Heading down to Delaware for the day, and I should have already hit the road. Therefore:

Tuesday Open Discussion

You know the rules, have fun.

Heading down to Delaware for the day, and I should have already hit the road. Therefore:

Tuesday Open Discussion

You know the rules, have fun.

From the Star Ledger:

Recession causes houses of faith to flood N.J. realty market

The latest entries in the New Jersey real estate market feature some unusual amenities.

A two-floor building in Seaside Heights comes with a baptismal pool, as well as a few “open sitting/reading areas.”

In Montclair, a 16,133-square-foot property includes Palladian windows and a large wood-paneled conference room.

There’s a basement meeting hall and “main sanctuary” in an Audubon facility overlooking Hidden Lake Park — on sale for $490,000.

The three church properties are just a sample of the many houses of faith that have come on the market in New Jersey alongside a flood of foreclosed residences. Experts point to a range of factors, from long-developing demographic shifts to a drop in donations during a tough recession.

“A lot of congregations, especially in smaller churches, have older populations, so they can no longer afford to maintain large properties,” said Mark Kotzas, a broker for Crossroads Realty in Ocean County, which is handling the sales of several faith centers, including Grace Evangelical Church, the one advertising the baptismal pool.

…

Brokers say the hurdles in selling religious properties are often different from private home sales. There are fewer potential buyers in the market; decisions are often made by committees in the congregation; zoning restrictions may prevent certain properties from being converted.“How do you value these properties?” said John Roedig, a partner with the May Commercial Group and the broker for the Grace Tabernacle Church in Audubon. “You have some general assumptions about a two-story Colonial house, but what can you say about a 20,000-square-foot building’s price?”

“Banks have gotten so strict in their lending,” said Drew Knapp, an agent with Century 21 Commercial Real Estate in Caldwell.

From the Star Ledger:

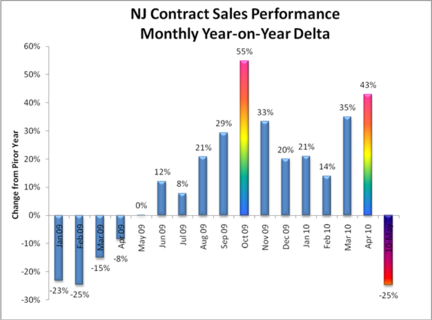

After tax-credit expiration; NJ pending home sales dip

Pending sales of New Jersey homes dropped by the greatest margin since February 2009 — when the U.S. economy shed more than 726,000 jobs, according to an East Bruswick-based appraisal firm.

Jeffrey Otteau, president of the Otteau Valuation Group, said about a fourth fewer buyers signed contracts for real estate in the state last month compared to a year ago.

“We had a full year of improvement in housing, so that means that today’s buyers, (potential homeowners) can’t get the same deals they could get six months ago,” Otteau said. “What buyers are saying is that the economy isn’t good enough for me to go forward without a tax credit.”

From Bloomberg:

Manhattan Empty Condos May Become Rentals as Leases Beat Sales

When Richard J. Bailes and his family paid $4.1 million in March for a four-bedroom apartment in the glass and steel Georgica on Manhattan’s Upper East Side, just eight of the building’s 58 units were occupied, he said.

Bailes and his family had plenty of places to choose from. About 8,700 new condos sit empty in Manhattan, with 75 percent not even listed for sale yet, said appraiser Miller Samuel Inc. Priced at levels the market no longer supports, they’re selling so slowly it would take as long as seven years to find buyers for them all, said Jonathan Miller, president of Miller Samuel.

…

Builders can’t afford to cut prices because they borrowed too much at the height of the market, according to Miller. He and his partners are betting that lenders will seek to sell their condo units at a loss rather than foreclose on the building and assume all the developer’s liabilities until the units are sold.Developers taking out construction loans borrow an additional amount for interest reserves, which is intended to cover the monthly payments on the loan while the project is under construction and until sales begin, Miller said. Alpert estimates that reserves on loans made in 2007 and 2008 will dwindle in the second half of 2010 and early 2011.

…

The relationship between home prices and rents typically remains steady within a market, Miller said. In Manhattan, the average apartment, adjusted for inflation, cost 8.1 times annual rent from 1991 to 1997, according to Miller Samuel data. That means that in those years, buyers in Manhattan concluded that the long term benefits of owning an apartment — tax savings and property appreciation — were worth an initial investment of eight times the cost of renting.Then in 1998, Manhattan prices began a decade-long climb, with year-over-year values rising by 10 percent or more in most quarters. By the second quarter of 2008 apartment prices peaked at 22.4 times annual rent, according to Miller Samuel data.

…

At that level, buying rather than renting in Manhattan only makes sense if the purchaser expects prices to continue rising at a meteoric clip, with future sales’ profits justifying ownership costs that also include property taxes, interest and maintenance fees. New York is the No. 1 city in the U.S. where the overall costs of buying are “significantly more expensive than renting,” according to a report released yesterday by property website Trulia.com.Manhattan’s multiple in the first quarter of 2010 was 19 times rent, even as rental prices fell 6.1 percent from a year earlier, according to data from Miller Samuel.

“That suggests a few things,” Miller said. “One is that prices are poised to slip further.”

The median value of apartments for resale in Manhattan has already fallen 31 percent since 2008, narrowing their spread over rents, Miller said. By comparison, apartments in new developments, which are saddled by debt for construction loans made during the property boom, have fallen by 24 percent — and much of that drop was due to smaller units being sold rather than significant price reductions by the developer, Miller said.

…

The 8,700 unsold new condos in Manhattan exceed all residential sales in the borough in 2009, according to Miller. About 6,500 of those units are “shadow inventory” and have not yet been listed for sale, he said.“If you flush that all into the market you tank the market,” Westwood’s Alpert said. “So the only way you can effectively push that into the market is to bleed it out very slowly. Well, the lenders don’t really have the option to bleed it out slowly because they can’t hold onto it for six years.”

…

“New York is Miami ‘08 right now,” said Peter Zalewski, principal of Condo Vultures LLC., a Bal Harbour, Florida, real estate brokerage and consulting firm specializing in bulk sales.

From the WSJ:

New Jersey Leads Tri-State in ‘Seriously Delinquent’ Mortgages

New Jersey’s mortgage loans that were “seriously delinquent,” meaning they are 90 days or more delinquent or in the foreclosure process, stood at 10.73% during the first quarter, leading the tri-state area, the Mortgage Bankers Association said Wednesday.

Connecticut and New York did better than the national averages, with seriously delinquent loans running at 8.13% and 8.94%, respectively.

The MBA said New Jersey was third in the nation for homes in foreclosure, with 6.17%. Florida had 13.97% and Nevada was at 10.40%.

From Housing Watch:

Home Price Recovery Will Take Three Years, Morgan Stanley Says

There’s more pain ahead for the housing markets, according to a recent report from Morgan Stanley.

How likely is this nightmare, and what can you do with this information?

“We see potential for another 5-10% decline in nominal prices over the next year,” said the authors of “U.S. Housing Strategy: The Long Road Home,” an analysis out this month from Morgan Stanley.

Even after home prices hit bottom, Morgan Stanley’s experts think home prices will stay low “for another three to four years, during which annual appreciation may reach only as high as inflation or income growth.”

Only a few economists still expect a big drop to home prices this year, though most expect prices to sag.

Morgan Stanley is on the pessimistic end of housing forecasts with its prediction of a potential drop of 5 to 10 percent. A decline like that would drag down the closely watched Case Shiller Home Price Index to between 136 and 129.

Other housing economists have softened their forecasts. In December, Mark Zandi, chief economist of Moody’s Analytics, predicted that home prices had a long way to fall before hitting bottom this autumn — down more than a third from its housing boom peak. His prediction back then, in an interview with Reuters, would have sunk the 20-city Case Shiller Index to about 128 — more than 10 percent down from its current level.

Zandi now predicts that, “Home prices nationally may still fall somewhat lower,” according to a recent interview with the Los Angeles Times. That’s a big change from the painful drop he predicted before.

From the NYT:

Owners Stop Paying Mortgages, and Stop Fretting

For Alex Pemberton and Susan Reboyras, foreclosure is becoming a way of life — something they did not want but are in no hurry to get out of.

Foreclosure has allowed them to stabilize the family business. Go to Outback occasionally for a steak. Take their gas-guzzling airboat out for the weekend. Visit the Hard Rock Casino.

“Instead of the house dragging us down, it’s become a life raft,” said Mr. Pemberton, who stopped paying the mortgage on their house here last summer. “It’s really been a blessing.”

A growing number of the people whose homes are in foreclosure are refusing to slink away in shame. They are fashioning a sort of homemade mortgage modification, one that brings their payments all the way down to zero. They use the money they save to get back on their feet or just get by.

This type of modification does not beg for a lender’s permission but is delivered as an ultimatum: Force me out if you can. Any moral qualms are overshadowed by a conviction that the banks created the crisis by snookering homeowners with loans that got them in over their heads.

“I tried to explain my situation to the lender, but they wouldn’t help,” said Mr. Pemberton’s mother, Wendy Pemberton, herself in foreclosure on a small house a few blocks away from her son’s. She stopped paying her mortgage two years ago after a bout with lung cancer. “They’re all crooks.”

From the Record:

North Jersey luxury homes languish on the market

Looking for a bargain?

Actor Eddie Murphy’s 30-room Englewood mansion, which went on the market in 2004 for $30 million, can be yours for $12.75 million.

And hip-hop entrepreneur Russell Simmons’ 35,000-square-foot mansion in Saddle River — offered for $23.9 million in 2007 — is now listed for $13.9 million, not much more than the $13.5 million Simmons paid in 2001.

Although it once seemed that markets catering to the richest Americans would be immune to an economic downturn, the recent history of North Jersey’s luxury home market tells a different story. As stock portfolios swooned last year and Wall Street cut thousands of jobs, wealthy people held off on buying multimillion-dollar homes. As a result of the slower demand, prices have plummeted, often by millions of dollars.

“I didn’t feel that at this level of income, people would be affected,” said Stephanie Rosken of Prominent Properties Sotheby’s International Real Estate in Tenafly. “But the market that I felt was not going to be affected was very much affected by this volatile economy. Very, very little is selling.”

In 2007, 143 homes sold for more than $2 million in Bergen County, and 10 for over $5 million. In 2009, only 57 sold for more than $2 million and only three for more than $5 million, according to figures from the New Jersey Multiple Listing Service. So far this year, sales are running at about the same pace as 2009.

Jeffrey Otteau, an East Brunswick appraiser who tracks the real estate market statewide, recently estimated that there is a seven-year supply of properties priced above $2.5 million in Bergen County.

From the WSJ:

Despite Bust, Ordinary Joes Still Can’t Afford Stately Homes

One of the disappointing aspects of a housing bust is that it doesn’t actually mean ordinary Joes can now afford stately homes with views of the Golden Gate Bridge or luxury apartments overlooking Central Park in Manhattan.

As we report in Friday’s Journal, prices have come down on nearly all types of homes, but there is still pretty fierce competition for homes in coveted neighborhoods with décor that would make the editors of Architectural Digest drool. That proves there are still more wealthy people than there are great homes in the best neighborhoods. The homes that are selling for peanuts generally are in places where the well-heeled don’t wish to bed down.

So far, indeed, the biggest price cuts have come at the lower end of the market. The S&P/Case-Shiller indexes show that home prices in the lower tier of the market in the Miami area are down 61% from the peak, while the upper tier is down 42%. In the Las Vegas area, the lower tier is down 64% and the upper tier 52%. In the New York area, prices are down 27% for the hoi polloi and 17% for the hoity-toity. In Los Angeles, they’re down 53% for the riffraff and 28% for the stars.

Now, some experts say that’s merely because the low end has already adjusted to reality while the high end is still in the clouds. And it is quite possible that prices on poorly located McMansions will have to come down hard to attract buyers. But in the ritziest neighborhoods, don’t look for prices to crash.

…

New Jersey has a 35-month supply of homes priced at $2.5 million or more, says Jeffrey Otteau, president of Otteau Valuation Group Inc., an appraisal firm in East Brunswick, N.J. That compares with a seven-month supply for the New Jersey housing market as a whole. Mr. Otteau says luxury sales are recovering more slowly than the rest of the market, partly because the state has lost many high-paying jobs in recent years.Though Mr. Otteau expects the luxury market in New Jersey to improve in the near term, he says it faces another slump within about five years as baby boomers are forced to sell big homes to cut their living expenses and fund retirement. “We’ve got another wave of houses coming on the market over the next five years,” he says.

From AOL News:

Would You Want to Live in a Serial Killer’s House?

If you’re in the market for an “excellent handyman’s special,” you might want to check out a two-story ranch-style house that’s for sale in East Meadow, N.Y. What the property listing doesn’t mention, though, is that Joel Rifkin, one of the area’s most notorious serial killers, used to live here.

Nor does it have to, under New York’s disclosure laws, despite the fact that prospective buyers might think twice upon learning of the home’s sinister past.

“There is no requirement under New York law to notify a purchaser or a respective purchaser of a murder, death or unpleasant act that occurred in the home,” notes Adam Leitman Bailey, an attorney who practices real estate law in New York and New Jersey. “New York is a caveat emptor [buyer beware] state.”

…

According to TruTV’s Crime Library, while some of Rifkin’s victims were killed in his vehicle, others were slain and dismembered inside his East Meadow home.

…

Coincidentally, the “Amityville Horror” house is also for sale in New York, for $1.15 million. The home is the site of a brutal 1974 mass murder, in which Ronald DeFeo Jr., then 23, murdered six of his family members. The crime and subsequent alleged supernatural incidents were detailed in several books and movies.Previous owners of the Amityville home had the address changed and made modifications to the exterior in an attempt to make it difficult to identify. Nonetheless, the house continues to attract tourists.

…

Not everyone, however, is completely against the idea.“I would definitely buy the house. It’s a part of true crime history, much like the Lizzie Borden Bed & Breakfast,” Jessika Gein told AOL News. Gein and her husband, Eric, own Serial Killers Ink, a leading “murderabilia” outlet.

From the Record:

Home prices in NY Metro area down 2.4 percent from last year

Home prices in the New York metropolitan area, which includes North Jersey, declined 2.4 percent in March from a year earlier, the Standard & Poor’s Case-Shiller index said today.

Nationally, home prices rose 2.3 percent from a year earlier.

Case-Shiller does not break down price data by county, but Bergen and Passaic counties saw small increases in home prices in March. According to the N.J. Multiple Listing Service, the median price of a single-family home in Bergen County was $395,000 in March 2010, up 2 percent from a year earlier. The number of sales rose 41 percent, to 342.

In Passaic County, the median price was $295,883, up 3 percent from a year earlier. The number of sales rose 70 percent to 202.

The volume of home sales was boosted by an $8,000 federal tax credit for first-time home buyers, as well as a $6,500 credit for repeat buyers. Both credits expired April 30, and analysts say demand for homes may drop as a result.

“The housing market may be in better shape than this time last year; but when you look at recent trends, there are signs of some renewed weakening in home prices,” said David M. Blitzer, chairman of the index committee at Standard & Poor’s. “In the past several months, we have seen some relatively weak reports across many of the markets we cover.”

From the Daily Record:

State revenues continue to fall short

State revenues continue to fall below projections, putting New Jersey in potentially tighter budget squeeze.

A new analysis by the nonpartisan Office of Legislative Services predicts that taxes and other revenue for the budget year that ends June 30 will be $402 million less than Gov. Chris Christie’s administration had expected.

The falling revenue won’t necessarily require immediate budget cuts, but it would largely eliminate the state’s current surplus of $500 million.

However, the OLS also estimates that revenue for the fiscal year that begins on July 1 will be $365 million less than the Christie administration projects.

Of the major state revenues, income taxes are experiencing the largest drop-offs, according to the OLS.

If those revenue projections prove true, then cuts beyond the already severe reductions proposed by Christie for the next fiscal year would be required to balance the state budget. The state Constitution requires the budget to be balanced every year.

From the Star Ledger:

Unexpected N.J. budget shortfall will likely force cutbacks

New Jersey’s budget picture is getting even uglier, with a projected $765 million shortfall during the next 13 months, according to figures to be released today.

An internal memo obtained by The Star-Ledger shows the bulk of the problem — $402 million, driven by a steep drop-off in income tax collections — must be dealt with before the current fiscal year ends June 30.

The state is also projected to bring in $365 million less than Gov. Chris Christie forecast in his already austere $29.3 billion budget proposal for next year, according to the memo by the nonpartisan Office of Legislative Services.

Sen. Paul Sarlo, chairman of the Senate budget committee, said the new figures were a “major setback.”

“I don’t believe anybody was expecting this,” said Sarlo (D-Bergen). “This is a significant, significant setback to the budget process.”

From the Asbury Park Press:

Seaside sees good times when MTV show returns

Filming of the MTV reality series “Jersey Shore” doesn’t begin here until July, but local business leaders Monday night rolled out the red carpet for the next season of the show.

About 60 people, including network representatives, assembled at the Spicy Cantina on the boardwalk to pledge support for the sometimes controversial show that has garnered its share of headlines since premiering in 2009.

A lot has changed here in a year: Few outside of the business community were even aware of the series production schedule at this time in 2009.

But from an economics perspective, “Jersey Shore” has been a boon for this resort town as the location of the show.

“It’s been an amazing thing to see down here, with tourists coming from all around the country, wearing and purchasing T-shirts,” said Michael Loundy, one of the hosts of the dinner and a broker at Seaside Realty. “The series has been great for the business community and the town of Seaside Heights.”

…

“Last year we invested about $4 million into the local economy and purchased over 20,000 meals during production,” Salsano said. “I’ve been to the Shore a lot in my life and Seaside Heights is what I think of when I think of the classic Jersey Shore town.”

…

Loundy said last month the house on Ocean Terrace, which has six bedrooms and three bathrooms and a 12-person occupancy, rents for $12,000 per three-day holiday weekend — a rate roughly 33 percent higher than a comparable beachfront property.

From the Asbury Park Press:

NJ unemployment: N.J. added 10,500 jobs in April, unemployment rate held steady

New Jersey’s economy added 10,500 jobs in April, and its unemployment rate remained stable at 9.8 percent, the state Department of Labor and Workforce Development reported Wednesday.

The report was a sign that the economy is in a recovery, albeit a choppy one. A wide range of private-sector companies accounted for the bulk of the hiring.

“Employers in New Jersey — at least some segments — have finally gained confidence in the sustainability of the recovery,” said Patrick J. O’Keefe, an economist and partner at J.H. Cohn, a Roseland-based accounting firm.

…

The New Jersey labor market was decimated during the national recession that began in 2007 and cost the state almost 230,000 jobs. But the report released Wednesday showed that hiring in April was at its strongest pace in two years.

…

The huge job gain came a month after the state lost 4,900 jobs, showing the recovery remains tenuous. But economists said it is headed in the right direction. New Jersey lost 100 private-sector jobs during the first four months of the year, compared with a loss of 71,700 private-sector jobs during the first four months of 2009, Rutgers University economist James W. Hughes said.“At least we’re looking at a recovery now and the recession is in the rearview mirror,” Hughes said. “However, we’re still probably a long way from gangbusters.”

Sectors with the biggest gains: Professional and business services added 3,700 jobs, manufacturing added 2,500 jobs and financial activities added 1,100 jobs. The public sector added 2,400 jobs, most of which came from hiring by the U.S. Census Bureau.

From the Daily Record:

A mighty Oak: Fully restored, historic Empire-style Victorian on market for $499,000

Four years ago, Bob and Michele Pulis bought a historic, circa-1818 house atop Schooley’s Mountain in Long Valley. Vacant for 40 years, the Oak Cottage was in serious disrepair, its only residents a family of raccoons.

“I can remember standing out there and just looking up at the (house),” Bob Pulis says. “It was sad. It was like (it was saying), ‘C’mon, man, help me.’ ”

Bob and Michele saw beyond the overgrown landscape, rotting wood and mounds of raccoon droppings to the Victorian charm the house exuded in its heyday. According to local lore, visitors to the three-story, 13-room home, with its distinctive mansard roof and shingled cedar siding, may have included Ulysses S. Grant and his family. This was when Schooley’s Mountain was an elite summer community.

The couple had just finished building their own house in Jefferson, but they wanted what Michele calls “one more family project.” So they decided to rescue the historic property, once known as “The Gem of the Mountain.” They would spend the next 3-1/2 years — and more than $525,000 — restoring the Oak Cottage to its former glory.

Last Memorial Day weekend, they proudly showed the refurbished Empire-style Victorian to more than 1,000 potential buyers. Its list price was $885,000.

“We bought it right at the peak of the market. We never foresaw an economic apocalypse coming,” Michele says.

Today, the Oak Cottage is still for sale — for $499,000.