From CNN:

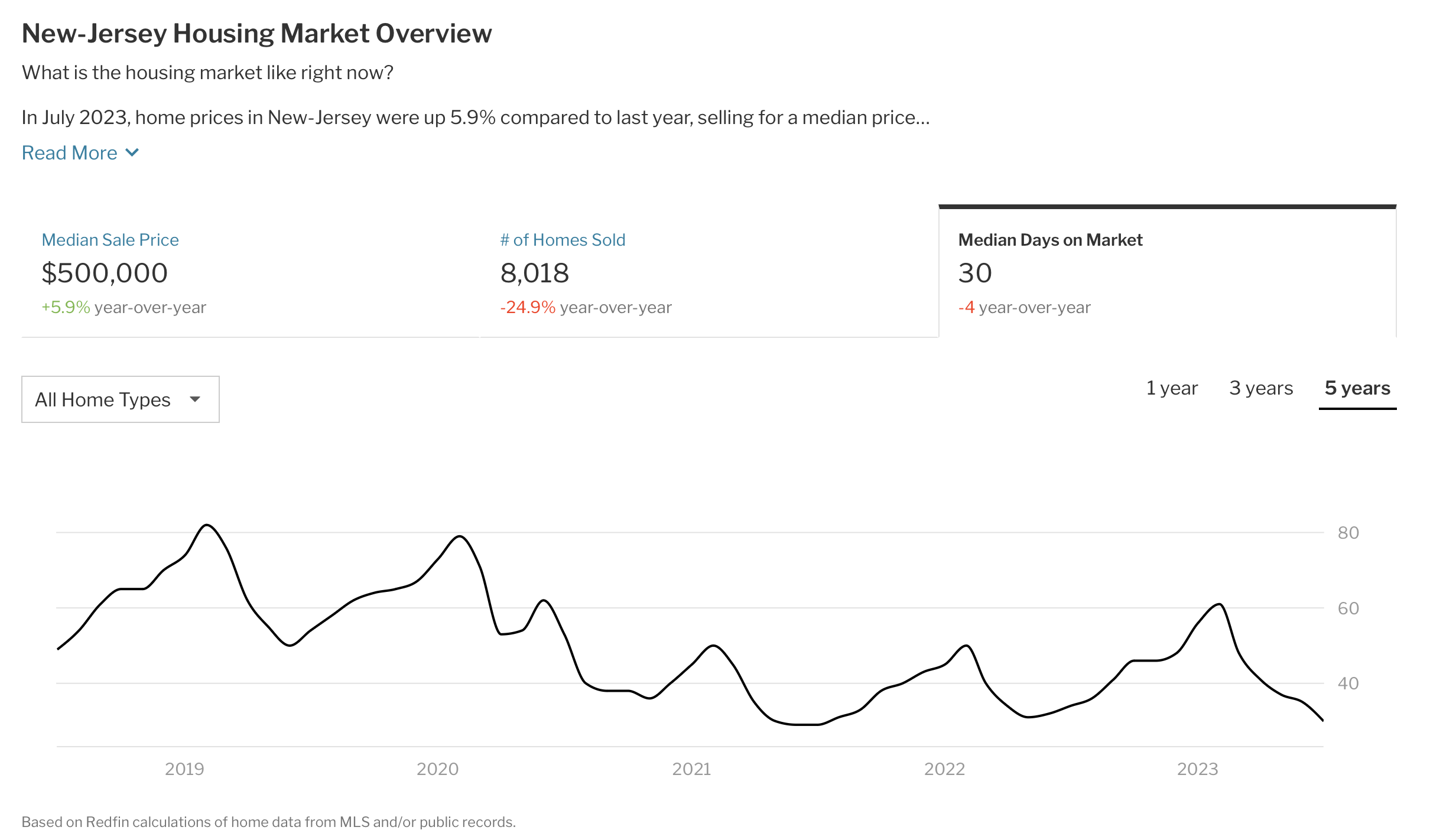

US home prices rose in July to record-high levels

US home prices continued to rise in July, hitting a new record high and marking the sixth successive month of gains, as historically low inventory pushes up the cost of a home.

Prices rose 0.6% from the month before, according to seasonally adjusted data from the S&P CoreLogic Case-Shiller US National Home Price Index released Tuesday.

Compared to a year ago, the national composite index also rose, with prices up 1% from July 2022, the prior peak, according to Case-Shiller data. It was followed by home prices that fell through January of this year, declining by 5% over those seven months.

“The increase in prices that began in January has now erased the earlier decline, so that July represents a new all-time high for the National Composite [index],” said Craig Lazzara, managing director at S&P Dow Jones Indices, in a statement.

What’s more, he added, the recovery in home prices is broadly based. As was the case last month, 10 of the 20 cities in the sample have reached all-time high levels. In July, prices rose in all 20 cities after seasonal adjustment.

Cities with the most price appreciation in July from the year before were Chicago, up 4.4%; Cleveland, up 4.0%; and New York, up 3.8%. The same three cities also saw the most appreciation in June.

At the other end of the spectrum, the cities with the largest price year-over-year price drops in July were in the West. Prices in Las Vegas were down 7.2% from a year ago and in Phoenix prices were down 6.6%.

The Midwest, where prices were up 3.2% in July from a year ago, continues to see the most price strength. It is followed by the Northeast, up 2.3%. The West, where prices are down 3.8% from a year ago, and the South, with prices down 3.6%, continue to see annual price declines.

National home prices have risen 5.3% since January, but the monthly increases are not as big as they were earlier this year. This is because higher mortgage rates have put pressure on affordability, said Selma Hepp, chief economist at CoreLogic.