From the Washington Post:

I’m in the process of building a house, so I recently met with the head of a real estate brokerage to discuss selling my current home in about a year. Knowing that I worked in finance, he asked me my views on the housing market because he said he was seeing lot of doom and gloom on the internet.

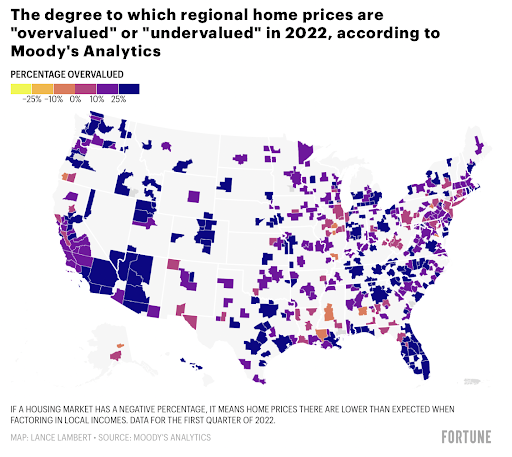

First, all real estate is local. The housing market where I live in coastal South Carolina is still strong. Although transactions are down from a year ago, that’s because there are very few houses on the market. A lot of people – many of them cash flush and not impacted by rising interest rates — are moving here from other parts of the country, and I wouldn’t have any trouble selling my house today if I wanted. He agreed.

He also agreed when I told him that you can’t randomly scroll on Twitter these days without running into predictions of an impending housing collapse. Jeff Weniger, the head of equities at WisdomTree investments, recently posted a thread on Twitter labeled “Housing is in trouble” that went a bit viral. The thread was well-researched with charts and data to back up each of his points, such as how the supply of new homes has skyrocketed, as have monthly principal and interest payments on mortgages. Correspondingly, the National Association of Home Builders’ Housing Market Index has tanked. New and existing home sales have dropped precipitously, and affordability has tumbled to 2005 levels.

Some people take these facts and extrapolate them into a thesis, which is that a housing crisis is coming that will be equal to or greater than the one that we experienced in 2008. In fact, judging from what I read online, this seems to be the prevailing view. I suppose some of this is understandable. The Federal Reserve is raising interest rates like never before, and I suppose that in some nightmare scenario higher borrowing costs will choke off demand for credit. But I doubt it will get that far, given how important the housing market is to the economy, accounting for anywhere between 15% and 20% of gross domestic product.

There are two main reasons why we are not going to experience another crisis in residential real estate. The first is that housing is financed much differently than in the years leading up to the subprime mortgage collapse and resultant financial crisis. You had no money down mortgages, “liar” loans, NINJA loans, interest only mortgages, negative amortization mortgages and numerous financial innovations on top of those – all of which were facilitated by poor underwriting standards. Then, those mortgages were packaged together into bonds given top AAA credit ratings. Those bonds were then packaged into high-risk securities called collateralized debt obligations that were also assigned the highest credit ratings. Finally, Wall Street created many hundreds and hundreds of billions of dollars of risky credit-default swap contracts tied to all those bonds and CDOs. It was a virtual daisy chain of leverage, and when people stopped paying for mortgages they shouldn’t have been given the first place, there was a domino-like effect that led to a bailout of some of the country’s biggest financial institutions.

Today, there is no market for subprime mortgages or related bonds, CDOs and credit-default swaps to speak of. What is out there is negligible and certainly not a threat to the financial system. I am not much of a fan of regulation, but it’s clear that things like the Volcker Rule, the Dodd-Frank Act and Basel III have made the financial system safer by curbing excessive risk-taking. In fact, it may be nearly impossible to have a housing-related crisis ever again. I recently obtained a construction loan for my new home, and I can assure you that the underwriting standards were the opposite of lax. At the very end of the process, my lender required a 30% down payment instead of 20% out of an abundance of caution.

The second reason is that consumers have massively deleveraged themselves. Almost half of mortgaged properties were considered equity-rich in the second quarter, meaning owners had at least 50% in home equity, according to real estate data provider Attom. Bloomberg News reported that it was the ninth straight quarterly increase, helped in part by an increase in down payments by recent buyers. Nationwide, the portion of mortgaged homes that were equity-rich reached a record 48.1% in last quarter, up from 34.4% a year earlier. Meanwhile, the share of homes that were considered seriously underwater — where the mortgage is 25% greater that the property’s estimated market value — dropped to a low of 2.9%.