From the Federal Reserve:

December Beige Book (Summary of current economic conditions) – Second District–New York

Construction and Real Estate

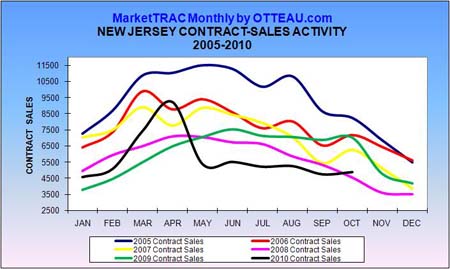

Housing markets across the District have been steady to softer since the last report, with some of the ongoing weakness at the lower end of the market attributed to the mid-year expiration of the home-buyer tax credit. In general, prices have drifted down across much of upstate New York and in northern New Jersey since mid-year, while prices in New York City remained relatively steady. Buffalo-area Realtors report that the housing market weakened somewhat in October through early November, particularly for lower-priced homes; sales activity has slowed, and the supply of homes on the market has increased. Similarly, a contact in northern New Jersey reports that market conditions remain sluggish: sales activity remains low and is still largely composed of distress sales, and prices are still said to be edging down.

Activity in New York City’s co-op and condo market has slipped by a bit more than the seasonal norm in October and early November, particularly at the lower end of the market, though a recent flurry of activity is reported at the very high end (homes in the range of $8 million or more). Prices remain stable across the spectrum. While the number of new condos under construction has declined modestly, there continues to be a substantial inventory of unsold, completed units. Manhattan’s rental market has reportedly softened a bit since the last report. Rents remain stable, but landlords are, once again, offering concessions (such as one or more month’s free rent), though these discounts are not as steep as in 2009. A substantial amount of new housing in the pipeline is likely to be offered as rentals.

Office markets across the District have been steady to slightly softer thus far in the fourth quarter. Asking rents held steady in Manhattan and slipped in northern New Jersey, Long Island and Rochester but rose modestly in Westchester and Fairfield counties and in Buffalo. Vacancy rates have been steady to modestly higher since the last report. Sales of commercial properties remain sluggish, and a contact in upstate New York reports that commercial construction activity remains at depressed levels.