With all eyes on the market this morning, why bother posting something about real estate.

Predictions for closing prices on the Dow, S&P, Gold and Oil are due in by noon.

With all eyes on the market this morning, why bother posting something about real estate.

Predictions for closing prices on the Dow, S&P, Gold and Oil are due in by noon.

From the NY Times:

In Home Sales, Courtesy Goes a Long Way

ANYONE who has stepped into the often-stressful real estate market in New Jersey lately can hardly help being aware that it is an increasingly rude arena.

With the supercilious buyers, hypersensitive sellers, inconsiderate sales agents and adversarial lawyers, “it really can be a jungle out there,” said Roberta Plutzik Baldwin, a broker for Keller Williams Realty in Montclair, somewhat ruefully.

“In a climate like this, where so many people feel financial anxiety, and sometimes every $100 is an important issue,” she said, “anger and animus seem to come out more frequently.”

Even when people have “tons of money,” said Karen Eastman Bigos, a broker for Towne Realty Group in Short Hills, more and more are “harsh” with remarks and attitudes, especially buyers.

Yet Ms. Bigos and Ms. Baldwin were among a number of real estate professionals emphasizing that courtesy still counts a lot and can sometimes be crucial to getting a deal done at all.

“Many, many times,” Ms. Bigos said, “I’m seeing deals turn on politeness, or the lack of it.”

…

Ken Baris of Jordan Baris Realtors in West Orange said, “Huge, huge — courtesy is huge.” He recalled selling a house a couple of years ago for a professional hockey player to a buyer who had been taken with the property. The buyer had explained in a warm letter how much it would mean to live in the player’s house. Even though a competing bidder offered $100,000 more during the three-day attorney-review period mandated in New Jersey, the player went with the letter-writing buyer.

…

Even if everyone is civil, or even gracious, during the precontractual phase, things can get strained when lawyers enter the picture, several brokers pointed out. In today’s market, much of the wrangling over price actually takes place after a buyer has a home inspection done — whereupon a lawyer writes a letter demanding that the seller either pay for repairs or offer a price discount.“A seller gets a scathing letter from an attorney saying ‘this, that and the other, and more’ has to be fixed, and a seller can be offended,” said Susan Hughes Hunter, the vice president of Lois Schneider Realtor in Summit.

“People feel this is their home, their blood, sweat and tears,” she noted, “and this letter makes it look like the house is falling down. The way attorneys speak is black-and-white, and in truth, it’s not really their job to say, ‘Oh, please, we would so love it if you would be kind enough to fix your roof.’ ”

…

Ms. Baldwin of Keller Williams says she always urges both buyers and sellers not to take such things personally, and to “think of a real estate sale as business, nothing more.”

From Bloomberg:

U.S. Jobs Gain Seen Too Small to Cut Jobless

American employers probably failed to create enough jobs in July to reduce the jobless rate, showing anxiety over government debt deliberations and a slowdown in consumer spending have shaken confidence, economists said before a report today.

Payrolls climbed by 85,000 workers after an 18,000 increase in June that was the smallest this year, according to the median forecast of 88 economists surveyed by Bloomberg News before a Labor Department report. The jobless rate held at 9.2 percent after rising in each of the previous three months.

Limited job gains and concern the economic recovery will be cut short led U.S. equities to their biggest slump since February 2009 yesterday. Slowing growth puts more pressure on Federal Reserve policy makers meeting next week to try to steer the world’s largest economy away from another recession at a time when inflation is also accelerating.

“The labor market is slowing towards stall speed,” said Patrick O’Keefe, chief economist at J.H. Cohn LLP in Roseland, New Jersey. “Employers were certainly seeing a decline, or leveling off, in demand for goods and services.”

The Labor Department’s data are due at 8:30 a.m. in Washington. Bloomberg payroll survey estimates range from no change to a 150,000 increase.

From CNBC:

Plunging Mortgage Rates Won’t Juice Housing

The one positive in all the uncertainty surrounding the nation’s debt was a plunge in Treasury yields, which in turn sent mortgage rates to record lows.

The 30 year fixed hit a near-low of 4.45 percent last week from 4.57 percent, and the 15 year made a new low of 3.52 percent, according to the Mortgage Bankers Association. Those low rates pushed refinance applications up 7.8 percent and purchase applications up 5.2 percent (both seasonally adjusted).

So are we housing geeks now jumping for joy? All good? Maybe not so much.

“Refinance application volume increased, but even though 30-year mortgage rates are back below 4.5 percent, the refinance index is still almost 30 percent below last year’s level. Factors such as negative equity and a weak job market continue to constrain borrowers,” notes the MBA’s VP of research and economics, Michael Fratantoni. “Purchase activity increased off of a low base, returning to levels of one month ago, but remains weak by historical standards.”

So even ridiculously low rates are not exactly boosting the housing recovery; that’s because rates have been historically low for a while.

“The problem is not the price of credit,” says economist Paul Dales at Capital Economics. “The key issue is that the high unemployment rate, tight credit criteria and high share of homeowners underwater on their mortgage are all keeping a lid on demand regardless of the price of credit. With the economy now weakening once again, these constraints are not going to go away soon.”

This is why Dales sees home prices weakening further, and we see that in data today from CoreLogic. Home prices were down 6.8 percent in June year over year, if you include distressed sales (foreclosures and short sales). That is a slightly deeper fall than May’s annual number. Without distressed sales, home prices were down 1.1 percent in June annually. That’s a bit better than the 2.1 percent annual drop in May. Of course you have to remember that distressed sales make up more than a third of the housing market right now, and far higher percentages in certain local markets.

From the Philly Inquirer:

Area’s home prices increase slightly

Prices for single-family homes in the Philadelphia region rose 0.7 percent in the second quarter, the first increase since 2008 that was not the result of government intervention in the real estate market.

An analysis of data for Prudential Fox & Roach by economist Kevin Gillen, vice president at Econsult Corp. of Philadelphia, showed second-quarter prices rose 0.9 percent in the suburbs and 0.2 percent in the city from first-quarter levels.

Gillen’s suburban data cover Bucks, Montgomery, Chester, Delaware, Camden, Gloucester, and Burlington Counties, as well as Salem and Mercer Counties in New Jersey and New Castle County, Del. – the locales in which Prudential Fox & Roach sells real estate. The data do not include condo sales.

The modest increase came after three consecutive quarters of declines totaling an average of 11 percent since the April 2010 expiration of the home-buyer tax credit. What adds to the significance of the second-quarter rise is that it occurred without any assistance from the government.

Not every county saw prices go up: Delaware and Salem Counties fell 1.3 percent and 4.1 percent, respectively; Bucks and New Castle were flat. Of the counties in which prices rose, Camden County was up 0.6 percent; Chester, 1.5 percent; Burlington, 1.6 percent; Gloucester, 2.4 percent; Montgomery, 2.5 percent; and Mercer, 6.1 percent.

“With these most recent price changes, the region’s house values have fallen by a cumulative average of 19 percent” since the market downturn began in third quarter of 2007, Gillen said.

Single-family-home sales – there were 13,558 in the second quarter – are running 18 percent below normal, he said, and the average time to sell a house in the region was 100 days, down from 120 in the first quarter.

…

What he finds notable is that city home values (excluding condos) have held up better than those in the suburbs. From their peak in 2007, city single-family-home prices have fallen 16 percent; suburban prices dropped 20 percent in the same period.In the 1990-94 economic downturn, prices in Philadelphia fell 17 percent, while the suburbs dropped just 2 percent. City values have held up much better, even though the current downturn is more severe, Gillen said.

…

Outer-ring suburbs have seen home values drop more than closer-in suburbs. In the city, outer neighborhoods lost more value than Center City and adjacent neighborhoods.In the 1990-94 downturn, the average home in Center City depreciated 41 percent. Today, value has dropped an average of 13 percent.

“That’s enough to actually negate the underperformance of Philadelphia homes during the 1980-2000 period,” Gillen said.

“If you were standing in 1980, and had a choice between buying a random home in Philly and a random home in the suburbs, and then were to hold that home until today, the Philadelphia home would actually outperform the suburban home in terms of total appreciation.

“If you predicted that to anyone in 1980 they would have had you committed!”

From HousingWire:

77% of refinancing homeowners reduce or maintain mortgage amount

Freddie Mac says 77% of homeowners who refinanced first-lien mortgages in the second quarter either reduced principal loan amounts or maintained the same loan value while benefiting from historically low interest rates.

Of those who refinanced, 51% ended up with the same loan amount, while 26% lowered their principal balance in 2Q, according to second-quarter refinance analysis from Freddie Mac.

Meanwhile, the median interest rate reduction for a 30-year, fixed-rate mortgage was about one percentage point, or an interest rate savings of 18%. Those same borrowers will save about $1,550 in interest payments on a $200,000 loan during the first year of the refinanced loan’s life, Freddie said.

“Savvy homeowners are taking advantage of some of the lowest fixed-rates in more than 50 years to lock in interest savings,” said Frank Nothaft, Freddie’s vice president and chief economist.

“Over the first half of 2011, fixed-rate mortgage rates hit a low during June, with the 30-year product averaging 4.50 percent and 15-year averaging 3.68 percent over the last four weeks of June,” Freddie said in its Primary Mortgage Market Survey.

From HousingWire:

Homeownership drops to 1998 level

The U.S. homeownership rate in the second quarter dropped to its lowest level in 13 years, according to the Census Bureau, with analysts expecting even more drops ahead.

The homeownership rate fell to 65.9%, down one percentage point from a year ago. It’s the lowest level measured since the first quarter of 1998. Analysts at Capital Economics said this means the homeownership rate built during the housing boom has been “completely wiped out” by its bust.

“The poor economic climate, the double dip in house prices, the high number of foreclosures and tight credit conditions are all reasons why the homeownership rate will continue to fall,” analysts said.

The rate remained highest in the Midwest at 70%, followed by 68.2% in the South, 63% in the Northeast and 60.3% in the West. Since the second quarter of 2007, the homeownership rate in the West has dropped more than four full percentage points.

Homeownership for younger consumers has become even more sparse. According to the Census Bureau, the rate among Americans younger than 35 years old dropped to 37.5% from 39% one year ago. This, analysts said, is a sign credit has tightened for younger consumers. With unemployment elevated for this cohort, as well, the rate could continue to fall in coming quarters.

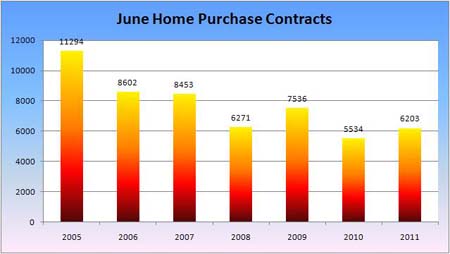

From the Otteau Group:

MarketNews – July 2011 Edition

Further evidence of stabilization in the housing market occurred in June as combined purchase contracts for resales and new construction increased by 12% from one year ago. This follows a 13% increase in May, reversing a trend of declining purchase activity over the preceding year. The market’s June performance essentially matched 2008 when the recession was still in its early stages. These recent improvements in the face of weak employment growth, high unemployment and restricted access to credit suggest that housing demand is stabilizing.

From Bloomberg:

Pending Sales of Previously Owned Homes in the U.S. Increased 2.4% in June

The number of contracts to purchase previously owned U.S. homes unexpectedly rose in June as buyers tried to take advantage of lower prices and borrowing costs.

The 2.4 percent rise in the index of pending home resales followed an 8.2 percent May gain, the National Association of Realtors said today in Washington. Economists forecast a 2 percent drop, according to the median estimate in a Bloomberg News survey.

…

Estimates for pending home sales ranged from a drop of 5 percent to an increase of 8 percent, according to 39 forecasts in the Bloomberg survey. Pending sales rose 17 percent from June 2010.

From the WSJ:

Behind the Numbers: Pending Home Sales Rise

This week’s reports on the housing market have been decidedly mixed.

On Tuesday, the government said new home sales were down 1% on a monthly basis in June. Also that day, the S&P/Case-Shiller index of home prices in 20 major U.S. cities was down 4.5% in May from a year earlier.

But today’s news was positive and unexpected: The National Association of Realtors’ seasonally adjusted index for pending sales of existing homes rose 2.4% on a monthly basis to a reading of 90.9 in June. Economists had forecast a 2% drop.

…

Peter Newland, economist, Barclays Capital: “The gains in May and June largely offset the sharp 11.2% decline in April, which likely owed in part to adverse weather conditions in much of the country. Indeed, the level of the index, at 90.9 in June, is back broadly in line with the (first-quarter) average….This is an encouraging report with regard to the outlook for existing home sales, which tend to lag pending sales by a month or two.”

…

Ian Shepherdson, chief U.S. economist, High Frequency Economics: “The underlying trend in existing home sales is more or less flat, and it is hard to imagine any near-term change as long as applications for mortgages to finance house purchase(s) are flat, too. In this context, the gains in pending home sales in May and June are probably best considered as nothing more than a rebound after the very late Easter and severe weather depressed the index in April.”

From the NAR:

Pending Home Sales Rise in June

Pending home sales increased in June following a wide swing down in April and then up in May, according to the National Association of Realtors®. Activity increased in the West and South but declined in the Midwest and Northeast; all regions show strong double-digit gains from a year ago.

The Pending Home Sales Index,* a forward-looking indicator based on contract signings, rose 2.4 percent to 90.9 in June from 88.8 in May and is 19.8 percent above the 75.9 reading in June 2010, which was the low point immediately following expiration of the home buyer tax credit. The data reflects contracts but not closings.

…

The PHSI in the Northeast slipped 0.4 percent to 68.9 in June but is 19.4 percent higher than June 2010. In the Midwest the index fell 3.7 percent to 79.7 in June but is 26.4 percent above a year ago. Pending home sales in the South increased 4.4 percent to an index of 99.2 and are 19.1 percent higher than June 2010. In the West the index rose 6.4 percent to 107.0 in June and is 16.4 percent above a year ago.

From the Fed:

July Beige Book – Second District–New York

Construction and Real Estate

Residential construction has remained depressed and housing markets across the District have remained sluggish since the last report, although there has been further improvement in the rental market. An authority on New Jersey’s housing industry reports that the resale market has remained weak, and that the level of optimism appears to have waned. Prices of existing homes have continued to drift down, largely reflecting a preponderance of “distressed” sales; otherwise, prices across northern New Jersey are generally flat. While the inventory of unsold new homes is fairly lean now, the inventory of available existing homes remains elevated–as high as 16 months of sales if units in foreclosure and other distressed properties are included. Buffalo-area Realtors also report some weakening in market conditions in May and June; while foot traffic has been fairly brisk, few people have made offers. More generally, sales activity across New York State has been steady to weaker. A major New York City appraisal firm reports that both sales and prices of co-ops, condos, and single-family homes remain flat overall–both in Manhattan and in the outer boroughs–with the high end of the market accounting for a larger share of sales than last year.

In contrast with the weakness in home purchase markets, rental markets have shown increasing strength. Manhattan’s apartment rental market has strengthened since the last report. Rents on new leases were reported to be up 6 percent in June from a year earlier in June. In addition, one contact notes that landlords have pulled back on concessions, which are now reportedly being offered on fewer than 5 percent of new leases, down from 60 percent in mid-2010. Separately, the Jersey shore summer rental market is reported to be fairly strong this year, though the sales market for rental units remains sluggish. More broadly, many New Jersey landlords are reported to be pushing through rent increases for the first time since the recession.

Commercial real estate markets have been steady to somewhat weaker since the last report. Office vacancy rates and rents were generally stable across the District during the second quarter: market conditions improved slightly in the Buffalo and Rochester metro areas and in Manhattan, but they weakened moderately in northern New Jersey and metropolitan Albany. However, industrial real estate markets weakened modestly across most of the District, with vacancy rates edging up and rents drifting down.

From HousingWire:

CoreLogic: Nondistressed home prices stabilizing

Stabilizing nondistressed home prices, a declining shadow inventory and stronger foreclosure auctions should lead to lower distressed sales and less downward pressure on prices, according to CoreLogic.

The report notes that while mortgage performance is improving, it is not improving nearly as much as other consumer debt performance.

Despite, a bit of positive news in the report, CoreLogic notes that negative equity will remain a strong influence on the market for an extended period of time.

In May 2011, the “excluding distressed sales” home price index only dropped 0.4% from a year ago, compared to a decline of 7.4% for the all transactions HPI.

“Another very positive sign is that even while including distressed sales, the HPI increased between March and April — the first time in more than six months — and was up again between April and May. These increases represent the resumption of seasonality in home prices and are a positive sign for the market.”

…

Price discounts on distressed sales remain high, however, a major impediment to price stabilization, but the good news is that new auction filings have been down significantly since October 2010.Residential shadow inventory — the estimated number of pending supply of distressed properties — declined to 1.7 million units in April 2011, down from 1.9 million units a year ago and down nearly 20% from its peak.

“Given that the recent declines in auction filings and current shadow inventory levels are the drivers of future distressed sales, the level of distressed sales should, all things equal, begin to decline late in 2011 and into 2012,” the report said.

…

“Going forward, negative equity will primarily decline by a combination of foreclosures, amortization and, to a lesser extent, price increases,” the report said. “While price declines have been a large driver of negative equity, price improvements will most likely not be the antidote anytime soon. …”While the worst is over, it means many of these borrowers will be upside down for an extended period of time, which will result in a long tail of mortgage distress.”

From Forbes:

Ahead of the Bell: New home sales

More people likely purchased new homes in June than the previous month, although sales are expected to remain below healthy levels.

Economists forecast that new-home sales rose to a seasonally adjusted annual rate of 323,000 in June, according to a survey by FactSet. The Commerce Department will release the report at 10 a.m. Tuesday.

In May, sales fell 2.1 percent to an annual rate of 319,000. That’s less than half the 700,000 homes per year that economists say is typical in healthy markets.

In a separate report Tuesday, Standard & Poor’s/Case-Shiller will release its home-price index for May. The index measures home prices in 20 of the largest U.S. metro areas. It sank in March to its lowest levels since 2002. It rebounded slightly in April because of a traditional influx of spring buying.

Housing remains the weakest part of the U.S. economy. Sales of new homes have fallen 18 percent in the two years since the recession ended. Last year was the worst for new-home sales on records dating back a half century.

High unemployment, larger down payment requirements and tougher lending standards are preventing many people from buying homes. And some potential buyers who can clear those hurdles are holding off, worried that home prices have yet to bottom out.

From HousingWire:

Fannie Mae sees light at the end of housing tunnel

Home sales in the second quarter of 2011 were bad, according to Fannie Mae. Home prices also remain volatile, moving with gains and losses, over the past two years.

However, according to a housing forecast report card released on Friday from the government-sponsored enterprise, 2012 is likely to be a different story.

Next year will likely see meaningful gains in both categories, especially in the multifamily space. Both home sales and house prices should begin to improve from the third quarter 2011, with faster growth in the final two quarters of 2012.

…

“Clearly, the renewed slowdown in hiring underscores the uncertainty surrounding the economic outlook,” said Fannie Mae Chief Economist Doug Duncan. “The lack of sustained, robust job growth continues to push out into the future the time for the housing market to heal, which is crucial to a meaningful economic expansion.”Fannie Mae also predicts mortgage rates on 30-year fixed to hit 5% in the second quarter of 2012 and keep rising from there. Liquidations, on the other hand will remain at low levels for the long term.

Demands for rentals should remain robust, according to Kim Betancourt, Fannie Mae director of multifamily economics and market research, in a separate research report.

“There is some concern that multifamily fundamentals may stagnate if job growth remains anemic, however, new rental supply will be limited, likely resulting in keeping current rent levels stable,” Betancourt wrote.

Some updates on my reno.

Foundation and drainage work is done, grading is complete. We no longer have any grass at all. Retaining walls are up and looking great.

From the Star Ledger:

N.J. unemployment rate grows in June

New Jersey added 1,700 jobs in June, but the unemployment rate inched up one-tenth to 9.5 percent as more people reported looking for work.

The Labor Department reports that the state added 6,400 private-sector jobs last month but public sector jobs declined by 4,700.

The state says leisure and hospitality industries added 5,200 jobs; education and health services added 1,800 jobs; and 1,000 construction jobs were added.

The manufacturing sector was hardest hit with a loss of 1,900 jobs; financial activities lost 900 jobs; and trade transportation and utilities lost 400 jobs.

From the APP:

NJ gained 1,700 jobs in June; unemployment climbs to 9.5%

New Jersey’s economy added 1,700 jobs in June, the state said Thursday in a report that shows the labor market recovering slowly but steadily from the devastating recession.

The job growth wasn’t strong enough to keep up with the number of residents looking for work; the state’s unemployment rate rose to 9.5 percent from 9.4 percent in May.

“Right now, my daughter, son-in-law and grandson moved into my one-bedroom apartment,” said Veronica Gaddis, 50, of Lake Como, who herself has been out of work for two years. “I’m grateful for that because I know there are people who have nowhere to go. It’s a mess.”

…

New Jersey is trying to dig itself out of the hole left by a recession that caused it to lose 265,000 jobs, or 6.5 percent of its employment. And without a strong manufacturing presence, it hasn’t taken been able to take advantage of a resurgence in the nation’s manufacturing sector.The report in June, however, carried a hopeful sign. The state added 6,400 private-sector jobs last month. It added 28,100 private-sector jobs the first half of the year, preliminary estimates show. And that puts it on pace for its best performance since 2000, Rutgers economist James W. Hughes said.

“It’s destined to be the best job growth year in 11 years,” Hughes said.

Still, New Jersey at that pace wouldn’t recover its lost jobs until 2016. And there are obstacles to get there. For one, there remains a gap between the pre-recession skills that workers developed and the post-recession skills employers need, said Mark Vitner, an economist with Wells Fargo Securities.