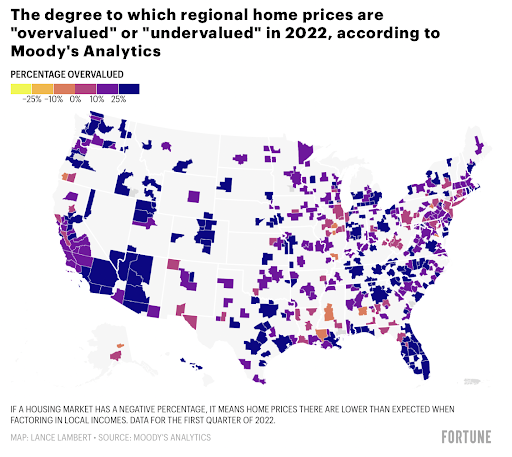

From Fortune:

183 housing markets could soon see home prices fall by 20%.

From Fortune:

From the Star Ledger:

The owners of Westfield Garden State Plaza are poised to make every shopaholic’s dream come true — you can literally live at the mall.

A plan, hatched pre-COVID, to redevelop New Jersey’s second largest mall into a lifestyle center, with apartments, took a step forward this week when Westfield Garden State Plaza mall owner, Unibail-Rodamco-Westfield, announced that it has partnered with Mill Creek Residential for the first phase of its redevelopment.

Ground will be broken in 2024 on 550 luxury apartments and they are expected to be completed in 2026, the two firms announced. “Plans are not definitive” about how many bedrooms they will have and how big they will be, said Geoff Mason, executive vice president, U.S. development, design & operating management for Unibail-Rodamco-Westfield.

From MarketWatch:

The housing market isn’t crashing, but it’s definitely feeling the burn.

After two frenzied years, home buying is cooling off as mortgage rates rise. Some experts in the field are calling it a “housing recession.”

U.S. home values fell in July by 0.1%, compared to the month before, a new Zillow report said.

While deceleration in home-price growth is typical for this time of the year, Zillow noted, the small decline is the first monthly dip since 2012.

The typical U.S. home value fell by $366 in July, and is now $357,107, as measured by the Zillow Home Value Index.

Given the dip in July, Zillow revised its forecast for the growth in home values to 2.4% through the end of July 2023. The current rate of growth is 16%.

But this hardly counts as a crash in prices, because the typical home value is also up 44.5% from July 2019 before the COVID-19 pandemic.

At this point, sellers are finding themselves with fewer offers, and are having to offer more concessions themselves to entice buyers.

From Bloomberg:

The US mortgage industry is seeing its first lenders go out of business after a sudden spike in lending rates, and the wave of failures that’s coming could be the worst since the housing bubble burst about 15 years ago.

There’s no systemic meltdown coming this time around, because there hasn’t been the same level of lending excesses and because many of the biggest banks pulled back from mortgages after the financial crisis. But market watchers nonetheless expect a string of bankruptcies broad enough to trigger a spike in layoffs in an industry that employs hundreds of thousands of workers, and potentially an increase in some lending rates. More of the business is now controlled by independent lenders, and with mortgage volumes plunging this year, many are struggling to stay afloat.

“The nonbanks are poorly capitalized,” said Nancy Wallace, chair of the real estate group at Berkeley Haas, the business school at University of California, Berkeley. “When the mortgage market tanks they are in trouble.”

In 2004, only about a third of the top 20 lenders for refinancings were independent firms. Last year, two-thirds of the top 20 were non-bank lenders, according to LendingPatterns.com, which analyzes the industry for mortgage lenders. Since 2016, banks have seen their share of the market shrink to about a third from about half, according to news and data provider Inside Mortgage Finance.

Many of the so-called shadow lenders will emerge from this slowdown relatively unscathed. But some lenders have already stopped operating or scaled down dramatically, including and Sprout Mortgage and First Guaranty Mortgage Corp. Both specialized in riskier lending that isn’t eligible for government backing.

First Guaranty, a company that according to court papers is majority owned by fixed-income giant Pacific Investment Management Co., filed for bankruptcy, saying it failed after it made loans earlier this year that dropped in value. It was holding onto those loans until it had enough to bundle into bonds and sell to investors, and it had been temporarily funding them with a line of credit.

Once interest rates started to climb, lending volume shrank across the industry, according to court papers. That meant the company could no longer find enough new loans to bundle, or get enough financing to keep operating, said First Guaranty’s chief executive officer, Aaron Samples. Firms included Flagstar Bank and Customers Bank are owed about $418 million, according to court documents.

First Guaranty employed 600 people before it filed bankruptcy in June and made $10.6 billion in loans last year, according to court records. Days before seeking court protection, the company fired 471 workers because it couldn’t get enough financing to overcome a cash crunch.

From CNBC:

Sales of previously owned homes fell nearly 6% in July compared with June, according to a monthly report from the National Association of Realtors.

The sales count declined to a seasonally adjusted annualized rate of 4.81 million units, the group added. It is the slowest sales pace since November 2015, with the exception of a brief plunge at the beginning of the Covid pandemic.

Sales dropped about 20% from the same month a year ago.

“In terms of economic impact we are surely in a housing recession because builders are not building,” said Lawrence Yun, chief economist for the Realtors. “However, are homeowners in a recession? Absolutely not. Homeowners are still very comfortable financially.”

The July sales figures are based on closings, so the contracts were likely signed in May and June. Mortgage rates spiked higher in June, with the average rate on the 30-year fixed loan crossing 6%, according to Mortgage News Daily. It then settled back into the high 5% range. That rate started this year around 3%, so the hit to affordability in June was hard, especially coupled with soaring inflation.

Homebuyers are also still contending with tight supply. There were 1.31 million homes for sale at the end of July, unchanged from July 2021. At the current sales pace, that represents a 3.3-month supply.

While demand is falling off due to weaker affordability, prices remain stubbornly high. The median price of a home sold in July was $403,800, an increase of 10.8% year over year. Price gains are now moderating, though, as this is the smallest annual rise since July 2020.

“The median home sales price continued to climb, but at a slower pace for the fifth consecutive month, shining a light on how downshifting buyer demand is moving the housing market back toward a more normal pace of activity,” said Danielle Hale, chief economist at Realtor.com. “A look at active inventory trends shows that home listings were nearly twice as likely to have had a price cut in July 2022 compared to one year ago.”

From Insider:

The odds of a severe housing downturn have risen, and US home prices could sink as much as 15% in that scenario, according to a report from Fitch.

But the credit rating agency said a moderate slowdown is still the more likely outcome, predicting that housing activity will fall by mid-single digits in 2023 and low-single digits in 2024.

Fitch reaffirmed a stable outlook for US homebuilders, but estimated that a sharp deterioration in the market could result in housing activity falling 30% or more over multiple years with home prices down 10% to 15%.

Fitch listed consumer confidence, GDP growth, home prices and unemployment as key factors contributing to its projections.

From Jalopnik:

There could be bad news around the corner as more and more car buyers are having difficulty keeping up with auto loan payments.

According to a report from Automotive News, 1.63 percent of auto loans haven’t received a payment in at least 60 days. That number is 0.4 percent higher than it was the same time last year, and the highest in the past four years.

That being said, car loan default rates are still below pre-pandemic levels. Satyan Merchant, the Senior Vice President of TransUnion told the outlet that the increase can be attributed to changes in origination — or where borrowers stand in credit and spending.

Borrowers who took out auto loans in the second and third quarters of 2020 are keeping up with them better than pre-pandemic borrowers, according to TransUnion. But auto loans in the second and third quarters of 2021 are starting to show similar delinquency rates as debt from before COVID-19.

“There is slight worsening performance of recent vintages at a risk tier level when we isolate near-prime and above cohorts, and we suspect pandemic score migration may be playing a role,” Merchant said in a statement.

He gave the example of a subprime customer whose credit improved in 2020 and was near prime for a 2021 car loan but who now behaves more like a subprime consumer.

…

So, what does this tell us? Well, from the looks of it, more and more people are falling a month or two behind on their auto loans, but they are not letting the delinquencies lead to defaults. That’s a good thing. As for if this behavior issustainable? That’s sort of anyone’s guess.

Remember 2008, when everyone was unable to pay their mortgage? Feels familiar to me.

We’ll see what 2023 holds.

From CoStar:

The future of the former Toys R Us corporate headquarters is still to be determined in New Jersey, a state that’s been ground zero nationally for the redevelopment of such large, isolated and what some call outdated suburban workplace campuses. But when its fate is decided, the outcome could help write the next chapter for America’s office parks.

For years, before its bankruptcy and liquidation in 2018, retailer Toys R Us occupied a 193-acre property in Wayne, a bucolic site on the waterfront of a reservoir. The campus was anchored by two connected office buildings totaling about 621,000 square feet at 1 Geoffrey Way. The property was sold in 2019 for $19 million and now sits mostly vacant.

A consulting firm, BRS of Medford Lakes, New Jersey, presented a market study on Thursday it did on the area where the campus is located, detailing its demographics and vacancy rates for different property categories. After months conducting that research and receiving input from residents, BRS said it will release its final report with recommendations for the best ways to repurpose the Toys R Us buildings, transitioning them to mixed use, by the end of the month. Those possible options include research and development space, shops, restaurants, and a performance hall.

“Based on our surveys … a lot of people have said that in addition to use for recreation bringing them to the site, there was a lot of interest in entertainment activities and dining and children’s activities, as well as festivals and shopping,” Alisa Goren, a BRS planner, said during the presentation. “So it looks like a lot of things that would bring you to the site are also things that would be appropriate and attractive to the market as a whole.”

The process playing out in New Jersey is part of a commercial real estate discussion taking part across the country. The national challenge of finding ways to repurpose and revitalize office properties isn’t going to go away, as even more companies rethink their workplace needs because of the pandemic and the work-from-home trend it accelerated. That’s led to some firms downsizing their footprints.

The former home of Toys R Us isn’t the first large corporate campus to be reimagined in the Garden State. New Jersey has seen more than its fair share of the redevelopment of former one-tenant suburban office complexes, dubbed “stranded assets,” some of which had been vacant for years. That’s because during roughly the past decade a number of companies exited their headquarters in the Garden State in the wake of mergers and acquisitions, belt-tightening, an effort to escape New Jersey’s high taxes, or in strategic moves. The repurposing of some of those sites is complete, offering a model for developers in other parts of the nation.

From the Washington Post:

With interest rates now hovering around 5%, existing-home sales are down more than 14% from last year. Some potential buyers are sitting on the sidelines until rates or prices or both decline, while sellers are hoping the market picks up again so they can get a higher price.

But don’t count on rates falling to those pandemic lows. They were the result of extraordinary market manipulation from the Fed. And unless this becomes a regular feature of monetary policy, rates are not going back to what they used to be.

The real estate market has been on a wild ride. House prices, measured by the Case-Schiller index, increased 30% between March 2020 and December 2021, a steeper rise than the lead-up to end the housing bubble in 2008. This was in part because many people moved during the pandemic, but also because the 30-year mortgage rate was only 2.65% in spring of 2021.

The impact of the Fed’s interference may be felt for years. In the spring of 2020, the Fed was desperate to avoid economic collapse, so it reverted to its 2008 playbook. It cut rates to zero and brought back quantitative easing, buying long-dated government bonds and mortgage-backed securities (MBS). Most residential mortgages are securitized by Fannie Mae or Freddie Mac, and resold in what is known as an agency MBS.

In 2020, the mortgage-backed security market was in trouble, and the Fed was even more aggressive than it was in 2008. It effectively became the only ultimate buyer of these securities: Its holdings of agency MBS increased by $1.3 trillion between 2020 and 2022, while the market for agency mortgage-backed securities grew by $1.5 trillion. The Federal Reserve now holds more than 40% of the total outstanding amount of agency MBS, or nearly half the market.

These actions were one big reason rates fell so low. Your mortgage rate is based on the 10-year bond rate, plus a premium for the extra risk involved. The size of that risk premium is largely determined in the MBS market, based on the liquidity and rate risk the investor takes on. The figure below shows the Bloomberg US MBS index minus the yield on 10-year bonds.

From NJ Globe:

Stepping up his fight against New York City’s congestion pricing plan, Rep. Josh Gottheimer (D-Wyckoff) and three Bergen County legislators today announced a new proposal that would incentivize New Jersey commuters to stay on their side of the Hudson.

Legislation offered by State Sen. Joseph Lagana (D-Paramus), Assembly Appropriations Committee Chair Lisa Swain (D-Fair Lawn) and Assemblyman Christopher Tully (D-Bergenfield) offers tax credits for New York-based companies to open regional offices in New Jersey, and reward businesses that help reduce commuting costs for their employees.

The New York plan, which Gottheimer called a Congestion Tax, could cost New Jerseyans who drive to New York an extra $23 per day, on top of tolls, gas and parking,

“Just read MTA spelled backwards and it tells you exactly how New York looks at New Jersey right now: as their personal ATM,” said Gottheimer. “The ‘Stay in Jersey’ bill will establish a new incentive program to provide New York businesses with tax credits for expanding business operations into New Jersey — closer to the primary residence of existing Jersey full-time employees — to help them avoid having to drive into the city and get whacked by the Congestion Tax.”

The lawmakers argue that their plan would improve work productivity, reduce commuter stress, enhance family time, protect the environment, and create New Jersey jobs.

Lagana, who represents a suburban Bergen district full of commuters, said that New York City’s bid to “add exorbitant congestion pricing fees” makes a cost-cutting plan necessary.

“It’s no secret that working close to home benefits not only residents themselves, but is a boon to local economies,” Lagana said. “Business hubs spur economic development and investment in our mom and pop shops, local eateries and markets, and boutique downtown stores.”

From the NAR:

The inventory recovery accelerated in July, as active listings increased at record-fast1 annual pace (+30.7%) for the third month in a row, according to the Realtor.com® Monthly Housing Trends Report released today. Although buyers had more for-sale home options in July, competition remained largely in sellers’ favor, with listing prices near all-time highs and homes selling more quickly than pre-COVID.

…

Between supply and demand trends, July data indicates that softening buyer interest is the bigger driver of accelerated inventory improvements. With typical monthly mortgage payments now 1.5 times higher than in July 2021, recent home sales data shows that many buyers are putting their plans on pause, which is giving active listings room to grow. However, the shift in market conditions seems to be having the opposite effect on seller activity, with new listings declining for the first time since March. This suggests that some homeowners are reconsidering their plans to list in light of trends like declining numbers of homes under contract. Despite the new seller dip, active listings grew at a record-fast pace for the third straight month in July, further signaling a real estate refresh on the horizon for 2022 buyers.

From MarketWatch:

Is this the news home buyers have finally been looking for? In June, the annual home price growth rate saw the “the greatest single-month slowdown on record since at least the early 1970s,” according to mortgage data and analytics company Black Knight. What’s more, this was coupled with the “largest single-month influx of for-sale inventory in 12 years,” the firm noted in a release about its latest Mortgage Monitor report on August 1.

The report reveals that June was the third straight month of cooling, with annual home price appreciation dropping from 19.3% in May to 17.3% in June; this is an even more pronounced drop even than in 2006. (For its part, the US CoreLogic S&P Case-Shiller Index also marked a decrease, with June “appearing to be a tipping point with a more significant pullback in buyer interest,” according to a report released at the end of July.) In fact, all 50 top metro markets saw growth slow in June with one in four major US markets seeing growth slow by 3 percentage points or more.

But why are we seeing this cool down? Holden Lewis, home and mortgage expert at NerdWallet, says mortgage rates are much higher than they were at the beginning of the year, forcing buyers to shop for homes in lower price ranges so they could afford the monthly payments. “As people buy less expensive properties, they drag down the rate of house price growth. This summer’s main lesson is the importance of setting a reasonable asking price,” says Lewis.

What’s more, Zillow economist Nicole Bachaud says the housing market is in the midst of a major transition. “Buyers have hit an affordability ceiling and demand is pulling back, causing homes to pool on the market as sales slow. Home sellers are being forced to adjust their expectations and many are opting to stay out of the market and keep their favorable interest rate,” says Bachaud.

To the delight of homebuyers and the chagrin of home sellers, Greg McBride, chief financial analyst at Bankrate, says this is not the housing market of a few months ago. “Sellers won’t get the moonshot asking price they thought, it will take longer to sell and there won’t be a bidding war. While buyers have more negotiating power now, mortgage rates remain above 5% and home prices are still lofty,” says McBride.

While headline-generating movements are to be expected during this period of transition, Bachaud says it’s important to remember just how far prices have risen not only during the pandemic, but over the past decade. “We are talking about small dips from record highs. A fall back near pre-pandemic levels is very unlikely as overall housing supply will remain a barrier and demand will still exist on the sidelines,” says Bachaud. Ultimately, she says, this a much-needed market rebalancing could help some first-time buyers catch up while homeowners will retain much of the equity they’ve built over the years.

Nearly half of mortgaged properties were considered equity-rich in the second quarter — meaning owners had at least 50% in home equity. This marked the ninth straight quarterly rise, fueled by soaring house valuations in the pandemic era and an increase in down payments by recent buyers, according to real estate data provider Attom.

Although the housing market has cooled recently, the percentage of equity-rich properties will probably keep increasing, according to Attom.

“While home price appreciation appears to be slowing down due to higher interest rates on mortgage loans, it seems likely that homeowners will continue to build on the record amount of equity they have for the rest of 2022,” Rick Sharga, executive vice president of market intelligence at Attom, said in a statement.

The gains were particularly sharp in the south, where many Americans moved during the pandemic.

In Florida, more than 60% of mortgaged homes are now equity-rich, up from about a third a year ago. It’s good news for owners and for municipalities as well, as it creates a more stable financial environment.

Nationwide the portion of mortgaged homes that were equity-rich reached a record 48.1% in last quarter, up from 44.9% in the first quarter and from 34.4% a year earlier, Attom said.

Areas with the highest share of equity-rich properties included Martha’s Vineyard and Nantucket, Massachusetts; Burlington, Vermont; and Gillespie county and Travis county near Austin, Texas.

Meanwhile, the share of homes that were considered seriously underwater — where the mortgage is 25% greater that the property’s estimated market value — dropped to a low of 2.9%.

From CNBC:

Stock futures were little changed Friday as investors waited for the July jobs report, looking for further clues about the Federal Reserve’s path of rate hikes and the state of the economy.

Futures on the Dow Jones Industrial Average were up 25 points or 0.08%. S&P 500 and Nasdaq 100 futures fell slightly.

Economists expect 258,000 jobs were added in July, down from 372,000 in June, according to Dow Jones. Unemployment is expected to hold steady at 3.6%. The jobs report will be released Friday at 8:30 a.m. ET.

“Investors will be waiting to see if the labor market can withstand the Fed’s rate-hike campaign as well as it did in June,” said Mike Loewengart, managing director of investment strategy at E-Trade.

Job growth is expected to slow as the Fed continues to hike interest rates to tame surging inflation, but it’s unclear whether that slowing will tip the economy into an official recession. Many said Friday’s report is crucial as it’s one of two the central bank will see before it decides how much to raise rates at its September meeting.

From the NYT:

The competition for parking space is getting steeper. Commutes are inching longer. Workplace lounges are filling up with commotion as junior associates play cornhole. What return-to-office debate? In some parts of the country, it’s been settled.

“I know almost nobody in Columbus who is fully remote,” said Grant Blosser, 35, who works at a financial services firm.

In October 2020, Mr. Blosser started going back into his office in Columbus, Ohio, five days a week. He cracked jokes with the young analysts, one of whom recently dragged his team to hot yoga. (It “kicked our butts.”) He listened to his book club’s selection in the car (currently, a biography of Winston Churchill). It was a relief, he said, to feel the “separation of church and state” that came from leaving the house each day.

“Almost everybody I know is in an office most of the time here,” he said. “The headlines that I read about as far as people dragging their feet going back to the office are about select companies and select cities.”

More than two years into the pandemic, American corporate workplaces have splintered. Some are nearly as full as they were before Covid-19 struck; others sit abandoned, printers switched off and Keurig cups collecting dust. Workers in America’s midsize and small cities have returned to the office in far greater numbers than those in the biggest U.S. cities. Some executives in large cities are hoping they’ll catch up, though they’ve been impeded by safety and health concerns about mass transit commutes, as well as competitive job markets where employees are more likely to call the shots.

In small cities — those with populations under 300,000 — the share of paid, full days worked from home dropped to 27 percent this spring from around 42 percent in October 2020. In the 10 largest U.S. cities, days worked from home shifted to roughly 38 percent from 50 percent in that same period, according to a team of researchers at Stanford and other institutions led by the economists Steven Davis, Nick Bloom and Jose Maria Barrero.