From the NYT:

Homeownership, the Key to Happiness?

If trying to buy an apartment in New York City has been making you miserable, consider this: actually getting that home may not make you happy.

A growing body of research suggests that spending money on real estate doesn’t necessarily mean investing in contentment. Indeed, the conventional advice to cut back on vacations, restaurant meals and other extras in order to save money for a home may actually be detrimental to felicity. Experts in happiness — an increasingly popular field focused on the scientific understanding of emotional well-being — say that people are happier when they spend money on experiences instead of material goods, whether it be a new car or a bigger apartment.

“People are making so many trade-offs in order to have that home,” said Elizabeth Dunn, an associate professor of psychology at the University of British Columbia who studies consumerism and happiness. She recently explored the impact of housing on people’s happiness while compiling studies for a new book, “Happy Money: The Science of Smarter Spending,” which she wrote with Michael Norton, who teaches at the Harvard Business School.

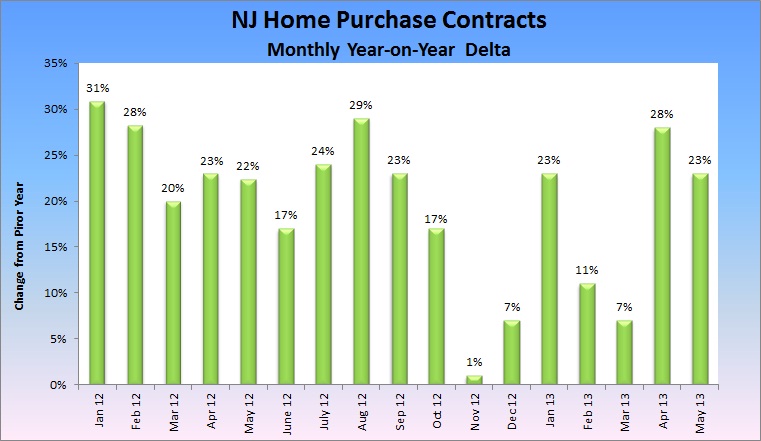

The recession forced many people to curb their spending habits and re-evaluate their overall lifestyles. But after saving money for years, buyers encouraged by low mortgage rates are re-entering the housing market. They find the pickings slim. In Manhattan, the number of apartments for sale for the second quarter was at a 13-year low, stoking competition and driving up prices.

Now there is research like Dr. Dunn’s, emphasizing that when it comes to your overall happiness, “there are a lot of better things you could be putting your money toward” than real estate.

This isn’t necessarily bad news in a place like New York City, where nearly 70 percent of the housing stock is rentals. And it may offer some solace to frustrated buyers facing bidding wars and all-cash offers they simply can’t top.

“People still view housing as a central component of happiness and a critical aspect of the American dream,” Dr. Dunn said. “But there is little research to support that.”

A 2011 study of about 600 women in Ohio found that homeowners weren’t any happier than renters. The study was conducted by Grace Wong Bucchianeri, then an assistant professor of real estate at the Wharton School at the University of Pennsylvania. Indeed, homeowners spent less time on leisure activities with friends and reported that they derived some pain from homeownership. What exactly caused that pain wasn’t indicated in the study, but financial experts say that people who make the leap from renting to buying can be caught off guard by the nuts and bolts.

“The reality of maintenance and repairs, and being ‘house rich but cash poor,’ can negate much of the perceived happiness people may have had about homeownership,” said Greg McBride, the senior financial analyst for Bankrate.com. Even if a low mortgage rate means you spend less each month than you did when renting, upkeep can drain a bank account faster than a leaking water heater.