From Portfolio:

Housing Sales Improving? Humbug

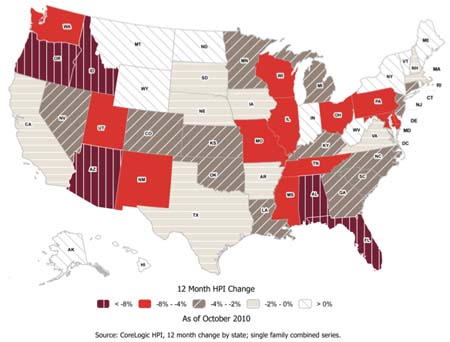

The housing market just keeps dragging down the economy, with small businesses likely to be among the hardest hit if the sector does not rebound.

This morning, the National Association of Realtors reported that sales of existing homes rose 5.6 percent in November from October. Good news, right? Well, not really. If you compare those figures to November 2009, when there was a tax credit in place for first-time homebuyers as part of the stimulus package, sales were down 27.9 percent.

And the 4.68 million homes sold amounted to fewer than the 4.75 million home sales that economists had forecast.

While National Association of Realtors Chief Economist Lawrence Yun saw the glass as half-full, others aren’t so sure.

…

Mark Vitner, an economist with Wells Fargo, gave his blunt reaction to Bloomberg: “Housing is going to remain dead in the water through the middle of 2011. As foreclosures come back on the market, that will put downward pressure on prices.”

From the NY Times:

U.S. Home Sales Rose in November but Missed Forecasts

Sales of existing homes climbed in November, but sustained growth in the job market and access to credit were needed before home purchases reach a level that signals a recovery, analysts said on Wednesday.

In the latest report to reflect an improving economy, the National Association of Realtors said on Wednesday that sales of homes rose 5.6 percent to a seasonally adjusted annual rate of 4.68 million in November, from about 4.43 million homes in October.

Still. the rate was nearly 28 percent below the 6.49 million of November 2009, and it fell below the pace of 4.75 million units that economists surveyed by Bloomberg had expected.

“We are underperforming, given the size of the population,” Walter Molony, a spokesman for the Realtors association, said. “Homes sales this year are sub-par. We should be over 5 million on a sustainable level.”

The November figure, a sharp reversal of the 26 percent plunge in existing home sales in October, refers to completed transactions for single-family townhomes, condominiums and co-ops.

From Bloomberg:

Sales of U.S. Existing Homes Rise Less Than Forecast to 4.68 Million Rate

Sales of existing homes rose less than forecast in November as the industry that triggered the worst U.S. recession in seven decades struggled to recover after a government tax credit lapsed.

Purchases increased 5.6 percent from the prior month to a 4.68 million annual rate, the National Association of Realtors said in Washington. Economists projected sales would rise to a 4.75 million pace, according to the median forecast in a Bloomberg News survey. The median price rose 0.4 percent from a year earlier.

Previous decreases in prices and mortgage rates have made houses more affordable, which may keep supporting demand after the end of a government tax credit caused the industry to slump. At the same time, unemployment hovering near 10 percent is a reminder it will take years for housing to regain pre-recession levels.

…

Distressed sales, which include foreclosures and short- sales in which the bank allows a home to sell for less than the full amount of the mortgage, accounted for 33 percent of total sales, about the same as in prior months.