From Bank of America:

The rise of Boomers as the main homebuyer

The latest Home Buyers and Sellers Generational Trends report from the National Association of Realtors found that for the first time since 2014, Baby Boomers overtook Millennials as the generation with the biggest share of homebuyers. From July 2021 to July 2022, 39% of surveyed homebuyers were Baby Boomers, followed by 28% of Millennials and 24% of Gen X (Exhibit 6).

The rise of Baby Boomers as the primary homebuyers can be attributed to three main reasons. First, as this generation retires, they move closer to family and friends. Second, demand for smaller homes increases as their children move out. Last but not least, Baby Boomers hold the greatest wealth across generations at $73 trillion in 4Q 2022, eight times that of Millennials (Exhibit 7). In the current environment of high home prices and interest rates, Baby Boomers are better equipped financially for home purchasing. In fact, only 49% of older Boomers (68-76 y/o) financed their home purchase in 2022, compared with 93% of those aged 33-42 y/o, according to the same National Association of Realtors report.

Given the importance of Baby Boomers in the housing market, where are they moving to?

The generational breakdown of Bank of America internal data suggests Baby Boomers’ migration patterns over the past few years have been different from other generations. Specifically, while Austin continues to attract inward migration overall, the number of Baby Boomers in the city has declined over the past year. The exodus of the group with the most cash could have added to the downward pressure on Austin’s home prices over the last year.

Las Vegas, Phoenix, Tampa, and Orlando are among the most popular destinations for Baby Boomers, according to Bank of America internal data (Exhibit 8). Note that the pace of migration slowed for Vegas and Phoenix over the past year, but was relatively unchanged for Tampa and Orlando. In our view, this could partly explain the still resilient home price appreciation in Tampa and Orlando relative to other cities.

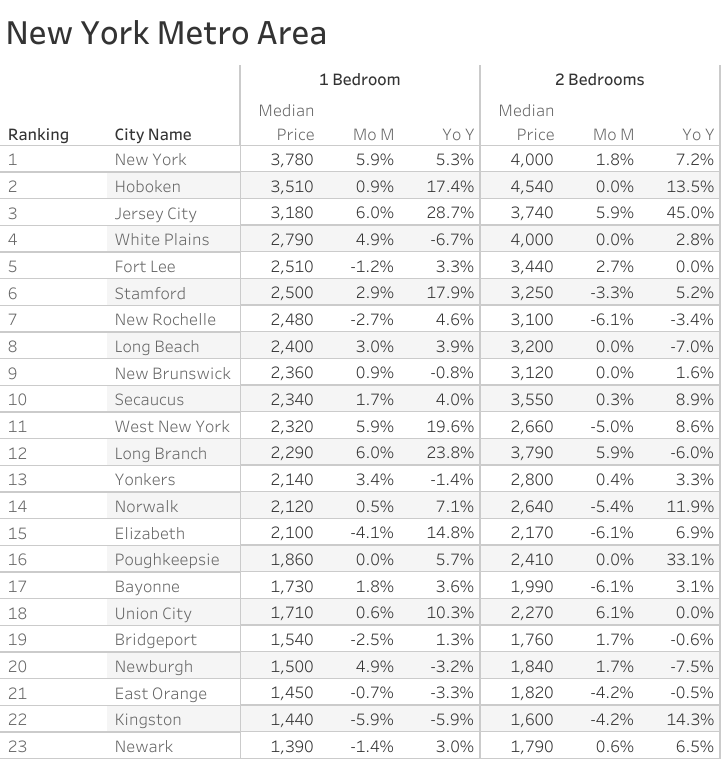

Alternatively, Baby Boomers, similar to other generations, are leaving some of the largest cities in the US, including the Bay area, New York and Seattle (Exhibit 9).

Millennials will likely drive home buying in the longer term

Source: Bank of America internal data

For Millennials, the most popular destination for domestic migration is Austin, with the number of Millennial customers up 16% in 1Q 2023, relative to three years ago, which led other cities by a wide margin. Cleveland, Tampa, and Dallas each saw a 6% increase in Millennial population over the past three years.

In the near term, many of this cohort are staying on the home buying sidelines. A recent Bank of America Global Research survey found that increasing concerns about affordability are the top reason many Millennials are staying out of the housing market. But hopeful buyers who may be waiting for the market to cool are still forging ahead in their own way. In a separate Bank of America 2023 Homebuyer Insights Report, over half of respondents who are not planning to purchase a home in the near term are still actively scrolling through real estate marketplace apps.

This means that demand for home purchasing will likely return when we move past the current housing cycle, especially in the case of younger Millennials, who are entering prime home buying age. In 1Q 2023, the home ownership rate for those younger than 35 years old was 39%, 23 percentage points lower than that for 35–44-year-olds.

{kind=link}