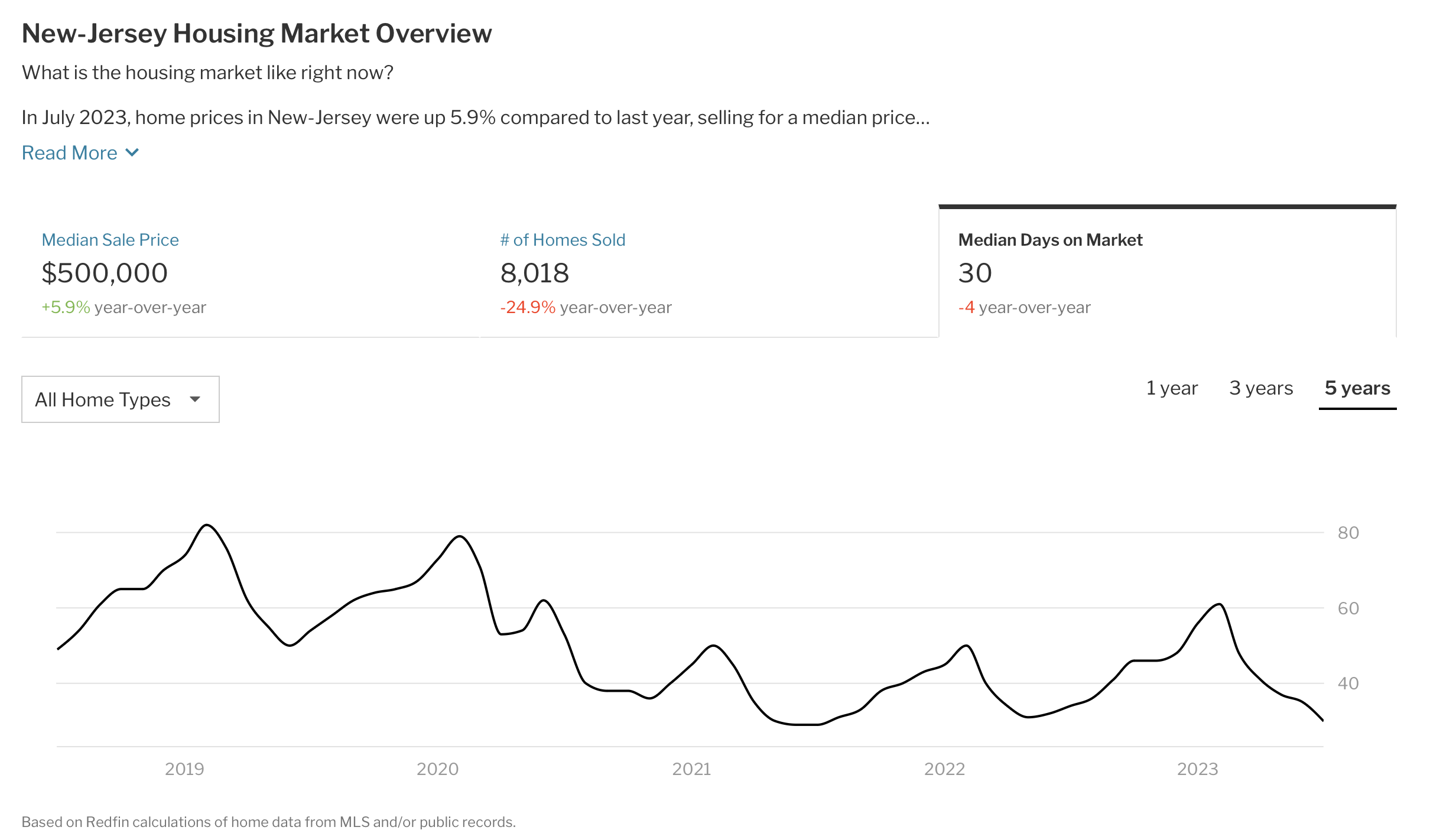

From Redfin:

New-Jersey Housing Market Overview

From Wolf Street:

Homebuilders don’t have the luxury of outwaiting the market, or waiting for the Fed to slash rates, or whatever, they must build and sell homes, that’s their business, no matter what the conditions in the market.

And the market is struggling with 7%-plus 30-year fixed mortgage rates and sky-high prices, after a ridiculous free-money spike during the pandemic. Sales of existing homes have plunged by about 25% from the same period in 2018 and 2019, and by about 32% from the same period in 2021, because buyers have pulled back, and the people with 3% mortgages have left the housing market altogether, not putting their homes on the market and not buying homes either, not even looking at homes.

That plunge in sales might be OK with potential home sellers, thinking that this too shall pass, but it’s not OK with homebuilders, and they’ve been adjusting to this market by cutting prices, building at lower price points, buying down mortgage rates, and offering incentives, such as free upgrades.

The latter two – buying down mortgage rates and piling on incentives – don’t show up in the prices of the homes they sell. So the pricing data that we have from the Census Bureau about sales of new single-family houses do not include the costs of mortgage-rate buydowns and incentives.

With mortgage rate buydowns, the homebuilder subsidizes the mortgage payment.

The duration of the buydown can be for a few years, which effectively turns it into a teaser rate that can cause problems when the rate jumps to normal.

Or the rate-buydown can be for the entire term of the mortgage (“permanent”).

The big homebuilders have mortgage-lender subsidiaries that originate the mortgage for their customers and then sell the mortgage to Government Sponsored Enterprises, such as Fannie Mae, which will securitize the mortgages into MBS. For example, the mortgage-lender subsidiary of D.R. Horton is DHI Mortgage Company.

Having their own mortgage lender makes rate buydowns a lot simpler for homebuilders. This is similar to the “captive” auto lenders, such as Ford Credit offering 0% 36-month financing for F-150 XLTs at the moment.

The costs of the mortgage-rate buy-downs can be big, because the home prices are big, and buydowns effectively lower the sales price of the home.

From Yahoo Finance:

The National Association of Realtors housing affordability index was unchanged at 87.8 in July, matching the lowest level in data back to 1989. A level of 100 means a family with the median income has enough income to qualify for a mortgage at the median home price.

The typical family spent 28.5% of their income on the principal and interest of their mortgage payment each month, also matching an all-time high, according to the report released Friday. Qualifying income for a mortgage, based on a 20% down payment, was a record $104,496 in July.

“Higher mortgage rates continued to harm affordability despite modestly lower median home prices,” Lawrence Yun, NAR’s chief economist, said in an email. “Consequently, the Federal Reserve is unintentionally widening the social divide by preventing middle-income renters from ownership opportunities.”

Buying conditions have deteriorated swiftly over the last year as borrowing costs climbed and a shortage of available homes kept asking prices elevated. Mortgage rates are now near their highest level since 2000 and many homeowners who locked in at much cheaper rates are reluctant to sell.

The lack of inventory has, in turn, driven up home prices, and allowed the housing market to recoup the nearly $3 trillion in value wiped out last year.

From Redfin:

Nearly one of every five (18%) millennials and 12% of Gen Zers who replied to a recent housing survey believe they will never own a home.

That’s according to a Redfin-commissioned survey conducted by Qualtrics in May and June 2023. The survey was fielded to 5,079 U.S. residents who either moved in the last year, plan to move in the next year, or rent their home. This report focuses on the 1,340 Gen Z (aged 18 to 26) and 1,973 millennial (aged 27 to 42) respondents. The stat above is based on the following question: Do you believe that you will ever own your own home in the future? Respondents could choose “yes” or “no.”

Lack of affordability is the number-one barrier to homeownership for young Americans. Roughly half of Gen Z and millennial renters who believe they’re unlikely to purchase a home in the near future say the high price of homes on the market is blocking them from buying. That’s the most commonly cited barrier, and it’s followed by several other affordability-related reasons.

Nearly half (46%) of millennials and one-third (33%) of Gen Zers say their lack of ability to save for a down payment is a barrier, and more than one-third of both Gen Zers and millennials say mortgage rates are too high. Roughly one-third also say they’re unable to afford monthly mortgage payments. About one in five (21%) Gen Zers and 16% of millennials say they need to pay off their student loan debt before they’re able to buy a home.

From the NYT:

New York City officials on Tuesday are expected to start enforcing strict new regulations that limit residents’ ability to rent out homes through platforms like Airbnb.

The move is expected to lead to the removal of thousands of listings from the platforms. It is the latest and potentially most consequential development in the yearslong feud between big cities and the home-sharing companies.

The city argues that the proliferation of short-term rentals through Airbnb and other platforms has pushed up rents and helped fuel New York City’s housing shortage.

Airbnb has said the new rules amount to a “de facto ban” on the platform, and other critics say the city is bending to the lobbying of the hotel industry and locking out cheaper options for visitors.

…

For years, the city has maintained that existing laws preclude people from renting out homes to guests for less than 30 days, unless the host is present during the stay. The city also asserts that no more than two guests are allowed to stay at a time, and that they must have ready access to the entire home.

But there continue to be numerous listings for rentals of whole apartments and homes, and the city has argued companies like Airbnb are not policing their platforms aggressively enough to root out violators.

A city official claimed in a July court filing that more than half of Airbnb’s $85 million net revenue in 2022 from short-term rentals in New York City came from activity that is illegal. Airbnb disputes the figure.

The new regulations, which the city will begin enforcing on Tuesday after a series of court challenges, require hosts to register with the city to be allowed to rent on a short-term basis.

From the Star Ledger:

Location may be the key word in real estate but, like anything else, timing can also make a difference.

A house in Closter that hit the market in May just closed for $205,000 over its asking price. And the listing agent, Risa Corson of Coldwell Banker Realty, says the “timing was crucial.”

The sellers initially wanted to wait until August to list, but Corson convinced them to list sooner and write into their terms that they couldn’t close until August, when their new out-of-state home would be finished.

“We have a very strong school system, we’re close to New York City and a lot of people want to move to town for the schools and proximity,” said Corson, a 19-year Closter resident herself. “I knew we’d have a better pool of buyers in May than if we waited until the end of summer.”

The four-bedroom, three-bathroom home was listed for $995,000 and sold for $1.2 million. “The house needed some updates but it was well maintained,” Corson said. “It’s on a cul-de-sac.”

There were 40 showings in four days and two offers were made by the second day. The sellers cancelled a weekend open house and asked for highest and best offers on the fifth day. At that point they already had an offer for $1.1 million.

“There was very little on the market in that price range at that time,” Corson said. “I knew given the low Inventory, the time of year and interest rate concerns that time was of the essence.”

A total of 12 offers, all over asking price, were submitted.

Corson sold a house two doors down in November. That one was listed for $999,000 and sold for $1.1 million.

“I even was a little shocked myself (the more recent listing) went that much over asking,” she said.

From the Star Ledger:

For the first time in a few years, you might’ve gotten a deal or picked up a prime last-minute rental at the Jersey Shore this summer.

That’s because there were more houses to choose from and demand wasn’t as strong.

The rental markets near New Jersey beaches have been booming since the COVID pandemic as people chose to stay closer to home. That led to about a 25% increase in prices and difficulty in finding a prime house — one close to the beach, with a pool or that allows pets.

But this summer, things normalized. There were more houses in the rental inventory and demand was weaker as people resumed long-distance traveling or balked at the high rental prices while paying more for things like gas and groceries.

“The ‘COVID bump’ that we experienced over the last three summers has finally come to an end,” said Duane Watlington, founder of Vacation Rentals Jersey Shore LLC, which lists properties for rent in Ocean City, Long Beach Island and Wildwood.

…

“While it’s a step back from last two years,” he said, “we picked up a lot of fans during COVID who hadn’t come here. They liked the area and continue to come here.”

Inquiries for rentals started strong in January but came to a standstill from about March until June, said James Ward of Keller Williams Ocean Living in Point Pleasant.

“They’re usually prime booking times,” he said. “I attribute it to people finding deals in other places and generally choosing other options.”

…

The increase in rental inventory, from people who purchased homes the past few years and are now placing them up for rent, has benefitted renters. Some that weren’t fully rented offered price reductions throughout the season — and they increased the pool of homes to choose from.

…

“People are choosing real estate over everything else to invest their money in,” said Ward. “So there is a lot of new rental inventory.”

Watlington, of Vacation Rentals Jersey Shore LLC, has added 500 new listings since the end of last year, bringing his total rolodex to 2,700 rentals.

“This increased inventory gives vacationers a wider selection to choose from across all price levels,” he said.

From the Record:

As if being a first-time home buyer in New Jersey weren’t difficult enough, we can now add low market inventory and high mortgage rates into the mix.

As of this week, the current rates in New Jersey are 7.55% for a 30-year fixed mortgage, according to Bankrate. That’s just below the national average rate of 7.63%. This time last year, the average 30-year fixed mortgage rate was 5.55%.

“Interest rates are staying up, so that’s making people maybe who thought about moving go, ‘Well, I know I can sell my house now, but I don’t want to pay seven and a half percent’ on a mortgage for my next home,” whereas “maybe I’m currently paying three or four percent on my mortgage” for my current home, said Jenn Vongas, a real estate agent with Coldwell Banker Realty in Morris County.

Because of this, New Jersey’s housing inventory has declined 23% over the past 12 months, with 11,404 new listings in July 2022 versus just 8,732 new listings in July 2023.

Between the limited inventory pushing housing prices up and those rising mortgage rates, first-time buyers are being further discouraged from entering the housing market.

“It’s not that there is no inventory, but it’s moving fast,” said Ghada Abbasi, a real estate agent for Coldwell Banker Realty in Bergen County. “So we cannot catch up with the demand.”

Abbasi said first-time buyers are often getting beaten out by individuals with higher purchasing power. Offers made by these buyers are more frequently chosen over offers from first-time buyers simply because they are able to do things like make larger down payments and put in offers over the original asking price, as well as pay in cash.

“The demand is there for the premier buyer, I should say. The buyers who will meet the income requirements, who have the cash,” she said. “Whenever something comes up, they jump on it, overpay for it, and get it.”

From the Week:

With the prices of homes remaining stubbornly unaffordable, the number of available home listings shrinking, and record high mortgage rates, potential homebuyers are increasingly looking to newly constructed homes to fill the gap. Builders are expected to meet the rising demand for new homes while also dealing with soaring construction costs. The solution? New homes are being built smaller and much closer together than before.

The housing market seems locked in a cycle that is driving the affordability of homeownership down. The average mortgage rates are at the highest they’ve been in over a decade, driven by the Federal Reserve‘s efforts to avoid a recession, The Wall Street Journal reported earlier this summer. The rates keep potential buyers out of the market while simultaneously “discouraging homeowners from selling, limiting the supply of homes for sale,” the outlet added. At the same time, the high demand and low supply are keeping house prices high.

With the market shrinking, home builders are trying to find ways to make housing affordable in order to entice more customers to buy new homes, and shrinking the size of newly built single-family homes has become a popular way to do that. Reducing the size of new homes helps “cost-constrained buyers” and can “boost the bottom line for builders who are contending with spiraling labor and construction costs,” per a more recent report from the Journal. Data from Livabl by Zonda, a listing platform for new construction homes, showed the average unit size for newly constructed homes decreased by 10 percent nationally, the Journal summarized.

During the pandemic, the number of detached single-family homes increased, but a “succession of economic shocks” has “caused builders to change course,” Zillowreported. Construction starts for typical single-family homes declined 10.1 percent between 2021 and 2022, but starts for houses with less than three bedrooms increased 9.5 percent in that time. Zillow found that “the homes that builders opted to begin work on became smaller, more likely to be attached and more likely to be built offsite.” Attached properties such as condos or townhouses also saw a 2.9 percent increase, compared to detached homes, which fell by 12 percent over the same period.

…

The trend toward smaller homes is becoming “pretty consistent nationally,” Mikaela Arroyo, director of the New Home Trends Institute at John Burns Real Estate Consulting, told Market Watch. “We’re seeing a lot of deletion of separate, defined spaces,” Arroyo said. Builders are eschewing the kitchen, dining, and living room setup for one kitchen and one “great room.” The kitchens are larger than they used to be “because we’re taking away the dining room,” she added. And while smaller homes are “not solving the affordability crisis,” they are “creating opportunities for people to be able to afford an entry-level home in an area,” Arroyo said.

From Reuters:

Existing home sales fell 2.2% in July to a seasonally adjusted annual rate of 4.07 million units, the lowest level since January, from an unrevised 4.16 million units in June, the National Association of Realtors said on Tuesday. Economists polled by Reuters had forecast home sales would be little changed at 4.15 million units.

Sales fell in the Northeast, Midwest and South, but rose in the West, where home prices have fallen most sharply in the past year. All regions experienced annual sales declines.

Home resales, which account for a big chunk of U.S. housing sales, fell 16.6% on a year-on-year basis in July.

Home prices have bottomed out after being pressured by the Federal Reserve’s aggressive interest rate hikes, but the persistent shortage of properties for sale could limit any rebound as many prospective buyers are forced out of the market.

Mortgage rates have surged again recently to the highest levels in decades, with the average rate on the popular 30-year fixed-rate mortgage topping 7% in the latest week, according to mortgage finance giant Freddie Mac.

There were 1.11 million previously owned homes on the market last month, up 3.7% from a month earlier but down 14.6% from July 2022. At July’s sales pace, it would take 3.3 months to exhaust the current inventory of existing homes, up from 3.2 months a year ago.

A four-to-seven-month supply is viewed as a healthy balance between supply and demand. The median existing house price rose 1.9% from a year earlier to $406,700 in July, the fourth time it has topped $400,000.

Interesting look at mortgage rate lock-in from Fortune:

From Fortune:

On Monday, the average 30-year fixed mortgage rate reached 7.48%, marking the highest level since the year 2000. Even prior to this recent surge in mortgage rates, housing affordability, as monitored by the Atlanta Fed, had already deteriorated beyond the levels seen at the housing bubble’s peak in 2006. Once this latest mortgage rate surge is factored in, August 2023 will become the worst month for housing affordability this century.

The journey to this predicament can be traced back to last year’s sharp rise in mortgage rates, which escalated from 3% to over 7%. That rate surge, coupled with the Pandemic Housing Boom pushing U.S. home prices up over 40% in just over two years, deteriorated housing affordability across the nation.

“The housing market is at a pivotal point as we head into fall. Mortgage rates are now at more than a two-decade high, and for some home shoppers, those higher rates are enough to cause them to step back from the market,” wrote Lisa Sturtevant, chief economist at Bright MLS, in a statement to Fortune. “It is likely to be a very slow fall [in the] housing market this year. Home prices, which had rebounded this summer, will dip in some markets as new listing activity increases at the same time a segment of the homebuying population sits the market out.”

While Sturtevant doesn’t expect “major [house] price corrections since supply is still at historically low levels and overall economic conditions remain healthy,” she does see risk in overheated housing markets. House prices in places like Austinand Boise have already started to fall again.

“The markets at greatest risk of price declines are those where affordability challenges are the worst, including some West Coast markets, as well as places where prices have run up quickly, including in parts of the Sunbelt,” Sturtevant says.

From Yahoo Finance:

Goldman Sachs housing analysts no longer think home prices will fall this year. Instead, they are forecasting a slight increase.

“We are revising our home price forecasts higher, to 1.8% for full-year 2023 vs. -2.2% prior, and 3.5% in 2024 vs. 2.8% prior,” Vinay Viswanathan, a fixed income strategist at Goldman Sachs, wrote in a note for the firm’s housing team. “These forecasts imply home prices will remain roughly unchanged through [the] year-end and then return to trend growth levels in 2024.”

This comes as home prices have resumed an upward trend and mortgage rates remain elevated, creating a bleak homeownership situation for many Americans. Goldman Sachs analysts previously thought that higher mortgage rates would put more downward pressure on home prices.

After declining month over month for seven straight months late last year and into 2023, home prices reversed course in February have stayed that way through May, the latest month for which there is data from Case-Shiller’s national price index.

Craig Lazzara, managing director at S&P DJI, said the data backs the case that the final month of monthly declines was in January.

…

Based on the firm’s housing affordability index hitting record lows, the Goldman Sachs analysts expected that home prices would need to decline nationwide before buyers would bite. But that conclusion has changed.

“We trace most of this demand to non-economic sources: household formation and seasonal turnover,” Viswanathan wrote. “While high frequency data suggests housing turnover may moderate, household formation is well above its long-term trend.”

…

Housing affordability has worsened over the past year due to high mortgage rates, with the average rate on the 30-year fixed mortgage climbing north of 7% in the past week, Freddie Mac reported.

While so far many homebuyers have swallowed these increased costs, they “demonstrated behavior that, in our view, reflects unsustainable adaptations to elevated mortgage rates,” Goldman Sachs noted.

For instance, the average debt-to-income ratio on conforming purchase mortgages is over 38%, “a significant aberration from post-Global Financial Crisis averages,” Viswanathan wrote.

“In addition, smaller and lower price homes have seen stronger price growth than larger, higher-quality properties. That said, we expect mortgage rates fall by 100 basis point through the end of next year, somewhat stabilizing affordability,” Viswanathan wrote.

From ROI-NJ:

How about that economy?

The answer may not be that good: 44% of 434 certified public accountants surveyed by the New Jersey Society of Certified Public Accountants believed New Jersey’s economy is expected to stay about the same during the second half of the year compared to the first half … but an equal number (44%) believed it will worsen, and only 12% think it will improve.

Inflation and the ability to find skilled personnel are two of the biggest challenges facing survey participants this year, at 66% and 53%, respectively, followed by state and federal policies that are unfriendly to businesses (40%) and rising interest rates (39%).

Going forward, respondents said the most helpful steps government could take to improve business conditions include implementing measures to ease inflation (73%) and reducing burdensome regulations (66%). Respondents recommended addressing the needs of small business, lessening the tax burdens of individuals, cutting government spending, reducing the pension burden and incentivizing people to work.

“As strategic advisers to their clients and organizations, CPAs are good sounding boards about the business environment. Our members always have a great read on what’s important for growth and sustaining business operations,” Aiysha Johnson, executive director and CEO of the NJCPA, said.

This year’s survey, conducted in June and sponsored by Bernstein Private Wealth Management, was conducted to gauge CPAs’ outlook on the national and New Jersey economies midway through the year.

The moderate stance is more positive than the same economic survey initiated by the NJCPA in 2022, which showed nearly 65% of CPAs believed New Jersey’s economy would worsen during the second half of the year and 28% of CPAs believed economic conditions in the state would stay the same. Only 7% thought it would improve.

Last year, the survey showed similar top concerns, but inflation at that time was a heavier worry at 73%, followed by the availability of skilled personnel at 57%.

“Surveys like this one are a good way to gauge sentiment in all facets of society. It’s not surprising that inflation was more of a concern last year,” Roosevelt Bowman, a senior investment strategist with Bernstein Private Wealth Management, said.