil it down to the three R’s: rocket scientists, regulators, and ratings agencies.

The rocket scientists are the wizards of Wall Street who invented securities that supposedly dispersed risk widely but actually created much more leverage than proved wise.

There is a good case that the savings-and-loan mess of the 1980s was made in Washington, the inevitable result of government deposit insurance that led to tails-you-lose, heads-I-win banking. The current mess was made on Wall Street.

A bubble so large also required aggressive mortgage originators, imprudent home buyers and myopic investors. But it wouldn’t have been as bad if not for the paper factories that sliced up individual subprime mortgages and assembled the pieces into securities, each with its own acronym, that were deemed safer than the underlying loans. They behaved as if they were taking a little poison and diluting it in a big reservoir; instead, they poisoned the entire water supply.

…

“The idea of risk dispersion is nice in theory, but in practice it depends on who it gets dispersed to,” says Peter Fisher, a former Federal Reserve Bank of New York official now at money manager BlackRock Inc. “It turned out we weren’t dispersing it to strong hands who could hold it through the volatility. Rather, we were dispersing it to weak hands who couldn’t hold it, and ended up adding to the volatility.”The cost of delinquency, default and falling house prices often was passed to entities (some linked to brand-name banks) that lacked the financial strength to weather a storm. As the entities couldn’t bear the burden for long, they had to sell mortgage-linked securities into a hostile, illiquid market, pushing down already depressed prices.

In a modern capitalist system, regulators provide guardrails to keep markets from driving the economy off a cliff. The regulators failed. Whether regulators should or could have restrained innovation on Wall Street or prohibited business deals between consenting, sophisticated adults is a tough question.

But regulators failed to protect unsophisticated consumers from mortgage loans that they simply couldn’t afford or didn’t understand; they’re now fixing that. And regulators misunderstood the risks that banks were taking and failed to stop lenders from lowering standards too far in their frenzy to attract business; fixing that will be tougher.

Among their many failings, the regulators allowed lenders to make a fundamental mistake: To lend not against the borrower’s cash flow and income, but instead to lend against the seemingly inexorable increase in the value of the collateral. Mortgages were made to people who couldn’t afford the payments because the lender (or investor) figured that if the borrower defaulted, the house would always be worth more than the loan.

“It is the hallmark of a credit bubble when lenders think that because collateral is going up in price they can ignore the borrower’s ability to pay,” says BlackRock’s Mr. Fisher. “Collateral should only be a backstop.” When lenders forget that, regulators must step in. “Lenders need someone to prevent them from competing their way to the bottom,” he says. Let’s put those words on a laminated card and hand it to every banking supervisor.

…

The flaws of rating agencies are a mélange of conflicts of interest, misleading grading systems that classified complex securities as if they were much like simple corporate bonds and a backward-looking approach that proved particularly useless. They were the enablers. They are atoning and changing their ways, as they should. Their business model will change; government oversight will be strengthened.But investors who relied on the rating agencies — particularly supposedly sophisticated pension funds and other institutions — are at fault, too. Rating firms became a crutch for investors who simply didn’t want to spend the time and money required to be prudent investors at a time when low interest rates had everyone reaching for higher returns without contemplating the higher risks.

A little “back to basics” in banking and investing would go a substantial way toward avoiding a repeat of the Panic of ’08.

Enjoy!

Notes:

OFHEO HPI and Purchase Only Index are both quarterly state-level series.

S&P Case Shiller Index is a monthly series and is based on the NYC Commutable Metro Area. This index includes areas outside of New Jersey.

NAR/NJAR Index is a quarterly state-level series based on MLS data.

OFHEO and HPI Indicies are based on repeat sales, NAR/NJAR is a simple median.

S&P Case Shiller Tier Rankings are as follows:

Low: Under $327733

Middle: $327733 – $469975

High: Over $469975

(as of March 2008)

Source data can be found here:

NJ Home Price Tracker Spreadsheet (XLS)

Hat tip to Pretorius for aggregating the bulk of this data and providing the concept. I’ll be adding the OFHEO MSA level data in the next day or two.

From Bloomberg:

S&P/Case-Shiller U.S. Home-Price Index Falls 14.4%

Home prices in 20 U.S. metropolitan areas fell in March by the most in at least seven years, pointing to weakness in the housing market that will constrain economic growth.

The S&P/Case-Shiller home-price index dropped 14.4 percent from a year earlier, more than forecast and the most since the figures were first published in 2001. The gauge has fallen every month since January 2007.

Prices continue to slide as record foreclosures put more homes on the market and stricter lending standards make it harder to get loans. Falling home values are slowing consumer spending, threatening to halt the six-year expansion.

“Many households are putting their home-buying plans on hold, given the expectations that the house price corrections will persist,” Celia Chen, an economist at Moody’s Economy.com in West Chester, Pennsylvania, said before the report. “The housing downturn remains in full swing.”

Prices dropped 2.2 percent in March from a month earlier, after a 2.6 percent decline in February, the report showed. The figures aren’t adjusted for seasonal effects, so economists prefer to focus on year-over-year changes instead of month-to- month variations.

From Bloomberg:

New-Home Sales in the U.S. Rose 3.3% to 526,000 Pace

New-home sales in the U.S. unexpectedly rose in April after readings for the prior month were revised down, signaling a worsening housing slump is still a threat to the economy.

Sales increased 3.3 percent to an annual pace of 526,000 from a 509,000 rate the prior month that was the lowest in 17 years, the Commerce Department said today in Washington. A separate report today showed home prices dropped in the first quarter by the most in at least 20 years.

Concern about declining home values and stricter loan rules are limiting demand and foreclosures are throwing even more properties on the market. Federal Reserve policy makers view the prospect of larger decreases in house prices and the effect that would have on financial institutions as a “key source” of risk to growth.

“There’s certainly more room for declines in home sales,” Adam York, an economist at Wachovia Corp. in Charlotte, North Carolina, said before the report. “People will be reluctant to buy, lenders will be reluctant to lend. We don’t think a leveling out in the housing market is coming anytime soon.”

Now Open, Part II!

Prior weekend thread closed due to comment overflow