From the NY Post:

US office real estate prices headed for ‘severe crash,’ investors say

The commercial real estate market is headed for a severe collapse due in large part to sky-high interest rates and declining property values, according to a survey of investors.

Around two-thirds of those who responded to a Bloomberg News survey said they believe that the commercial real estate market will recover only after a crash.

When asked when they believe the price of office properties will hit bottom, 44% said they expect that to happen in the second half of next year while 22% said it will be in the first six months of 2024, according to Bloomberg News.

Just 6% of the 919 respondents said that prices would bottom out this year while 29% predicted that it would happen in 2025 or beyond.

The Fed has raised interest rates aggressively, which is increasing the cost of financing commercial properties at a time when there is also reduced need for them, which has hit rent levels.

Investors are bracing for a possible crisis triggered by default on $1.5 trillion in debt that is coming due by the end of 2025,.

Some $270 billion in commercial real estate loans held by banks are set to mature in 2023, according to Trepp.

Over the next four years, commercial real estate properties must pay off debt maturities that will peak at $550 billion in 2027, according to analysts at Morgan Stanley.

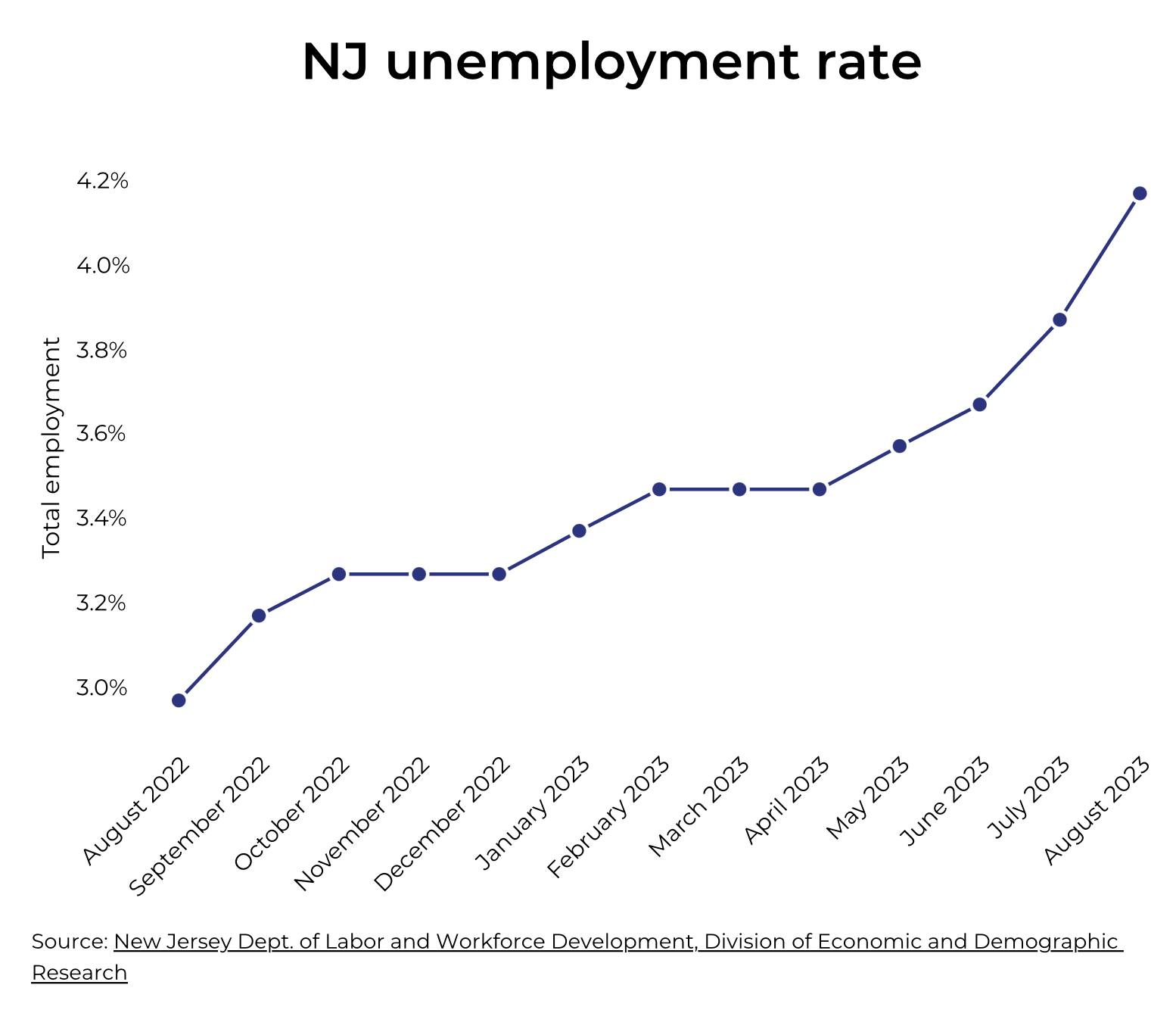

Earlier this month, a study released by economists from NYU Stern Business School, Columbia Business School and the National Bureau of Economic Research showed that vacancy rates are at 30-year highs in many American cities.

In New York City, the vacancy rate was 22.2% in Q1 of 2023.