There appears to be some thought that home prices on the coasts are elevated or subsidized through the use of the Mortgage Interest deduction (MID) and State and Local Tax (SaLT) deductions. These two deductions, either alone or together, artificially increase the price of homes making them less affordable. Without the “subsidies”, prices would fall, increasing affordability, which is better for everyone (except the people that currently own the homes).

I would argue that this would not be the case, that eliminating SALT and MID would cause the opposite. Not because removing the deductions wouldn’t cause prices to fall, they would. But because removing SALT and MID right now, would cause a seize up in the housing market, further removing inventory from the market, reducing supply. This would likely be the unexpected consequence of eliminating those deductions. With home prices remaining at current levels, or even increasing as supply is restricted, along with the elimination of deductions – housing is now even less affordable.

Why?

If prices fell, owners would continue to sit on properties until values recovered. We are seeing this phenomenon across many real estate markets in the US. This shouldn’t be a surprise, we’ve only been talking about it for the past 5 years. Because values have not recovered, sellers either financially can’t sell the properties (under water, near negative equity, not enough equity to move), or psychologically (I’ll never sell it for less than it’s worth). In many regions we’re finally starting to see markets start to move again as values recover. Should prices stall, or fall, this impact of restricted supply will continue to impact the market for many more years (until prices recover).

For-purchase supply may also transition to for-rent supply as investors purchase more homes, due to the fact that corporate tax structure would favor corporate ownership of housing over individual ownership of housing. As investors purchase these homes and convert them to rentals, you further constrain housing inventory, pushing prices up as supply dwindles.

This would also create a strain on move-up buyers, causing them to remain in place as they now find that the marginal increase in housing costs to upgrade is no longer affordable or realistic, so now you have a large portion of owners who would have previously moved-up staying in place. You might also see a follow-on trend of expansion and renovation of existing housing stock in lieu of moving to a larger house. This has the overall negative effect of increasing the average cost of local housing stock (through renovation you turn a less expensive house into a more expensive house, that less expensive house is forever gone).

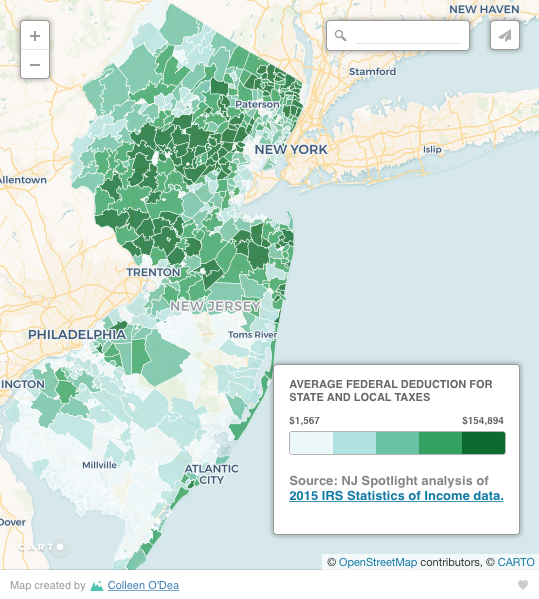

In places like NJ, where a very large portion of older/retired owners no longer have a mortgage and don’t claim the MID, these individuals would see no significant increase in housing costs that would cause them to sell their homes and downsize. This means a big chunk of current inventory does not see any precipitating factor to put their homes on the market. In fact, if the standard deduction increases, retirees might find it less expensive to remain in place, further amplifying the impact of reduced inventory.

We may also see an impact to increased rental prices as renters who don’t currently itemize see benefits of the increased standard deduction, this may manifest as increasing rental rates in areas with high rental demand. So, both sides of the affordability picture are impacted.

So there you have it, eliminate the MID and SALT, and housing becomes even more unaffordable. Believe me, the unintended consequence will prevail here. You cannot evaluate these types of scenarios as an either-or situation, even though logically you might want to. The problem is, the cat is already out of the bag, the deductions exist. You are not comparing two hypothetical situations, one with the deduction and one without, you are looking as a third situation, one where it existed, and now no longer exists – the outcome here will be very different than if it had never existed at all.

Elimination of these deductions without major short-term impacts would require removal of these at a slow, measured pace – for example, a 10 year phase-out based on income, with the income-based limits falling every year. I completely don’t understand why we have discussions involving broad changes rapid one-time events when we know that implementing these kinds of changes in a measured pace results in significantly easier to manage situations, without the risk of unintended consequence.

But hey, what do I know?